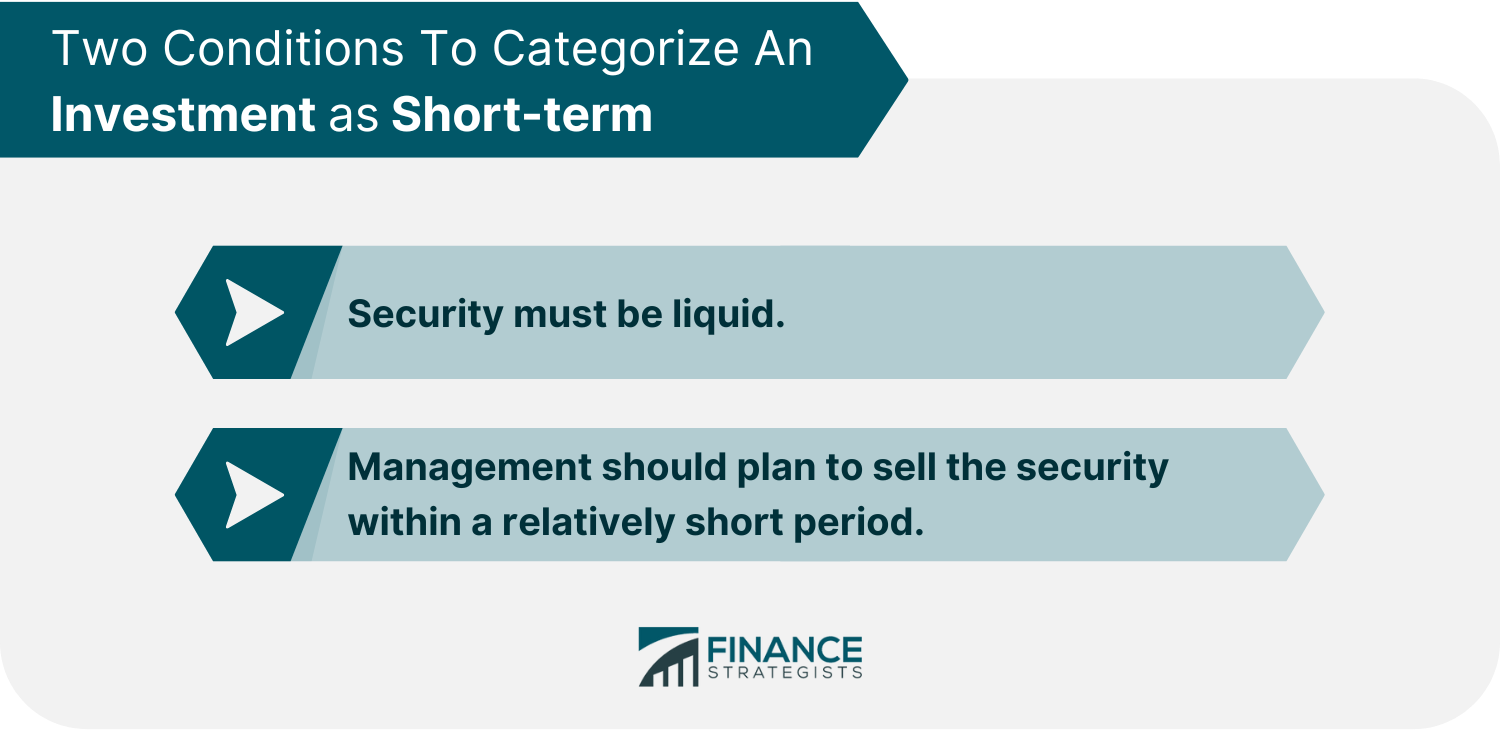

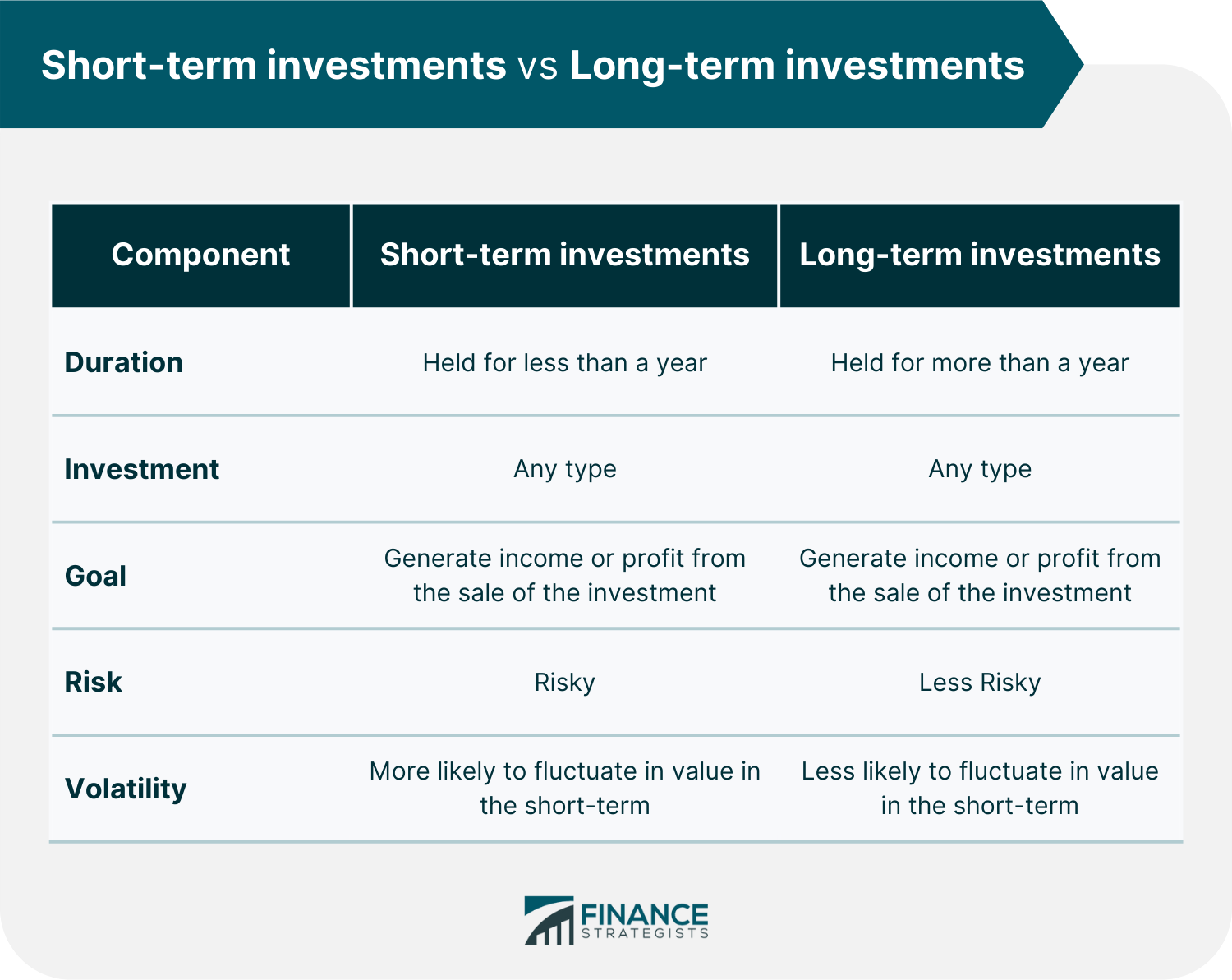

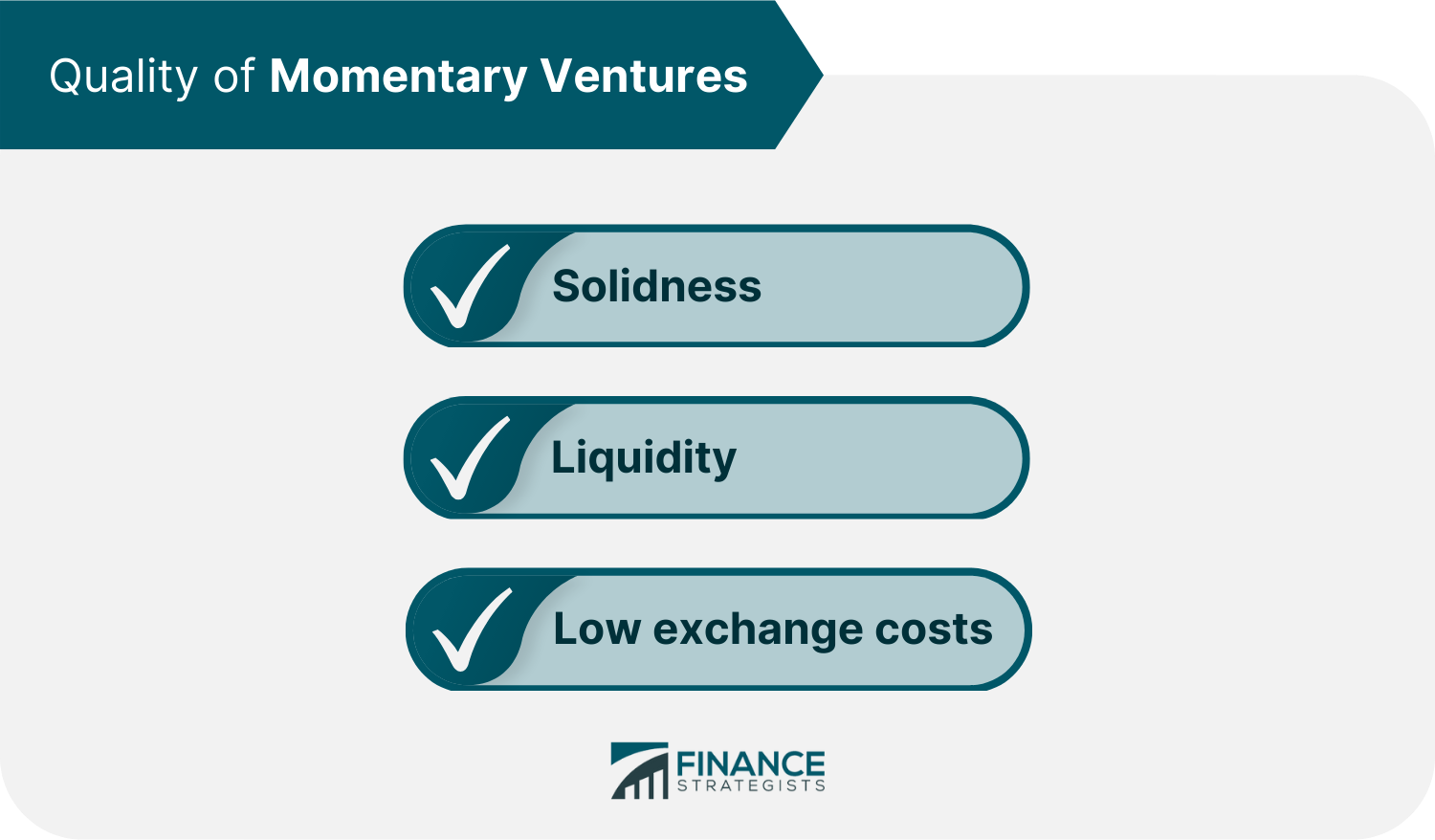

Transient speculations, also called short-term investments, are those that are made for a brief period of time with the expectation of earning a quick return. Many people view these types of investments as high risk because they are generally more volatile than longer-term investments. However, there are some strategies that can help mitigate the risk involved with transient speculations. Short-term investments are a necessary part of any financial portfolio, but they should never be your only strategy. There are several reasons why you should consider short-term investment strategies, but you need to know how to balance them with long-term investments. Momentary ventures can be a great way to get started investing because they allow you to buy and sell quickly, which means that you will get more practice trading and learning about the market. You can also make a profit on short-term investments when the market goes up or down quickly, and this allows you to make some money while you wait for long-term investments to pay off. However, it is important not to get caught up in the excitement of making a quick buck. Many people feel like they have missed out on something when they do not make a profit right away, but this is not always true. There are many different short-term investment strategies, so it is important to do your research and find one that best suits your needs. It is also important to remember that no investment strategy is without risk, so you should always consult with a financial advisor before making any decisions. The goal of a short-term investment for both companies and individual or institutional investors is to preserve capital while also generating an income like a Treasury bill, mutual fund, or similar benchmark. Organizations with a solid financial position will have an investments account on their balance sheet. This allows the organization to affordably invest extra money in stocks, bonds, or cash equivalents to earn a higher interest rate than what can be gained from a standard bank account. Two primary conditions must be met for an organization to categorize an investment as short-term. Firstly, the security must be liquid, meaning it can be bought or sold quickly and without affecting the price. For example, a stock listed on a major exchange that trades frequently or U.S Treasury bonds would meet this criterion. Secondly, management should plan to sell the security within a relatively short period–such as one year. Short-Term investments also include debt securities with maturities of one year or less–like U.S Treasury bills and commercial paper. Attractive value defenses protect against speculations in common and preferred equities. Corporate securities, for example, are securities issued by another firm that have short maturation periods and must be readily converted to be considered liquid. Unlike long-term investments, which are held for a period of at least one year, short-term investments are purchased knowing they will be rapidly sold. People who do not have immediate plans for their money (such as purchasing a car or a house) can also utilize long-term investments. Intermittent speculations may be used to help a financial backer build a portfolio. Even though they offer lower paces of return than putting money into a record store over the long term, they are highly fluid speculations that give financial backers the flexibility to bring in cash they can withdraw quickly if necessary. Businesses do not consider long-haul ventures as profitable until they are sold. This means that companies who choose to invest in short-term ventures experience changes in value at the market rate. So if a short-term investment decreases in value, the company sees it as a loss on their profit statement. Transient speculation profits are looked at simply as a pay articulation. Transient firms are more likely to succeed than long-term enterprises. They are also safer, making them ideal choices. Transient ventures help to expand your income sources in case of market unpredictability. Generally, speculative investments tend to have lower rates of return. A decline in the value of a one-time project will rapidly influence a company's