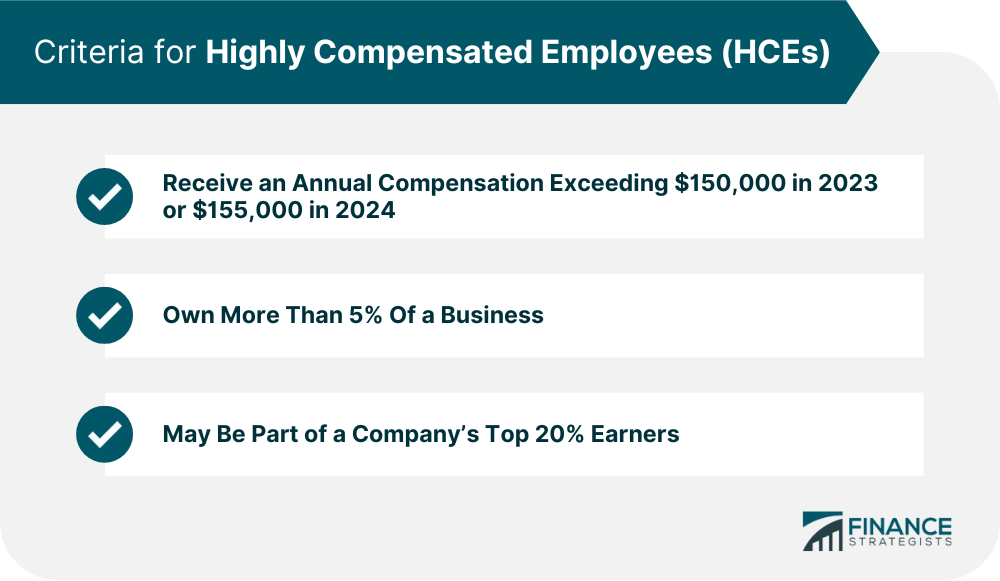

Highly Compensated Employees (HCEs) are individuals who make considerably more money than a company's other workers. Examples include executives, managers, and owners. It is vital to distinguish HCEs because they can affect how a company's 401(k) system is set up. The IRS defines HCEs based on employees' annual total compensation, including paychecks, bonuses, commissions, and cafeteria plan salary deferrals. Individuals receiving yearly compensation that exceeds $155,000 in 2024 or $150,000 in 2023 are considered HCEs. An individual is also considered an HCE if they own more than 5% of the business or company sponsoring the 401(k) plan, regardless of annual compensation. The 5% includes the individual's own shares and any of their family's shares in the company. Individuals may also be deemed as HCEs if their company ranks them in the top 20% of employees based on compensation.

