Question 1

The MST Manufacturing Company produces one product that passes through a single process in a manufacturing cycle lasting approximately 18 days.

Therefore, there will generally be some work-in-process inventories at the end of each month.

After MST started its manufacturing operations on 1 January, the costs of production for the rest of the month are given as follows:

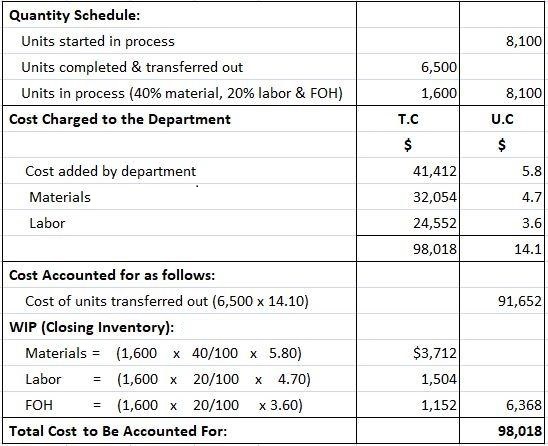

| Materials | $41,412 |

| Labor | $32,054 |

| Factory Overhead | $24,552 |

The production statistics for the month were:

| Units completed and transferred to finished goods store | 6,500 |

| Units in process (materials 40% and labor and overhead 25%) | 1,600 |

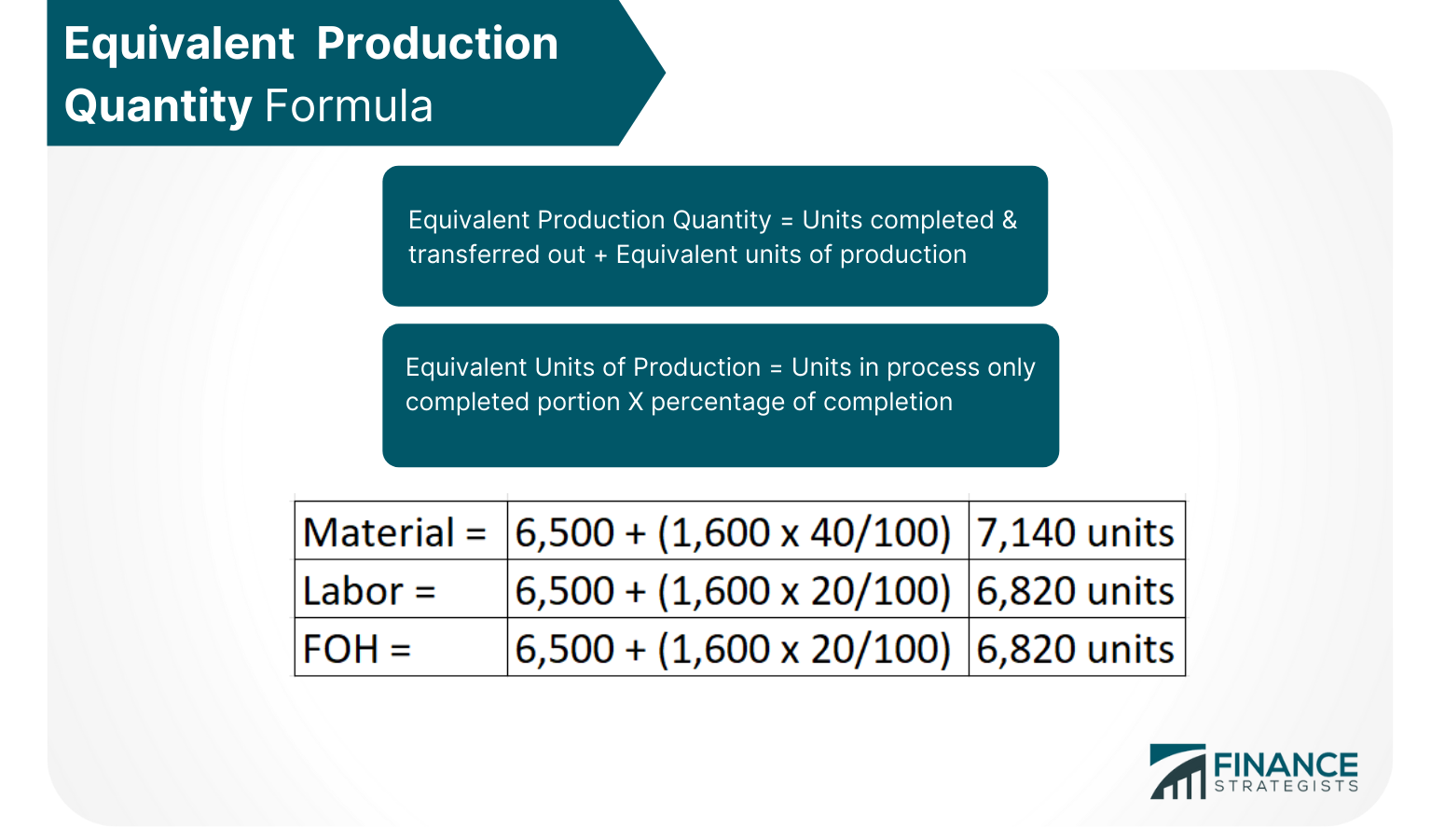

Required: Prepare a statement showing the equivalent production quantity for the month in terms of materials, labor, and factory overhead. Also, prepare a cost of production report.

Solution

MTS Manufacturing Company Cost of Production Report For the month of January 20xx

Working

Question No. 2

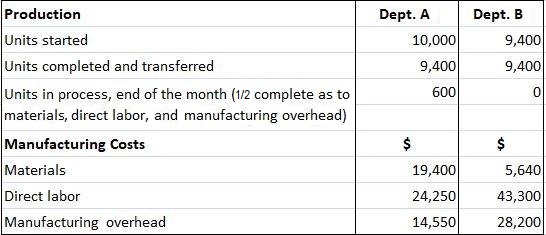

The Tuttni Corporation manufactures one product that passes through two manufacturing departments. Production and manufacturing costs for the month of April were as follows:

Required: Using the process costing system, prepare a cost of production report for the month.

Solution

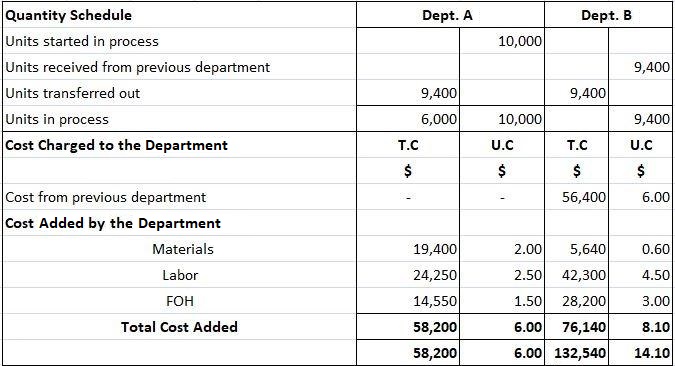

Tuttni Corporation Cost of Production Report For the Month of April 20xx

W.I.P ending inventory:

Computation

Equivalent/Effective production

Department I

Materials = 9,400 + 600 x 50/100 = 9,700 units

Labor = 9,400 + 600 x 50/100 = 9,700 units

FOH = 9,400 + 600 x 50/100 = 9,700 units

Department II

Materials = 9,400 + 0 = 9,400 units

Labor = 9,400 + 0 = 9,400 units

FOH = 9,400 + 0 = 9,400 units

Cost of Production Report (CPR) Questions and Answers FAQs

Process Costing always follows the same process while job-order costing applies to each job separately.

Job-order costing is used when there is production of a variety of products or for one time jobs. This system records costs at the time they are incurred and it is easier to have control over the job.

The cost of ending inventory in a Process Costing system is equal to the sum of all costs for units transferred out plus labor and factory overhead costs, less any materials that were released but not yet used in production. The cost of goods sold is the sum of all costs for units started and completed during the period.

A work-in-process inventory (wip) is an account that represents the cost of partially completed products. In Process Costing, the wip inventory accumulates the costs of all units that were started and completed during the period, but had not been transferred out of the department as of the end of the accounting period.

Yes, it can be used if there is only single product. However it is recommended to use job order costing for more than one product.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.