overall profit. Standard business ventures and procedures used by both businesses and individual investors include: Declarations of deposit (CDs): These are deposits made with banks that commonly have higher interest rates since they secure money for a specified period. These periods usually range from as long as five years. They are FDIC-guaranteed for up to $250,000. Currency market accounts: Returns on these FDIC-guaranteed records will exceed those on investment accounts, but you will need to wager a minimum amount of money. It is important to remember that securities held in a currency market differ from ordinary assets, which are not FDIC-insured. Depositories: There are various officially sanctioned securities, such as bonds, notes, floating rate notes, and Treasury Inflation-Protected Securities. Security reserves: Expert resource managers/speculation firms offer these assets, which are ideal for a shorter time frame and can provide above-average profits. Simply be aware of the costs. Metropolitan securities: These are securities such as those offered by local or state governments, can sometimes provide greater returns and tax benefits since they are often exempt from personal taxes. Shared (P2P) lending: Excess money can be put into play through one of these loaning stages, which matches debtors to lenders. Roth IRAs: These can offer people a lot of flexibility and different investment options. You can withdraw your contributions (but not the earnings) from a Roth IRA without penalty or charges. If you have more money than you need, it might be better to pay off debts with high-interest rates instead of investing in safe but low-return short-term investments. If you have more money than you need, it might be better to pay off debts with high-interest rates instead of investing in safe but low-return short-term investments. Here's an example of a short-term investment: In its quarterly explanation dated April 21, 2022, Microsoft Corp. stated that its accounting report held $92.2 billion in momentary ventures. The central portion was U.S. government guarantees, which were $78.4 billion in total. This was followed by corporate notes/securities worth $11.7 billion, contract/resource upheld protections of $590 million, unknown government securities worth $501 million, civil protections of $269 million, and testaments of the store (CDs) at $2 billion. The best options for temporary investments include short-dated CDs, currency market accounts, high-return investment accounts, government securities, and Treasury bills. Check their current interest rates or rates of return to find which is best for you. Where Can I Store My Monies for an Extended Period? A few typical momentary speculation vehicles are half-year CDs, currency market accounts, high-return bank accounts, government securities, and Treasury bills. Financial contributors will evaluate this question in light of involvement and risk tolerance. Nonetheless, many financial experts will advocate that you should invest $5,000 in a common asset or trade exchange institution that tracks the S&P 500 and keeps it for the long run. People who have just a little money have an abundance of options. They can put their money into any gambles that do not require a firm base equilibrium, such as certain investment accounts, small portions of a listed asset, or significantly cheaper equities, bonds, and CDs. Transient investments are excellent options for both individuals and businesses who want to find a balance between liquid and stable assets to grow their wealth. The choices are plenty: from CDs to bonds and high-yield savings accounts, it is simply up to each investor to do their research. If you want to save money for the present moment, you are probably seeking a safe location to keep money before you intend to access it not too far in the future. The unstable business sectors and recession have compelled numerous financial investors to retain cash as Covid's emergency was put off, and the economy continues dealing with an inundation of growth. Although momentary ventures come with less risk, they also have the potential to miss out on better earnings in the long run. So by investing your money in a safer short-term venture, you can ensure that you will have cash when you need it instead of gambling it on a