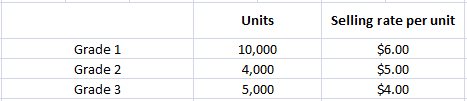

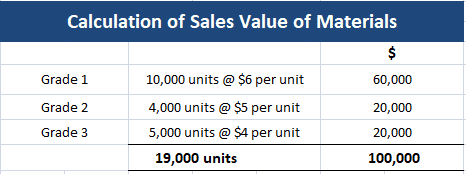

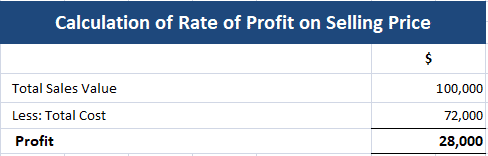

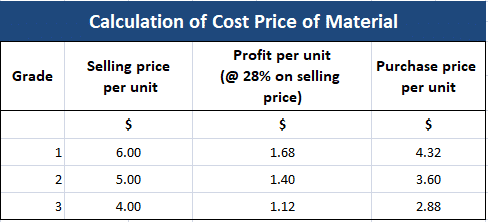

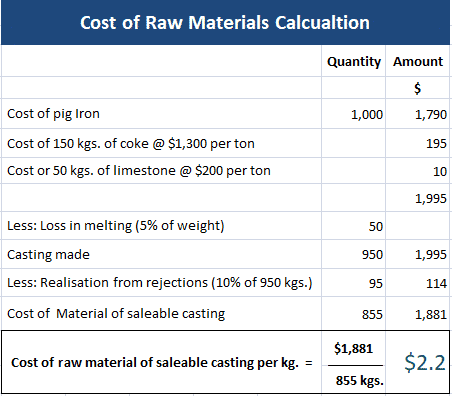

Sometimes, when materials are purchased in bulk at a single rate, there will be a mixture in terms of item quality/grade. In such cases, it is necessary to determine the proper cost of each quality/grade of the material. This process of finding the separate cost of each material is called apportionment of the joint cost of materials. The cost of the various qualities/grades is ascertained based on their selling price or market price, as demonstrated in the following example: A truckload of Material A was purchased for $72,000. The material was sorted into the following grades and market rates: Required: Calculate the purchase rate per unit of each grade of material, assuming that all grades yield the same rate of profit. Rate of profit on selling price (or sales value) = (Profit / Sales value) x 100 = (28,000 / 1,00,000) x 100 = 28% Batala Foundry melts pig iron to produce castings. Coke and limestone are used to melt the metal. 150 kgs. of coke and 50 kgs. of limestone are required to melt 1 ton of pig iron. The loss in melting is 5% and the rejections amount to 10% of the castings made. The cost of pig iron is $1,790 per ton, the cost of coke is $1,300 per ton, and the cost of limestone is $200 per ton. Rejections fetch a rate of $1.20 per kg. Required: Calculate the cost of raw materials per kg. of saleable casting.Example 1

Solution

Example 2

Solution

Apportionment of Joint Cost of Materials FAQs

As far as possible, apportionment of joint cost is avoided. It occurs when there are multiple products produced from a single raw material or process, whereby individual items have different rates of profit or loss. It is mostly done to avoid accounting for the same costs against each item individually.

The sales value of all items should be taken into consideration. Each item should reflect its fair share in the profit/loss made. It is important that excess or unnecessary costs/expenses against any one product, which have already been accounted for, are not repeated in calculating the respective product's cost.

To apportion raw material, sales value of the item with highest sales value/profit is considered as 100%. Sales values of all other items are then calculated as a percentage of this unit. This percentage is called the "apportionment rate".

The relative value of joint products affects the apportionment of costs because it determines the proportionate share of each product in the final sales price. For example, if Product A has a higher value than Product B, then a greater portion of the joint cost of materials will be allocated to Product A.

The apportionment of costs can be changed by changing the basis on which the costs are allocated. For example, if the basis of allocation is changed from weight to volume, then the costs will be allocated in a different manner. It is important to note that any changes to the allocation method should be applied consistently to all joint products.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.