Blanket Absorption Rate

Blanket absorption rate is used in relation to the recovery or absorption of overheads.

For ease and simplicity, a common absorption rate for overheads may be used across a factory for all jobs and units of production, irrespective of the department in which they were produced. This is known as the blanket absorption rate.

A common absorption rate is not appropriate when a factory has many departments, or when the jobs or units of production do not spend an equal amount of time in each department.

Such a rate should also be avoided if all the jobs or units do not pass through all the departments in the factory.

Rather than using the blanket absorption rate, the departmental overhead rate of the respective departments (calculated using the amount of overhead assigned to departments) is applied to the jobs or units of production based on the time spent in each department.

Departmental Absorption Rate

When the overhead absorption rate is calculated separately for each department in a factory, this is known as the departmental absorption rate.

It is advisable to establish separate overhead rates for each department to ensure that all jobs and units of production are charged with their fair share of overheads. This is suitable when jobs and units do not spend a similar amount of time in each department.

Example

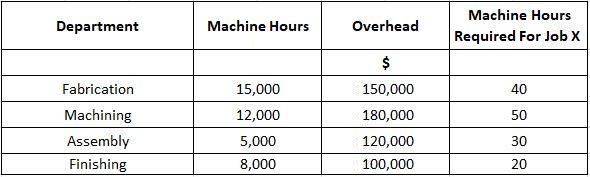

ABC Ltd. manufactures engineering components. The following budgeted information is given for 2019-20:

Required: Calculate the blanket and departmental overhead absorption rates and the overhead to be charged to Job X under both methods.

Solution

Calculation of Blanket Overhead Absorption Rate

Overhead Rate = Total Overhead / Total Machine Hours

= $5,50,000 / 40,000 machine hours

= $13.75

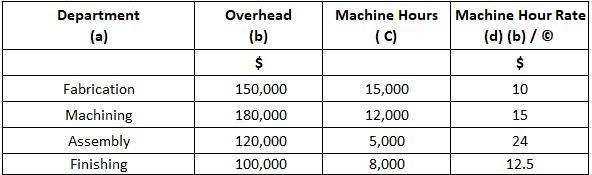

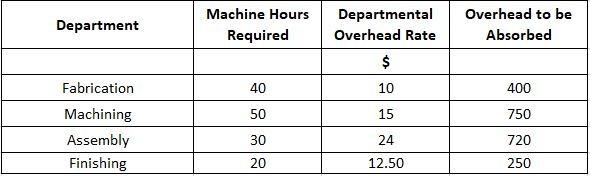

Calculation of overhead to be charged to Job X (based on the departmental overhead rate)

Calculation of overhead to be charged to Job X (based on the blanket overhead rate)

Total machine hours to be used on Job X = 40 + 50 + 30 + 20 = 140 machine hours

Blanket overhead rate = $13.75

Overhead to be charged to Job X = 140 machine hours x $13.75

= $1,925

Blanket Absorption Rate and Departmental Absorption Rate FAQs

The main difference between a blanket absorption rate and a departmental overhead rate is that the former is used when all jobs and Units of Production pass through all departments in the factory, while the latter is used when this is not the case. A common absorption rate for overheads is not appropriate when a factory has many departments, or when the jobs or Units of Production do not spend an equal amount of time in each department.

When all the jobs or Units of Production pass through all the departments in a factory, it is appropriate to use a blanket absorption rate. This is because the overhead expenses are incurred uniformly across all the departments in the factory. The main benefit of using a blanket absorption rate is that it is simple and easy to calculate.

Using a departmental overhead rate is beneficial because it ensures that all jobs and Units of Production are charged with their fair share of overheads. This is suitable when jobs and units do not spend a similar amount of time in each department. It also enables the identification of which department is responsible for incurring a particular overhead expense.

Assigning overheads to departments ensures that all jobs and Units of Production are charged with their fair share of overheads. This is suitable when jobs and units do not spend a similar amount of time in each department. It also enables the identification of which department is responsible for incurring a particular overhead expense. Allocating overheads to jobs or units refers to assigning expenses to the job or unit that causes them.

Companies may choose to alter their methods of charging overhead for many different reasons, including changes in the way the company produces its products, changes in the composition of the workforce, or changes in the level of activity.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.