potentially risky investment. Therefore, security is the first thing investors should look for in short-term investments. If you are making momentary speculation, it is usually because you want the money ready by a specific date. The cash should be available if you are putting something away for an initial payment on a house or a wedding, for example. Transient speculations are those made in less than three years. If you have a longer time horizon—at least three to five years, if not longer—stocks are an option. They offer the potential for much higher returns. Generally, the stock market has risen about 10% yearly for extended periods. However, it can be very unpredictable. So a longer timeframe allows you to determine the good and bad times in the stock market. Transient speculations are safe, but they have lower returns. Transient speculations have some severe drawbacks: you will not likely make as much in a short investment as you would in a long one; and if you are investing for the short term, your choices will be limited to less risky options like bonds, rather than more volatile ones like stocks. (But if you can invest for the long haul, that is when buying stocks makes sense.) Transient speculations do have a few advantages, after all. They are generally highly fluid, so you may obtain your money at whatever time is most convenient for you. Furthermore, they will frequently be less dangerous than long-haul projects, with restricted disadvantages or perhaps no drawbacks. Here are a couple of the most incredible short-term opportunities to consider that might return some money. 1. Accounts with high returns on investments Compared to holding cash in an account, which typically accrues little to no interest, investing in a high-return investment account at a bank or credit association is a much better option. The latter will steadily pay dividends into your account. Savers should look closely at high-return investment accounts from different banks to find which offers the best interest rates and terms. Risk: Savings accounts are protected by the Federal Deposit Insurance Corporation (FDIC) and the National Credit Union Administration (NCUA) at banks and credit unions so that you won't lose money. For now, there is not much of a gamble to these records; nevertheless, financial sponsors who keep their cash for more extended periods may have problems keeping track of growth. Liquidity: Savings accounts are highly flexible, and you may add money to the report anytime. Banks can typically only make a maximum of six charge-free transfers or moves per explanation cycle, regardless of the circumstances. (The Federal Reserve currently allows banks to postpone this requirement.) You should be looking for banks that charge fees for keeping up with the record or accessing ATMs so that you can minimize them. 2. Transient corporate security reserves Corporate securities are stocks or debt bonds issued by large companies to raise funds for their operations. They are usually seen as safe and pay interest at regular intervals, such as quarterly or semi-annually. A security reserve is a collection of corporate securities from different organizations, often across various industries and company sizes. This diversification means that one poorly performing bond will not hurt the overall return on investment. The security asset will pay interest periodically, typically monthly. Risk: Because the public authority does not guarantee a corporate security store, it may lose money. However, bonds will typically be relatively safe, especially if you buy a comprehensive range of them. Furthermore, a momentary asset provides the slightest degree of danger and openness to changing loan costs, so increasing or declining rates have little impact on the asset's price. Liquidity: A brief corporate security store is very fluid and may be traded on any day the financial sector is open. 3. Accounts in the currency market Currency market accounts are investment accounts that typically pay a higher interest rate than regular savings accounts but usually require a higher minimum investment. Risk: Make sure you choose an FDIC-insured currency market account to protect your record from losing money. Each contributor's aggregate investment limit for each bank may be up to $250,000. With currency market accounts, the real gamble for investors occurs over extended periods. That is because these types of investment vehicles typically have low loan costs. As a result, it can be difficult for backers to keep up with growth. However, this is not currently a primary concern. Liquidity: Money market accounts are very liquid, yet government regulations sometimes impose certain limitations on withdrawals. 