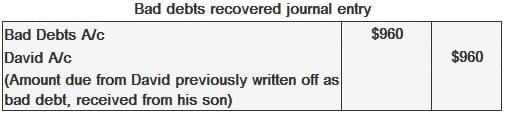

Occasionally, a business may find that an amount it had previously written off as bad debt is received at a later date. The receipt of such an amount is called the recovery of bad debts. Clearly, the amount cannot be credited to the personal account of the debtor because that account was closed down when the amount due from that debtor was written off as bad debt. The entry to record bad debt recovery would, therefore, be as follows: After this entry, the bad debts recovery account will show a credit balance at the end of the financial year and will be transferred to the credit side of the profit and loss account as an item of income. John has learned that David, who owed him $960, has passed away and left no estate behind. John decides to write off this amount as a bad debt. Task 1: Show the journal entry. Three months later, David's family member visits John to pay off the amount due. Task 2: Show the bad debts recovered journal entry.

Example

Recovery of Bad Debts FAQs

Recovering a bad debt means getting back money owed to you.

Bad debts can be written off when you stop trying to get the money back. A company may know that it will never get paid, or no longer wants to pursue payment of an account.

We would record a credit in our accounting records for the amount that we receive. We would also record a debit to bad debts for the same amount.

Recovering bad debt helps companies understand how much they may have lost during a specific time period due to uncollected Accounts Receivable. This information is vital to a company.

We would credit the cash account because we have received money from a debtor that was owed to us earlier. This is not considered income. We also record a debit to the bad debts account because we had previously written off this amount as a bad debt. This is considered an expense.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.