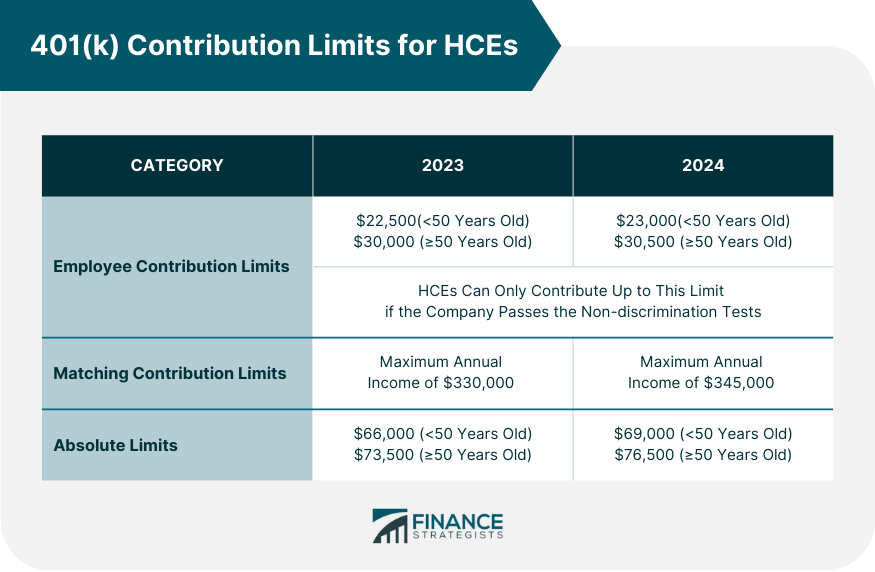

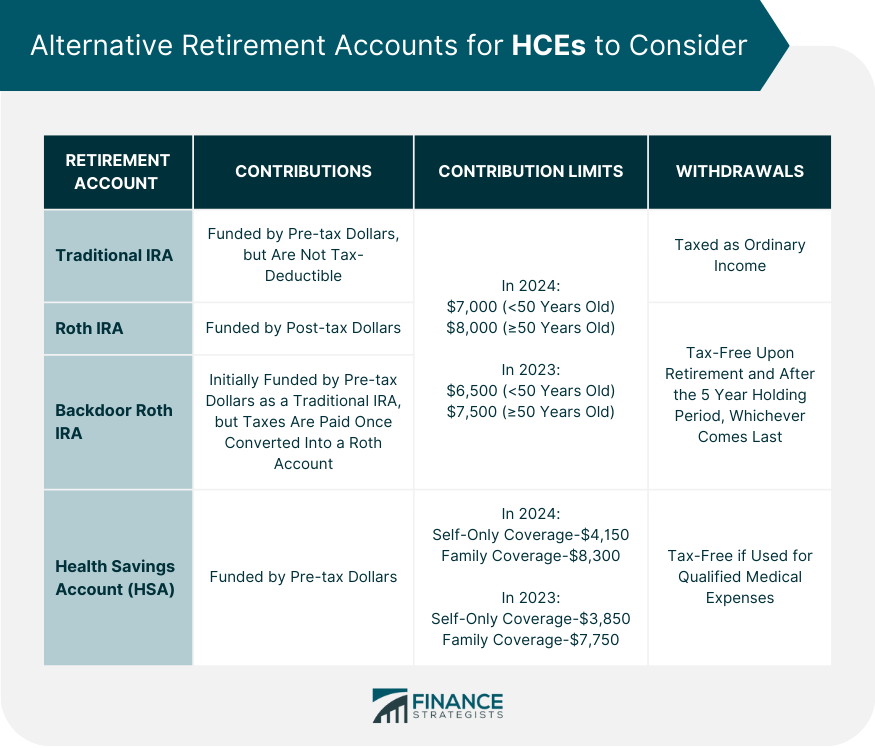

Generally, a 401(k) participant can contribute up to $23,000 to a 401(k) in 2024 ($22,500 in 2023). Employees 50 years and older are also allowed a catch-up contribution of $7,500 ($7,500 in 2023). These amounts do not yet include matching contributions from employers. However, the actual amount an HCE can contribute highly depends on how much other employees contribute, especially those not tagged as HCEs. It is because the IRS requires companies to run the plans they sponsor through non-discrimination tests yearly. These tests are intended to ensure that a company’s 401(k) plans do not favor HCEs over other employees. As part of these discrimination tests, the average HCE contributions of a company must not exceed the average contributions of non-HCEs by more than 2%. For example, suppose non-HCEs contributed an average of 3% of their annual salary towards 401(k) plans. In that case, HCEs can only channel up to 5% of their yearly compensation toward their 401(k) plan savings. Additionally, the total HCE contributions can only exceed total non-HCE contributions by 2%. If a company fails these tests, they may require their HCEs to withdraw part of their contributions. Aside from employee contribution limits, there are other contribution limits that an HCE’s 401(k) must adhere to. These are: Some employers offer matching contributions to 401(k) plans as part of their benefits package. It means that whatever amount you contribute, your sponsoring company can match a certain percentage and add it to your 401(k) savings. Employer matching programs are often based not just on how much an employee contributes but also on their annual compensation. The IRS also adds a further limit to the amount of yearly income that employers can match. In 2024, employer matches must be computed based on a maximum annual income per HCE of $345,000 (an increase from the $330,000 limit in 2023). This is consistent for all HCEs, whether their salary exceeds this limit. To illustrate further, consider this example: Suppose your annual salary is $460,000, and your company offers to match 100% of your contributions up to 5% of your total compensation. You elect to max out the IRS contribution limit and channel $23,000 to your 401(k) plan. You expected your company's contributions to equal $23,000, which is exactly 5% of the $460,000. But because of the IRS matching contribution limit, your company can only contribute $17,250, which is 5% of $345,000. The IRS sets an absolute limit to the total amounts that can be deposited into a 401(k) plan from all funding sources, including an employee’s contributions and an employer’s matches. This limit can also change each year. For 2024, the limit is either 100% of a contributor’s annual income or a maximum of $69,000 (for employees under 50 years old) and $76,500 (for those aged 50 and above), whichever is less. These new absolute limits increased from 2023’s $66,000 and $73,500, respectively. Note that absolute limits typically apply to HCEs with very generous employers or to self-employed individuals who are both employer and employee in a solo 401(k) plan. It is clear from the preceding that there are limits to the amount of money you can save through 401(k) plans, especially if you are an HCE. Nonetheless, there are other ways you can increase savings for your retirement, such as: As an HCE, you cannot claim tax deductions on traditional individual retirement account (IRA) contributions because such benefits end after specific income thresholds. Tax deductions begin phasing out when a single person’s 2024 modified adjusted gross income (MAGI) reaches $77,000, or $123,000 for married couples filing jointly. These deductions are entirely eliminated once a single person’s income exceeds $87,000 or $143,000 for married couples filing jointly. However, you can still use a traditional IRA and benefit from the tax-deferred growth of your investments over time. It can supplement your 401(k) plan and increase your retirement savings. The 2024 contribution limits for traditional IRAs are $7,000 for those below 50 and $8,000 for those aged 50 and above. This is an increase from the 2023 limit of $6,500 and $7,500, respectively. Roth IRAs accept after-tax contributions, which means your money grows tax-free. Roth IRAs are not specifically designed for high-income individuals, but