4. Cash in the executive's accounts The money from the executive's account allows you to invest in various short-term investments and acts like an Omnibus account. With most cash management accounts, you can often deposit, write checks on the account, transfer money, and do other banking activities. Robo-advisors and online brokerages usually offer these kinds of cash management accounts. So, the executive's account contains a significant amount of flexibility. Risk: Because the executive's accounts are frequently invested in low-yield currency market reserves, there is little risk. Because of some Robo-consultant accounts, these foundations store your money in FDIC-insured companion banks. Double-check that you do not go over FDIC storage limits if you already work with one of the associate banks. Liquidity: The executive's bank accounts are quite liquid, and cash may be removed at any time. They may surpass typical reserve funds and currency market accounts in terms of month-to-month withdrawals because they limit withdrawals to only once a year. 5. Momentary U.S. government security reserves Government securities are very similar to corporate securities, with the main exception being that they are issued by the United States federal government and its agencies. The buyers of these securities invest in speculation vehicles like T-bills, T-bonds, T-notes, and mortgage-backed securities from governmental organizations such as the Government National Mortgage Association (Ginnie Mae). These bonds are considered relatively safe investments. Risk: Although the FDIC does not back United States government securities, the Treasury promises to repay cash for these bonds. Because they are supported by the complete confidence and credit of the United States, these bonds are considered extremely safe. An asset secured by momentary securities implies that the financial backer takes on a low measure of loan fee risk. So, interest rates rising or falling will not affect the price of the asset's securities. Liquidity: Government securities are highly traded and liquid assets. They can be bought or sold any day the stock market is open. 6. Punishment-free policies in stores A no-punishment statement from the retailer, or CD, lets you avoid the usual bank fee if you withdraw your CD before it matures. CDs are readily available at your bank and typically offer a higher yield than other bank assets, such as bank accounts and currency market accounts. CDs are time stores, which implies you agree to keep money in the record for a pre-determined length, ranging from weeks to years, depending on the development you require. The bank will offer you a more significant lending expense in return for this security. The bank regularly pays revenue on the CD, and at the end of the CD's term, the bank will give you back your original investment plus any earned interest. A no-penalty CD could also be appealing when rising interest rates because you can withdraw your money without paying a fee and then invest it elsewhere for a higher return. Risk: CDs are FDIC-insured, so your money is safe. Short-term CDs have limited risks, but one gamble is that you might miss out on a better rate elsewhere while your cash flow is restricted in the CD. If the interest rate is too low, you could also lose purchasing power to inflation. Liquidity: CDs are not as liquid as other bank ventures, but a no-penalty CD allows you to avoid the fee for finishing the CD early. So you can bypass the critical component that makes most CDs illiquid. 7. Treasury Treasuries are categorized into three categories: T-bills, T-notes, and T-bonds. They offer a guaranteed return on investment, backed by the AAA credit score of the United States government. Therefore, rather than investing in a government securities fund, you could choose to invest in specific bonds depending on your needs. Risks: The FDIC does not cover individual securities, but rather the public authority's guarantee to reimburse the cash; therefore, they are considered highly secured. Liquidity: You can trade U.S. government securities on any day the market is open, and they are some of the most liquid (easily traded) securities available. 