501(c)(3) organizations are non-profit entities that have been granted tax-exempt status by the Internal Revenue Service (IRS). A core feature of these organizations is their commitment to serving the public interest, encompassing fields like education, charity, science, literature, and many more. Operating primarily on funds from donations and grants, these organizations are exempt from federal income taxes and can provide donors with tax-deductible receipts. Furthermore, 501(c)(3) organizations are defined by the IRS into two major categories, namely public charities and private foundations. Public charities typically receive a larger portion of their funds from the public or governmental units and are subject to stricter regulation. Private foundations, on the other hand, are often funded by a single source, such as a family or a corporation, and have more flexibility in their operations. To qualify for the 501(c)(3) status, an organization's purpose, and mission must be dedicated to serving the public good. The IRS stipulates that this can include charitable, religious, educational, scientific, literary, and public safety testing, fostering amateur sports competitions, and preventing cruelty to children or animals. Moreover, it's crucial that the mission statement of the organization is clearly outlined and communicated, highlighting its aim to contribute to the public interest. Organizations need to meticulously detail their goals and strategies to achieve them to demonstrate their commitment to the purpose. A fundamental prerequisite for qualifying for the 501(c)(3) status is the organization's non-profit nature. Essentially, this means that any profits generated by the organization must not be used to enrich its members, directors, or officers. Instead, profits should be reinvested back into the organization to further its mission. This is not to say that employees and officers of the organization cannot receive reasonable compensation for their services. However, the primary intent should never be to distribute profits among stakeholders but to use the surplus to advance the organization's cause. The IRS has clearly defined the exempt purposes under which a 501(c)(3) organization must operate. These include charitable, religious, educational, and scientific purposes, among others. The objective of these purposes is to contribute positively to the welfare of the general public. Charitable means aiding the needy, promoting education, reducing tensions, protecting rights, and combating societal issues. To maintain their status, organizations must continually align their activities with these exempt purposes. There are certain activities that a 501(c)(3) organization is prohibited from engaging in such as participating in any political campaign for or against a candidate, excessive lobbying activities, and generating revenue through activities unrelated to their exempt purpose. Violations can result in penalties, or worse, revocation of their tax-exempt status. Hence, it's crucial for 501(c)(3) organizations to understand and abide by these restrictions to maintain their status. The first step in applying for 501(c)(3) status involves determining whether your organization is eligible. This requires that your organization is operated for one or more exempt purposes, does not distribute profits to benefit any individual, and refrains from engaging in prohibited activities. Once an organization deems itself eligible, it can proceed to prepare the application. However, if there are any areas of concern, it may be beneficial to seek legal counsel or consulting from a tax professional. The next application step is filling out either Form 1023 or Form 1023-EZ for tax-exempt status. Form 1023 is a comprehensive form that requires detailed information about the organization's structure, governance, finances, operations, and more. On the other hand, Form 1023-EZ is a shorter, less complex form that is only available to smaller organizations with less than $50,000 in annual gross receipts and $250,000 in total assets. Once the appropriate form is filled out, organizations must gather the necessary supporting documents. These include the organization's articles of incorporation, bylaws, and a detailed description of its activities, among others. These documents help the IRS understand the structure, governance, and operations of the organization. In addition, financial data, including projected budgets for the current year and the next two years, detailing the sources of income and planned expenses, should also be prepared. After the application form is completed and the necessary supporting documents are gathered, the application can be submitted to the IRS. A user fee must also be paid at the time of submission, the amount of which is determined by the organization's gross receipts. Once submitted, organizations can expect to wait several months for the IRS to review the application. During this time, the IRS may request additional information to help make its determination. After