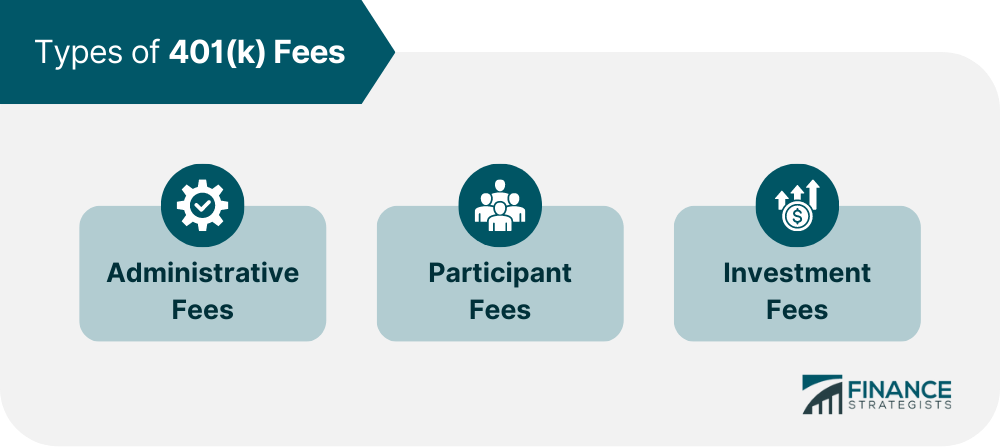

The types and amounts of fees that are charged by a 401(k) plan can impact on the total return earned by plan participants, particularly over long periods of time. For this reason, it is vitally important for plan participants to know how much they are paying in fees each year (or quarter or month) so that they can make informed investment decisions. The Department of Labor requires all 401(k) plan sponsors to furnish their participants with a prospectus at least once every 14 months that provides a comprehensive breakdown of all fees that are charged by the plan, and when they are charged for non-recurring events, such as moving money from one fund to another. This is fulfilled in the form of a 404(a)(5) participant fee disclosure. The plan administrator will create this document and then pass it on to the plan sponsor. The sponsor then has the responsibility of sending this to each employee in the plan. The disclosure can be sent via email or snail mail. Email is usually the preferred method, but all plan participants have to have either access to a computer or have opted in for email notification. Have questions about 401(k) Plans? Click here. The fee disclosure form is sent to all new participants when they first join the plan and all current participants about once a year. This form must break down three types of fees that are charged within the plan, which are listed as follows: It is relatively easy to find the actual breakdown of all fees that are charged within the plan prospectus. All fees are generally listed in boldface type so that they are easy to find and understand. This allows employees to make more informed investment choices and minimize plan expenses so that their savings balances can grow at a faster rate over time. In fact, the DoL has estimated $14 billion in savings to participants in 10 years as a result of fee disclosure rules. The vast majority of the savings, according to the DoL, come from the increased access to plan information and increased ability to choose lower cost investments. Fee disclosure rules may be relatively new - but they're in place because of a greater need for transparency. Transparent fees show employees exactly what they're taking home, and ultimately help plan sponsors fulfill their fiduciary duty to act in the financial best interests of their plan participants. That means, first and foremost, reasonable fees for 401(k) services. Employers therefore need to be cognizant of the fees that their investments are charging and monitor whether they are reasonable or not on an ongoing basis.401(k) Fee Disclosure Form

Many plans offer traditional mutual funds as their primary investment options, and these funds may assess a sales charge at the time of purchase or redemption.

There are also annual 12b-1 fees that are charged for the funds' operations and management. Some plans may instead charge a flat fee or percentage instead of transaction-based fees such as sales charges or commissions.

401(k) Plan Fee Disclosure FAQs

A 401(k) plan is a retirement plan offered by an employer designed to help employees save for retirement.

A 401(k) Plan Fee Disclosure is an official document that outlines the fees associated with a particular 401(k) plan, such as administrative costs and investment management fees. It also includes information about any other services included in the plan.

Employers must provide their employees with annual disclosure statements that include information about their 401(k) plan's fees. This statement must be provided no later than 30 days after the end of each plan year or within 30 days of when a new employee enrolls in the plan.

The disclosure must include the total administrative and investment management fees charged by the plan, as well as any other services included in the plan. It also provides information about who pays these fees (e.g., employer vs. employee).

Yes, small employers may be exempt from certain portions of fee disclosures if their plans have fewer than 100 participants. However, all employers are still required to provide employees with annual statements that clearly outline all applicable fees associated with the plan.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.