8. Currency market-shared reserves Avoid muddling a shared asset with a currency market account. While the exact name calls them, they come with various risks, but both are excellent transient speculations. A common currency market asset invests resources in things like Treasuries, civil and corporate obligations, and bank obligation protection. Furthermore, because it is a shared asset, you will pay a fee based on the firm that manages it. Risks: Although much of its speculation is insured, currency market reserves are not as secure as currency market accounts, which are FDIC-insured. In contrast, currency market assets may lose money frequently just when the market is undergoing severe difficulties, but they are relatively safe for the most part. In any case, they are the safest investments available and should protect your funds. Liquidity: With a money market shared reserve, you have reliable access to your cash and can withdraw it as needed. Although this account allows you to write checks against the assets, there is usually a limit of six monthly withdrawals. When you need money and are unsure where to invest it, possible interest rates come with a certain amount of risk. High-yield investment funds, currency market accounts, and cash-the-board accounts all yield around 1.2 percent annually and are low risk because they are FDIC-insured. Treasuries and security reserves are among the safest investment options, with CDs 2.5 percent or higher being the most secure and corporate security reserves slightly less. CDs, bonds, and other securities with a term of three to five years (or more) are usually acceptable. They're preferable to stocks because they provide stability and income; however, they can be extremely risky depending on how long you invest. 3.0+ percent of CDs (or much more if you put assets into stocks), and bonds are somewhat okay compared with stocks. What are the qualities of a good transient venture? Momentary enterprises may have a lot of things in common on an abstract level, but the three following traits generally characterize them: Solidness: Good short-term investments do not fluctuate in value as much as stocks and bonds do. The money will be there when you need it and is often insured by FDIC protection or a government guarantee. Liquidity: A decent momentary venture, in most cases, has high liquidity, which means you can get your hands on the money quickly and invest it. You will know when cash is available, and you can always reclaim your CD, except if you choose a no-punishment CD. Low exchange costs: An excellent short-term investment should not cost much money to get into or out of, unlike a house, for example. That is especially important when yields on short-term investments are at historic lows. These figures suggest that your money will not be at risk and accessible when you want to use it, which is one of the significant incentives for momentary speculation. On the other hand, you can earn a better return on long-term speculations, but keep in mind that there is more short-term unpredictability. You could need to sell all of your holdings at an inopportune time to get to that cash if you want it. If you are putting away money for a long or short time, you will need an unexpected cycle compared to if you were money management over the course of many years. Make your expectations clear. Because transient ventures have a lower potential return than long-haul ones, you must adequately establish your preconceptions. Prioritize your well-being. Usually, if your money is for immediate use, you should focus on security instead of return. Your cash should be accessible when you need it. Sometimes, the additional risk might not be worth the potential return. With many investments only yielding a small profit, it can be tempting to try to make more money by taking on more risks. But remember why you are successful in financial planning right now, and focus on that. Choose speculation depending on your demands. You might get a few more bucks on that CD, but suppose you