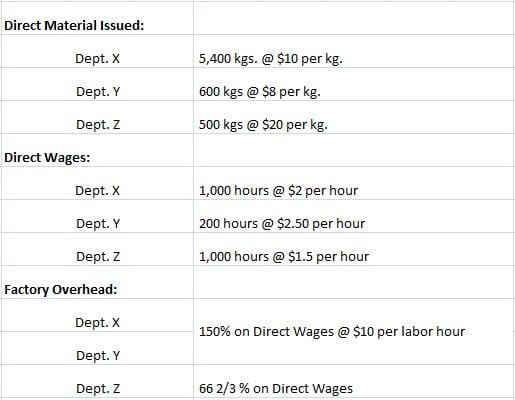

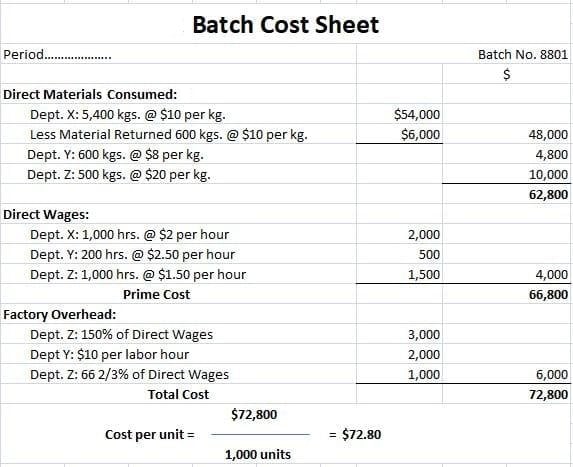

Batch costing is nothing but a modified form of job costing in which the cost of each batch of production is calculated. This method of costing is suitable for manufacturing units in which items are manufactured in definite batches. The batch costing method is also known as lot costing because products are produced in lots of, for example, 500, 1,000, or any other number. Batch costing is commonly used in the pharmaceutical industry. It is also applied in ready-made garment factories, watch factories, and production facilities for radios, televisions, and other items. Batch costing is a varied form of job costing. While job costing is concerned with ascertaining the cost of executing jobs, according to customer specifications, batch costing focuses on a group of identical products manufactured for the firm's own stock. Batch costing is generally applied to manufacture medicines, component parts of complex products (e.g., cars, scooters, computers, watches, and televisions), biscuits, food products, and ready-made garments. The products manufactured in a batch are used for a particular purpose (e.g., spare parts for composite products are to be used in a specific model only) or they are consumed within a specified period (e.g., medicines and food products). The costing procedure for batch costing is similar to that of job costing. The only difference is that a batch becomes the cost unit rather than a job. For the purpose of costing, each batch (or group of identical products) is allotted a serial number (known as a batch number), just like a job number. The presentation of the various items of cost is made in the form of a statement known as a batch cost sheet. The batch cost sheet includes the cost of any direct materials, direct labor, and direct expenses that can be directly identified with a particular batch. The share of overheads chargeable to the batch (calculated on some equitable basis) is also included. The total cost of a batch, as shown in the batch cost sheet, divided by the total number of products in the batch yields the cost per product in the batch. Cost per product in the batch = Total cost of a batch / Total number of products in the batch You are required to prepare a batch cost sheet for an engineering company showing the cost of Batch No. 8801, which contains 1,000 units. The batch passes through three departments: X, Y, and Z. The costs incurred for the batch are as follows: After the batch is complete, 600 kgs. of raw materials issued to department X are found to be surplus and returned to the storehouse.Batch Costing: Definition

Batch Costing: Explanation

Batch Costing Procedure

Example

Solution

Batch Costing FAQs

Batch costing is a modified form of job costing in which the cost of each batch of production is calculated. This method of costing is suitable for manufacturing units in which items are manufactured in definite batches.

Job costing is concerned with ascertaining the cost of executing jobs, according to customer specifications. Batch costing focuses on a group of identical products manufactured for the firm’s own stock.

The management is responsible for making out a statement of cost of goods manufactured and closing the cost ledger.

The batch cost sheet includes the cost of any direct materials, direct labor, and direct expenses that can be directly identified with a particular batch. The share of overheads chargeable to the batch (calculated on some equitable basis) is also included.

The statement of cost of goods manufactured is prepared on the basis of the total cost of the batch and the total number of products in the batch. The cost per product is computed by dividing the total cost of the batch by the total number of products in the batch.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.