the application submission, the organization must wait for the IRS to review the information provided and make a decision. This process can take several months, depending on the complexity of the application and the workload of the IRS. The IRS will either grant the 501(c)(3) status, ask for additional information, or deny the application. If granted, the IRS will issue a determination letter officially recognizing the organization's tax-exempt status. In case of denial, the organization has the right to appeal the decision. Recognized organizations are exempted from federal income tax on income related to their exempt purpose. This can be a substantial benefit, allowing more resources to be allocated toward fulfilling the organization's mission. In some cases, 501(c)(3) organizations may also be eligible for state and local tax exemptions. These can include exemptions from sales tax, property tax, and other local taxes. Donors can deduct their contributions to these organizations on their federal income tax returns, making it more attractive for them to contribute. This benefit not only applies to individual donors but also to businesses and corporations. Many foundations and government agencies limit their grant funding to organizations with this status, as it ensures that the funds will be used for a public purpose and not for private benefit. Being able to access these sources of funding can provide significant support for an organization's programs and services. Obtaining the 501(c)(3) status can be instrumental in an organization's growth and sustainability. Once an organization has been granted 501(c)(3) status, it must comply with several reporting obligations. The most significant of these is the requirement to file an annual information return with the IRS. The specific form to be filed depends on the organization's size and type. Most organizations will need to file Form 990, Form 990-EZ, or Form 990-N, also known as the e-Postcard. This form provides information on the organization's activities, governance, revenue, expenses, and other relevant information. 501(c)(3) organizations are also required to maintain detailed records. These include a record of all income and expenses, a record of all grants and contributions received, and records relating to any employment taxes the organization may owe. Keeping these records is not only crucial for tax purposes but also to demonstrate the organization's financial responsibility and transparency. This can be especially important when seeking donations or grants, as funders often want to ensure their contributions are being used responsibly. Another responsibility of 501(c)(3) organizations is to make certain documents available to the public. This includes the organization's application for tax exemption and its annual information returns for the past three years. These disclosure requirements are intended to promote transparency and accountability in nonprofit organizations. They allow the public to see how the organization is operating and how it is using its resources to fulfill its mission. One of the primary grounds for revocation of 501(c)(3) status is non-compliance with the requirements and obligations of being a tax-exempt organization. This could include failure to file annual returns, engaging in prohibited activities, or failure to meet public disclosure requirements. It is essential for organizations to understand these obligations and to have procedures in place to ensure they are met. Regular reviews and audits can also be helpful in identifying and addressing any potential issues before they result in the loss of tax-exempt status. Significant changes in an organization's structure or operations could also lead to revocation of 501(c)(3) status. This could include changes in the organization's purpose, the way it generates income, or how it distributes its resources. If substantial changes are planned, it's advisable for the organization to seek professional advice to understand the potential implications for its tax-exempt status. 501(c)(3) organizations are non-profit entities that serve public interests and are granted tax-exempt status by the IRS. To qualify for this status, organizations must operate for exempt purposes, refrain from distributing profits to benefit any individual, and abide by restrictions on their activities. The application process is comprehensive, requiring organizations to submit detailed information about their structure, governance, operations, and finances. Once granted, 501(c)(3) status confers significant benefits, including tax exemptions, the ability to receive tax-deductible contributions, and increased grant eligibility. These organizations must also comply with several obligations, including filing annual information returns, maintaining detailed records, and adhering to public disclosure requirements. Revocation of 501(c)(3) status can occur due to non-compliance or significant changes in the organization's structure or operations. What Is an IRS 501(c)(3) Organization?