want to withdraw cash before it doubles. Change your speculation type to match your needs. Some momentary speculations are better than others. The FDIC backs bank products, so you will not lose any money. However, market-based items, even safe ones like cashier's checks, could decline in value over short periods. Understand the risks of your investment options before making a decision. Transient speculations are typically sheltered, especially when compared to longer-term projects like equities or stock assets. Whatever you do, be sure you know what you are getting yourself into. Publication Disclaimer: Before making any investment decisions, all potential investors are encouraged to research the venture and consider if it is right thoroughly. Additionally, investors should keep in mind that past performance is not indicative of future success. Assuming you have gotten rid of your Visa obligations and have extra funds left over after paying your high-need bills, the next stage for you should be to save and grow your money. With the many choices available in today's financial world, it can be hard to know what kind of bank account you should use and when is the right time to start saving. It is tough to predict when or why you will need your money. Buying a house, saving for children, and returning to graduate school are all big choices that could use up your savings. According to Bridget Todd, head of mentor development at The Financial Gym, you should "by and large, ponder your objectives and separate them into classes given period." Doing so will help you best allocate any extra money you may have. Below, CNBC Select interviewed Todd and The Financial Gym organizer Shannon McLay about how to set up your investment funds, both now and as you approach retirement age. When you have a savings account with three years of living costs and your debt is paid off, you are in a great financial situation to do more with your money. After you have decided how much to save and what records to utilize, you should first figure out precisely what you require every day, according to McLay. Each success, dream, or want has a cost you can plan for. She asks, "Do you require a reserve of motion? Is it possible that you will marry someone? Do you wish to buy a property in 5 or 10 years? Do you want a tattoo?” She inquires about your objectives, implying that they might have altered durations. “Tattoos can be quite a financial investment,” McLay, an expense often disregarded by recent college graduates alongside other costs such as egg freezing and pet ownership. Suppose you are saving money for goals that will take place within the next two years, keep it in a generally safe record, such as a high-return investment account that earns interest at 1% per year. To have it when the opportunity comes, open a Marcus by Goldman Sachs High Yield Online Savings or an Ally Online Savings account and link it to your financial records. If your objectives are a long way in the future, think about financial planning with an investment fund. It involves more risk, but it might be worth taking a chance since you won't need the money immediately. There are many types of investment funds and investment portfolios. Generally speaking, lower-risk portfolios yield predictable but slower growth. Higher-risk portfolios offer the potential for high returns, but you could also lose money as the market fluctuates. A high-yielding bank account is the safest since your money is not put into the financial exchange, yet it offers 16x more premium than the public standard. When you feel you are ready to take more risks with your money, look for a financial firm or Robo-advisor that works best for your lifestyle and personality. “Do you want to be more hands-on when managing your investments, or would you prefer to set it and forget it?” asks McLay. Acorns, for example, is an essential app that connects to your financial data. Loose coinage may be generated through programs like Acorns, which connect to your financial records and add loose change. Betterment and wealth front are Robo-consultants that allow you to choose the length of time for your reserve funds goals and how much risk you want to take on before you can set up a constant sum to contribute. Rates for financial counselors are usually lower (about .01% to .25% of your income) than expert monetary advisors, who charge no less than 1%. Ellevest, for example, charges enrollment costs rather than a percentage of your earnings. To take on a greater percentage of the duty yourself, you can open a money market fund with E*Trade, Fidelity, Charles Schwab, or Vanguard. “They are a bit more of a task,” says McLay. When you put assets into a portfolio that includes stocks and bonds, there is more gambling when you own a greater quantity of stocks. Stocks are generally more volatile, while the security market is usually a modest risk. In any event, you should not be alarmed by the gamble, according to McLay: “If your aim is over two years away, you can anticipate both good and bad market cycles.” Knowing this, you may put your money in different pails based on the distance between each goal and how much risk you are willing to take. Contribution for medium-term objectives (six to ten years) should be less hazardous than long-term financial planning for retirement (more than ten years away). Todd includes the following diagram to help illustrate his point: Over the course of the next two years, keep cash reserve funds in an open bank account for any life achievements that come up. This way, Todd, you will not have to wait for the stock market to help you. You may withdraw your money at any time without worrying about additional desk work or the market's return. Although using a high-return investment account with financing costs of around 1% will not give you the highest possible return, you should be open to seeing your funds returned in a secure, FDIC-insured account. Assuming you know you will need your money in three to five years, consider putting it in financial exchange, but more securely. “You should keep at least 40% of your portfolio invested in bonds,” Todd states. “Throughout this period, you must be very conservative in placing objectives. Be that as it may, you must take a step forward to enhance returns,” Todd adds. Todd typically suggests a portfolio containing at least 75% stocks for investment goals in this time frame. Having 25% of the portfolio in bonds helps mitigate some risks while still allowing you to pursue your objectives. According to Todd, long-term goals such as retirement require a powerful component (at least 90 percent in equities), which makes sense because the financial market has generally increased every seven to ten years. “To make the most of your extended projects, you should go heavy on equities,” she explains. The primary worry/problem. “There is a lot of life left before you retire,” McLay adds. “Between now and 59 and a half, a lot of expensive things can happen.” Additionally, it is crucial to remember that contributing can help you afford them. You will be the most successful in developing your wealth when you have a combination of accounts that are both high and low accounts and a mixture of short-term and long-term goals you are working towards. When it comes to investing, there is no one-size-fits-all approach. Different types of accounts offer different pros and cons, so it is important to consider what will work best for you and your individual circumstances. Short-term investments are typically less risky than long-term investments, but they also tend to have lower returns. If you are investing for a short-term goal, it is important to find an investment that is safe and has a reasonable return. Investing in a long-term goal such as retirement requires a different approach. Long-term goals generally require more risk, but they also have the potential for higher returns. If you are investing for a long-term goal, it is important to find an investment that has the potential to grow over time. The most successful investors typically have a mix of short-term and long-term goals and a mix of high-risk and low-risk investments. This gives them the flexibility to weather the ups and downs of the market and still make progress towards their goals. Investing is a personal process, so it is important to find an approach that works for you. If you are not sure where to start, seek out the advice of a financial advisor. A financial advisor can help you assess your goals and find an investment strategy that is right for you.Best Short-Term Investment Strategies That You Should Not Ignore

