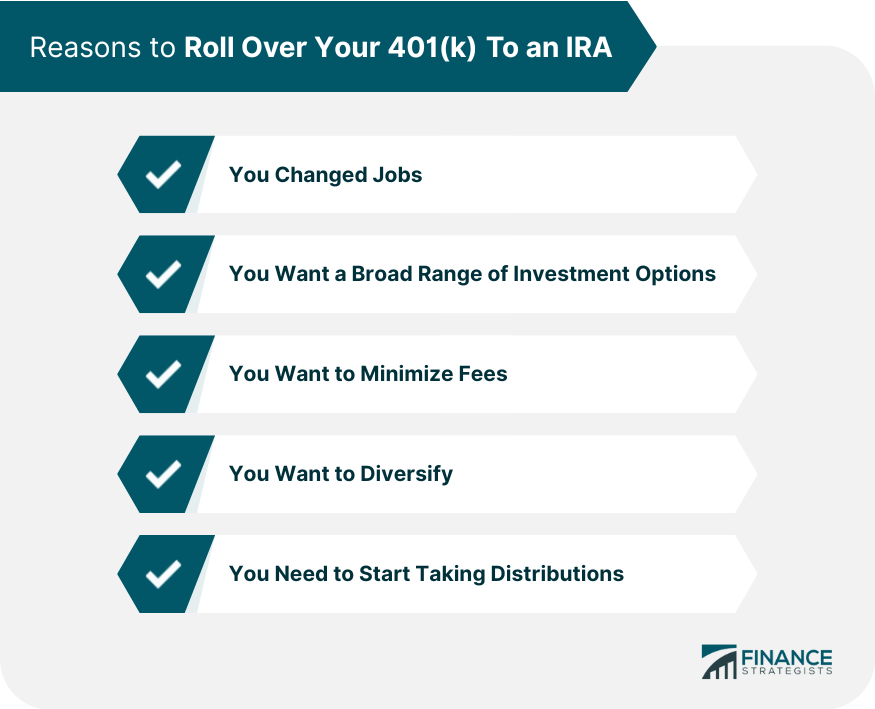

A 401(k) Rollover to IRA is when you take the money out of your 401(k) plan and put it into an Individual Retirement Account (IRA). It's very easy to roll over a 401(k) to an IRA. There are many reasons why you'd want or need to transfer money from one account or investment vehicle into another, including: Need help with a Roth 401(k) rollover? Click here. 401(k) rollovers can be a great way to save for retirement. When you roll over your 401(k) into an IRA, you get to keep all of the money in the account and you don’t have to pay any taxes on it. You also get to choose your own investments, which gives you a lot more flexibility than you would have if you left your money in a 401(k). There are two ways to roll over a 401(k) into an IRA - you can either do a direct rollover or an indirect rollover. This is when the money from your 401(k) plan goes directly to your new IRA account, without going through your own hands first. This is the best way to rollover a 401(k) because it ensures that you receive the money immediately. If you take possession of the check for your 401(k) distribution, then it becomes taxable that year - even if you deposit it into your IRA rather than spend it! You can also rollover a 401(k) by doing an indirect rollover through what's called a 60-day rollover. This is when you withdraw the money from your current 401(k) plan and wait at least 60 days before rolling it over into either another 401(k) or an IRA. If you don't wait the required time period, then the IRS considers this a taxable distribution, and you'll have to pay taxes on the money as well as a 10% early withdrawal penalty if you're under age 59½. The direct rollover is generally the best option when rolling over a 401(k) into an IRA, because it's simpler and faster. However, not everyone is able to do a direct rollover - if your 401(k) is held with the old employer, then they may be unwilling to release the money to the new provider. In this case, you'll have to do an indirect rollover. Just be sure to follow all of the rules so that you don't get hit with any penalties from the IRS. The benefits of rolling over your 401(k) into an IRA include: a.) Contributing to an IRA is tax-deductible, which can help reduce your taxable income and lower your current year's taxes if you qualify. b.) You can set up a Simplified Employee Pension, or SEP-IRA - a traditional IRA that allows you to contribute as much as 25% of your income from self-employment for retirement purposes. The disadvantages of rolling over a 401(k) may include: Before you decide to rollover a 401(k) into an IRA, there are a few things you should consider:

How Rollover Works

Direct Rollover

Indirect Rollover

Best Option for You

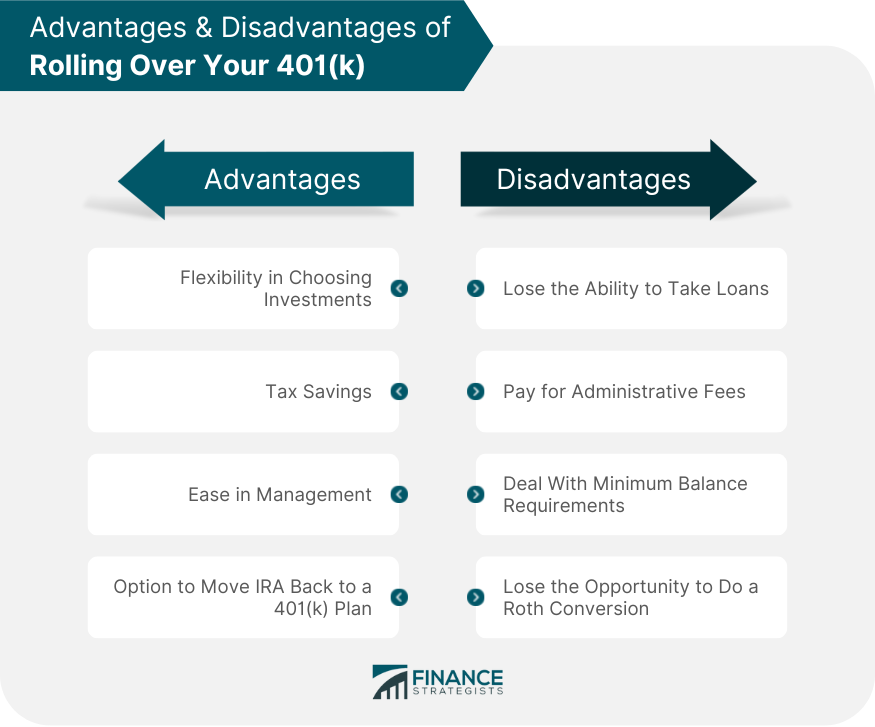

Benefits of Rolling Over Your 401(k)

Disadvantages of Rolling Over Your 401(k)

Things to Consider Before Making the Switch

401(k) Rollover to IRA FAQs

A 401(k) rollover to IRA is the process of transferring funds from a 401(k) account into an IRA account.

The rollover works by transferring funds from the 401(k) account to the IRA account. This can be done in two ways: a direct rollover, where the money is transferred directly from the 401(k) provider to the IRA provider, or an indirect rollover, where the money is transferred to the individual, who then has to deposit it into an IRA account within 60 days.

The benefits of rolling over a 401(k) into an IRA include: choosing the type and amount of investments that your IRA holds, keeping your existing 401(k) or changing to a lower-cost provider or investment option and taking loans against your 401(k) account.

The disadvantages of rolling over a 401(k) into an IRA include losing the ability to take loans against your 401(k) account, paying administrative fees if you rollover your 401(k) into an IRA with a different provider and if the fees are higher, then this could reduce your returns.

Before making the switch from a 401(k) to an IRA, you should consider how much money do you have in your 401(k) account, what is the current balance of your 401(k) account, what type of investments does your 401(k) account hold, and what type of investments does your IRA account hold?

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.