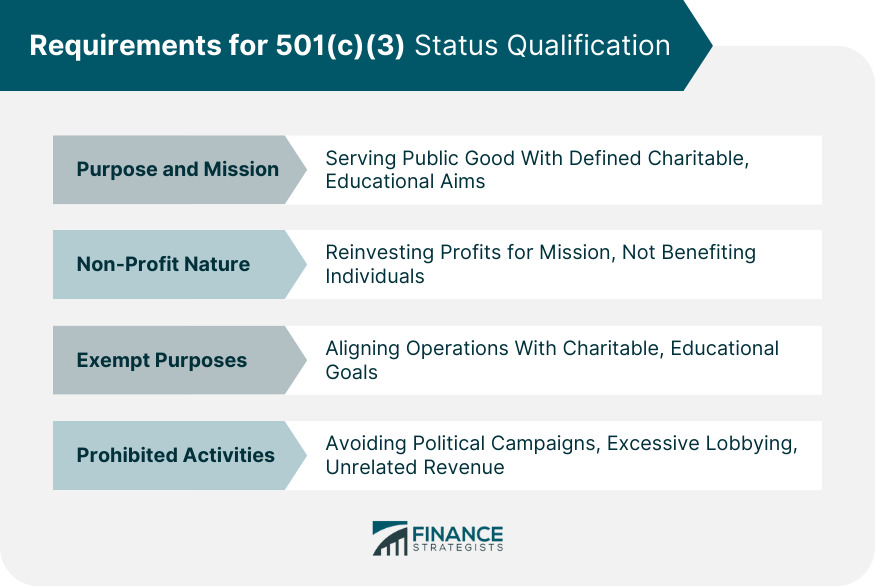

Requirements for 501(c)(3) Status Qualification

Purpose and Mission

Non-Profit Nature

Exempt Purposes

Prohibited Activities

501(c)(3) Organization Application Process

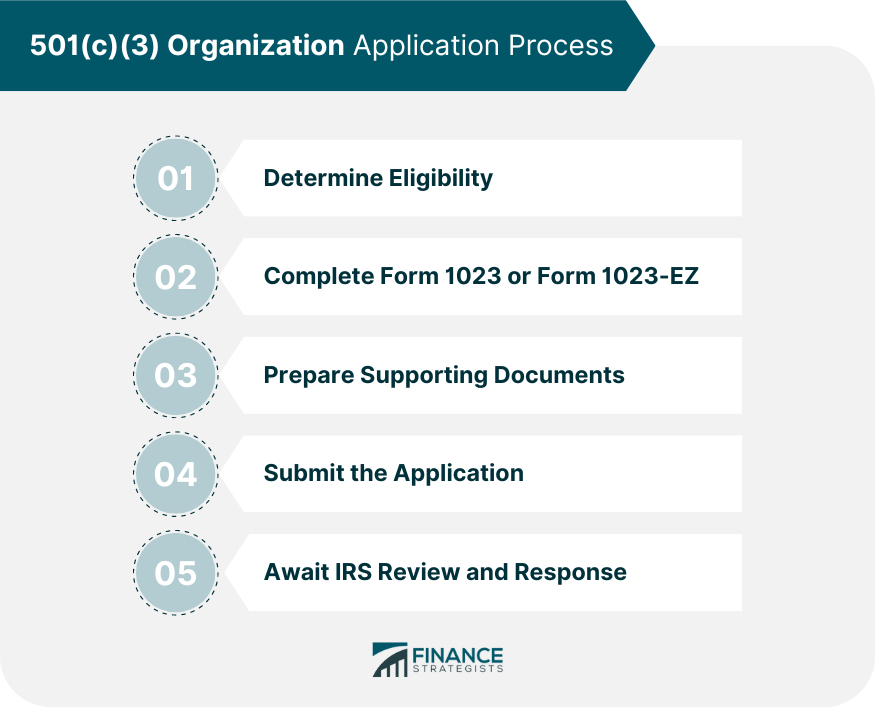

Determine Eligibility

Complete Form 1023 or Form 1023-EZ

Prepare Supporting Documents

Submit the Application

Await IRS Review and Response

Benefits of IRS 501(c)(3) Status

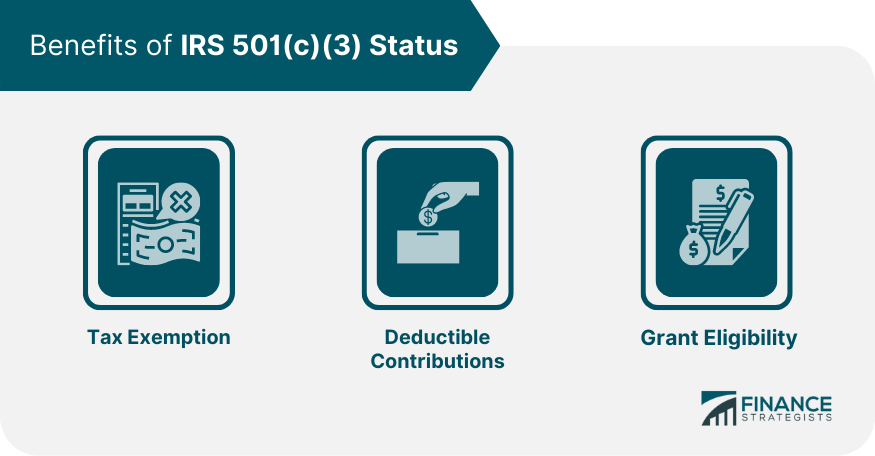

Tax Exemption

Deductible Contributions

Grant Eligibility

Compliance and Reporting Obligations

Annual Information Returns

Recordkeeping and Documentation

Public Disclosure Requirements

Grounds for Revocation of 501(c)(3) Status

Non-Compliance

Substantial Changes

Conclusion

IRS 501(c)(3) Organizations FAQs

A 501(c)(3) organization is a non-profit entity that has been granted tax-exempt status by the IRS due to its commitment to serving public interests, such as education, charity, science, and literature.

The application process involves determining eligibility, completing the appropriate IRS form (1023 or 1023-EZ), preparing supporting documents, submitting the application and the requisite fee, and awaiting IRS review and response.

The benefits include federal income tax exemption, the ability to receive tax-deductible contributions, and increased grant eligibility.

They must file annual information returns, maintain detailed records, and comply with public disclosure requirements.

Non-compliance with requirements and obligations, engaging in prohibited activities, or substantial changes in the organization's structure or operations could lead to revocation of its 501(c)(3) status.