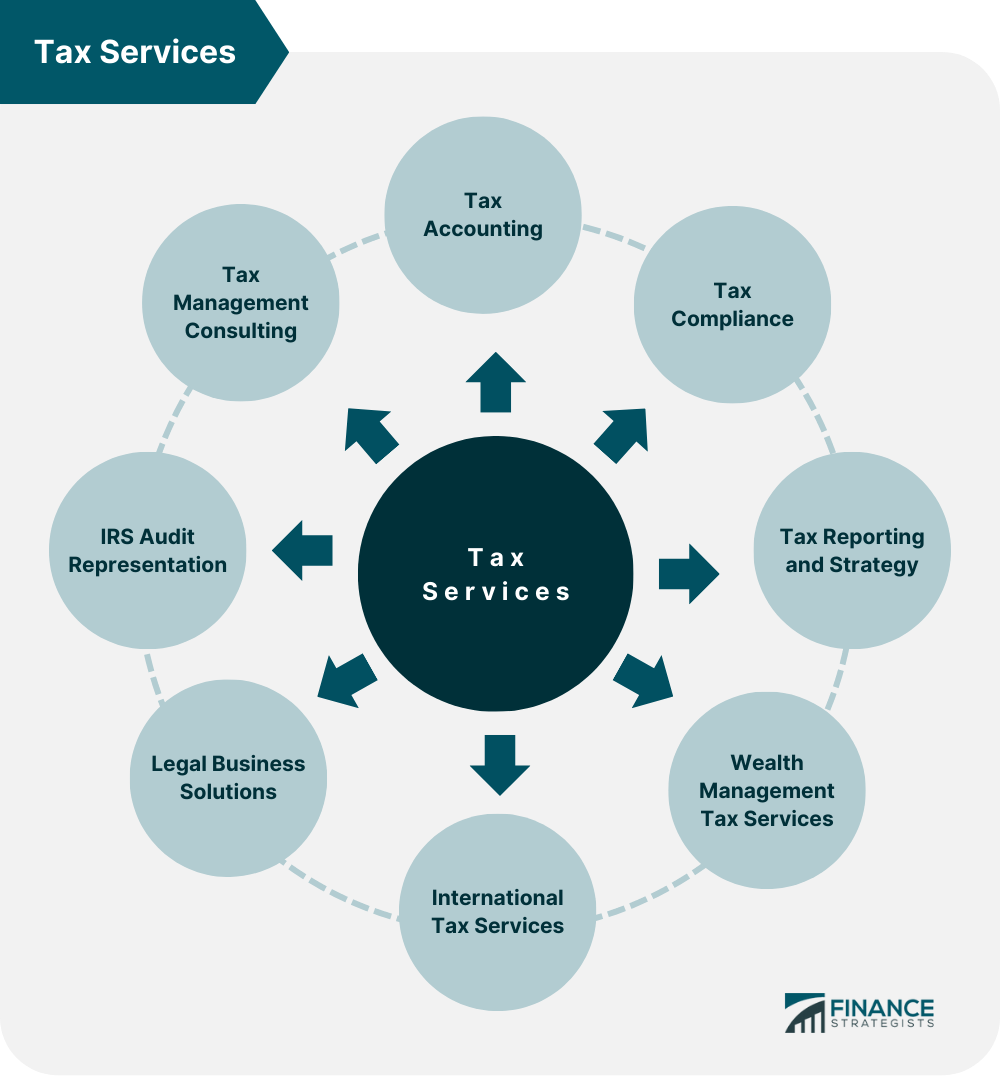

The collection and preparation of information before the deadline for tax filing is an excellent opportunity for individuals and businesses to review their current financial position and decide on their future plans. Generally, compliance with the tax guidelines of the Internal Revenue Service (IRS) can help them strengthen their financial situation. For example, they can take advantage of tax deductions and avoid paying penalties, which saves them money in the long run. However, with the ever-changing nature of the tax code, paying the right amount of taxes and filing the appropriate forms can be challenging, especially when you try it on your own. Whether you work on your taxes personally or decide to hire a professional, it is essential to be aware of the various forms of taxes that you need to consider when filing your returns: Have questions about taxes? Click here. Individuals and businesses needing help with their taxes can hire professionals to support them in various tax matters, such as the following: This type of tax service involves monitoring and recording the cash inflow and outflow of either an individual or a business. As the cash inflows and outflows grow larger, the process becomes more complicated, and the support of a tax accountant might be required. Tax compliance focuses on ensuring that companies or individuals meet filing deadlines, avoid penalties, and remain compliant with IRS guidelines. This also covers retrieving, analyzing, and consolidating the necessary tax information. This service is about helping individuals or businesses develop an effective plan to minimize taxes. It might involve analyzing the current tax rate, researching potential deductions and credits, and determining the best way to improve cash flow. This tax service type helps clients maximize their net worth by providing advice on issues relative to wealth management, such as fiduciary taxation, generation-skipping transfer tax (GSTT), charity tax, and estate tax. This service focuses on the foreign tax compliance and reporting needs of multinational businesses. It also entails understanding the latest trends in global taxation and providing advice for expanding abroad. This type of service provides clients with the legal tax-related advice they need during all stages of their business. This can include areas such as entity formation and intellectual property issues. For individuals facing an audit from the IRS, gathering evidence, responding to inquiries, and even attending the interview can be stressful. Fortunately, some IRS-authorized tax professionals can represent their clients during these proceedings. Tax management consulting provides comprehensive support for dealing with taxation, especially for complex or unfamiliar tax issues. This service can involve helping businesses at the management level identify potential areas of improvement in their operations. Today's complex tax regulations can make it difficult for individuals and businesses to meet their tax obligations independently. This is why many of them seek professional help with their taxes. Below are some of the benefits they can experience when hiring a professional tax service: Hiring professional tax services can help people avoid costly mistakes. However, when choosing a service provider, there are several factors that clients should consider: The individual or company offering tax services should have the right expertise and knowledge about the specific type of tax that needs to be handled. Someone who is updated on the current tax regulations and has years of experience in the chosen field might be the best choice. It is essential to consider if the services being offered by potential tax service providers meet all of the client’s needs. This can range from basic tax accounting and compliance to IRS audit representation or international tax services. Asking about a professional tax service’s cost structure in advance is the most effective method to avoid unpleasant surprises later on. Clients should also compare the cost of their prospects’ services before settling on a provider. A professional tax service provider should possess the right qualifications and certifications. Clients can ensure this by checking references and speaking to previous clients. This will also give them a better idea of how each prospect works. Financial information is confidential, and data breach is a serious concern. An excellent professional tax service has adequate measures to protect sensitive data. This can include tools like anti-virus software, firewalls, and encryption protocols. An excellent professional tax service should be accessible and offer timely communication. This will