some HCEs can contribute at least partially if their income is within the threshold set by the IRS. For 2024, if your income falls between $146,000 to $161,000 ($230,000 to $240,000 for married couples filing jointly), you can make a partial contribution to a Roth IRA. Remember that if your income exceeds the above ranges, you are prohibited from contributing to a Roth IRA. To make full contributions to a Roth IRA, the IRS allows what is called a backdoor Roth IRA. It involves making non-tax deductible contributions to a traditional IRA before converting it to a Roth IRA. Consider the following steps: Open a traditional and a Roth IRA simultaneously. Contribute $6,500 to the traditional IRA, which is the maximum allowed in 2023. Next, convert the traditional IRA into a Roth IRA and pay taxes on the $6,500. Now your earnings can grow tax-free. This process helps you navigate around the contribution limits for a Roth IRA. Using the backdoor, you can contribute the full $6,5000 instead of just a partial contribution. Note that a backdoor Roth IRA can be tricky. It is best to ask for guidance from a qualified financial advisor for smooth processing. If you have a qualified high-deductible health plan (HDHP), you can set up an HSA. You can channel pre-tax dollars into this account and enjoy tax-free growth. Additionally, you will not be taxed for withdrawals made for qualified medical expenses. The 2024 contribution limit for HSAs is $4,150 for individuals and $8,300 for families, an increase from 2023's $3,850 and $7,750. While HSAs are not technically retirement plans, you can save money for qualified medical expenses, allowing your 401(k) and other retirement funds to grow unimpeded. Highly Compensated Employees are individuals who make considerably more money than a company's other workers. Examples include executives, managers, and owners. HCEs maintain retirement savings in 401(k) plans like the average employee. However, the IRS sets limits to what HCEs can contribute based on their total compensations, other employees' contributions, employer matching contributions, and the absolute limit on contributions. If you are an HCE, IRS limits can be unnerving, but there are other ways to increase your retirement savings beyond your 401(k). You can fund a traditional IRA with non-deductible contributions, open a Roth IRA, set up a backdoor Roth IRA, or contribute to an HSA. It is always best to consult a qualified financial advisor to ensure that you make wise decisions for your retirement planning needs. These professionals can guide you on the best strategies for your goals and risk tolerance.What Are Highly Compensated Employees (HCEs)?

Have questions about 401(k) Contributions? Click here.

401(k) Employee Contribution Limits for HCEs

Additional 401(k) Contribution Limits for HCEs

Alternative Retirement Planning Strategies for HCEs

Funding a Traditional IRA With Non-Tax Deductible Contributions

Contributing to a Roth IRA

Opening a Backdoor Roth IRA

Setting up a Health Savings Account (HSA)

Final Thoughts

401(k) Contribution Limits for Highly Compensated Employees FAQs

The Internal Revenue Service (IRS) defines HCEs as individuals receiving a total annual compensation exceeding $155,000 in 2024 or $150,000 in 2023. You can also be considered an HCE if you own 5% shares of the company or are ranked in the top 20% of all employees based on total compensation.

Generally, the absolute limit, which is a combination of employee and employer matching contributions, is set at $69,000 ($76,500 for employees 50 and older). However, the Internal Revenue Service (IRS) sets additional limits for HCEs based on the average salary percentage that non-HCEs contribute and the average total contributions of other employees.

Yes, if your annual income is less than or equal to $23,000 ($30,500 if you are aged 50 or older).

The salary deferral limit is the maximum amount of an employee’s pre-tax compensation that can be contributed to a 401(k). The limit for 2024 is $23,000. For individuals aged 50 or older, their limit is $30,500 because they can contribute an additional catch-up contribution of $7,500.

HCEs can consider funding a traditional individual retirement account (IRA) with non-tax deductible dollars, opening a Roth IRA, using a backdoor Roth IRA, or setting up a health savings account (HSA) to add to their 401(k) plan.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.