How Do Short-Term Investments Work?

Short-Term Investments vs Long-Term Investments

The Pros and Cons of Short-Term Investments

Professionals

Drawbacks

Short-Term Investments Instances

Protections

What Are the Most Profitable Short-Term Investments?

How Can I Make the Most Out of My $5,000 Investment?

What Can You Invest in for Very Little Cash?

Momentary Ventures

What Is Momentary Venture?

The Most Promising Scenarios for Transient Cash

Ways to Save Money for a Long Time or Until You Need It

Contributing Your Reserve Funds

Saving up for the Future That You Want

Where Should You Place Your Investment Money?

Contribute to Both Short-and Long-Term Goals

Short-Term (Zero to Two Years)

The Current Moment (Three to Five Years)

Medium-Term (Six to Ten Years)

Long-Term (More Than Ten Years)

The Bottom Line

Short-term Investment Strategies FAQs

Short-term investments are those that you anticipate will grow in value over a relatively short period of time, typically three years or less. Many investors choose to keep some of their portfolio in short-term investments as a way to protect against market volatility and unforeseen events.

There are a number of different short-term investment strategies that investors can use to try to grow their money. Some common approaches include investing in stocks, bonds, and mutual funds; using dollar-cost averaging; and investing in index funds.

Short-term investments can be subject to market volatility and other risks, so it is important to carefully consider your goals and risk tolerance before choosing any investment. You may also want to consult with a financial advisor to get guidance on how to best grow your money.

Some tips for short-term investing include diversifying your portfolio, staying disciplined with your investments, and being mindful of fees and expenses. It's also important to have realistic expectations about the potential growth of your investments.

Short-term investments are those that you expect to grow in value over a relatively short period of time, while long-term investments are those that you expect to hold for a longer period of time. Many investors choose to keep some of their portfolio in short-term investments as a way to protect against market volatility and unforeseen events.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.