assure clients that their questions or issues will be addressed quickly and efficiently. A good tax service provider should offer ongoing support to keep the individual or business up-to-date with the latest changes in tax laws. They must also be willing to frequently review a client’s status and ensure compliance with any updated regulations if necessary. A Form 1040 and a state tax return with no itemized deductions cost $220 to prepare and file, whereas an itemized Form 1040 and a state tax return cost an average of $323. Self-employed individuals pay an average of $457 to complete an itemized Form 1040 with a Schedule C and a state tax return. Rates will vary if portions of the tax filings fall under special circumstances and require the tax professional more time to finish. There are certain circumstances when hiring a professional tax service is the best action. These can include the following: Individuals or businesses may lack time to prepare their taxes before the deadline. Hiring a professional can save the time and hassle which often comes with this process. If an individual or business has complex items to report, such as multiple income sources or substantial non-cash donations, it might be better to hire a professional. Circumstances like these usually complicate the tax filing process and require additional forms. Hiring a reliable tax professional assures clients that they are filing correct information while being protected from fraud and data breaches. This can provide them with a sense of security and peace of mind. With the ever-changing nature of the tax code, paying the right amount of taxes and filing the appropriate forms can be challenging, especially for businesses or individuals who attempt it independently. This is why many of them seek professional help with their taxes. Tax services are provided by professionals who specialize in the various aspects of taxes, such as tax accounting, tax compliance, tax reporting, wealth management taxes, international tax services, and IRS audit representation. Clients who hire professional tax services save time and money. They also have fewer chances of being audited by the IRS while simultaneously gaining access to expert advice that can help them with their planning. Clients should select a professional with the right qualifications, relevant experience, and a transparent fee structure when looking for a service provider to meet their tax needs. Someone accessible who offers quality services, ongoing support, and data security is also preferred. Enlisting the help of a professional, such as a tax accountant, is important when clients have limited time to meet the deadline, are anticipating complex returns or if they value security.Understanding Tax Information

Tax Services

Tax Accounting

Tax Compliance

Tax Reporting and Strategy

Wealth Management Tax Services

International Tax Services

Legal Business Solutions

IRS Audit Representation

Tax Management Consulting

Benefits of Hiring Professional Tax Services

What to Look for When Hiring Professional Tax Services

Experience

Services Offered

Fee Structure

Qualifications

Data Security

Accessibility

Ongoing Support

Average Cost of U.S. Professional Tax Services

When Should You Hire a Professional Tax Service?

If You Are Experiencing Time Constraints

If You Are Anticipating Complex Returns

If You Value Security

Final Thoughts

Tax Services FAQs

Common tax services include tax accounting, tax compliance, tax reporting and strategy, wealth management tax services, international tax services, legal business solutions, IRS audit representation, and tax management consulting.

The average cost of filing a tax return with no itemized deductions is $220, but it costs $323 to file a return with itemized deductions. Meanwhile, self-employed individuals usually pay $457 to tax service providers to accomplish their itemized Form 1040 and attach a Schedule C.

The benefits provided by professional tax services include saving time and money, lessening the chances of an IRS audit, gaining access to expert advice, and receiving support for business planning.

Tax accounting involves monitoring and recording the cash inflow and outflow of either an individual or a business. In contrast, tax compliance focuses on ensuring that companies or individuals meet filing deadlines, avoid penalties, and remain compliant with IRS guidelines.

Clients should select a professional with the right qualifications, relevant experience, and a transparent fee structure when looking for a service provider to meet their tax needs. Someone accessible who offers quality services, ongoing support, and data security is also preferred.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.