DuPont Analysis Explanation

During the 1970s, DuPont Corporation developed a unique performance measurement system for its investment projects compared to other business enterprises of the time.

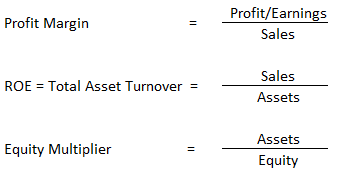

The purpose of DuPont's method is to define return on equity (ROE) based on its component parts.

As opposed to a simpler way of calculating ROE, DuPont's multi-faceted approach better detects whether and where a company has financial leverage.

From the standpoint of DuPont analysis, ROE is affected by three important components, namely:

- Operating efficiency (measured by profit margin)

- Asset use efficiency (measured by total asset turnover)

- Financial leverage (measured by the equity multiplier)

To calculate profit margin, total asset turnover, and the equity multiplier, use these formulas:

By breaking ROE into three distinct parts, investors can examine how effectively an enterprise uses its equity.

Original Form of DuPont Analysis

New asset avoidance may occur when financial accounting methods of depreciation artificially produce lower ROEs in the first year of an asset's service.

If ROE is unsatisfactory, DuPont analysis helps to locate the parts of the business that are underperforming.

Therefore, after DuPont Corporation used its new approach, it gained more importance.

DuPont analysis has since become one of the most popular measures to calculate ROE.

The theoretical concept behind DuPont analysis is that forms of ROE using net book value discourage investment in view of potentially risky ventures, which is because they underestimate the return for the first few years of investment.

The calculations in DuPont analysis seek to remedy this situation.

By breaking the ROE into profit margin, asset turnover, and leverage factors, investors can see and judge how effectively a company is using equity.

This is because poorly performing components will drag down the overall figure.

To calculate ROE using DuPont analysis, multiply the profit margin, assets higher is the return on equity. The below table gives the DuPont financial components of the DuPont model.

ROE = Profit margin x Asset turnover x Equity multiplier

Table (A) DuPont Financial Analysis Model

| Income Statement | Balance Sheet | Return on Capital Employed (ROCE) |

| Performance measure is: | Performance measure is: | |

| Profitability | Activity | Profitability x Activity |

Table (B) Financial Components of DuPont Model

| Profitability | Activity | Return on Capital Employed (ROCE) |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

Utility of DuPont Analysis

- The profit margin indicates how efficient the company's management is in operating the company and controlling costs.

- Asset turnover measures the efficiency of the company in generating sales for every dollar of assets.

- The equity multiplier shows how leveraged a company is by computing how much financing stockholders have provided for every dollar of assets.

- DuPont analysis is considered a useful tool for predicting future changes in Return On Net Operating Assets (RNOA).

- It facilitates industry group comparison as a standard measure, provided the industry groups use the same measure.

- It is an approach used to analyze enterprises by evaluating inter-relationships among multiple performance measures.

- DuPont analysis helps to identify the factors that increase profits.

- By identifying these factors, one can try to improve the efficiency of the enterprise.

Pros and Cons of DuPont Analysis

Advantages

There are several advantages associated with DuPont analysis:

- First, using DuPont analysis, investors can evaluate alternative stock investments and, in turn, compare why the ROEs of the stocks differ.

This is achieved by identifying the impact of operating efficiency, asset use efficiency, and financial leverage on ROE.

- Second, DuPont analysis helps to analyze the factors that contribute to the differing ROEs of stocks, which can guide portfolio management.

- Finally, DuPont analysis, as a tool, is a measure for an investment portfolio.

Instead of using this measure in isolation, using it along with other tools, such as return on investment, cash flow as a percentage of sales, or any other income statement item, will lead to fantastic analytical results.

Disadvantages

DuPont analysis suffers from several limitations. These are:

- It is a before-tax measurement of a short-term nature.

- It does not link to the cost of capital, time value of money, or the value itself.

- It is difficult to set a target for good ROCE.

- Using the gross value of assets as a measure instead of net value is contradictory to accounting practices based on principles and standards.

Calculating ROCE & Other Ratios Used in DuPont Analysis

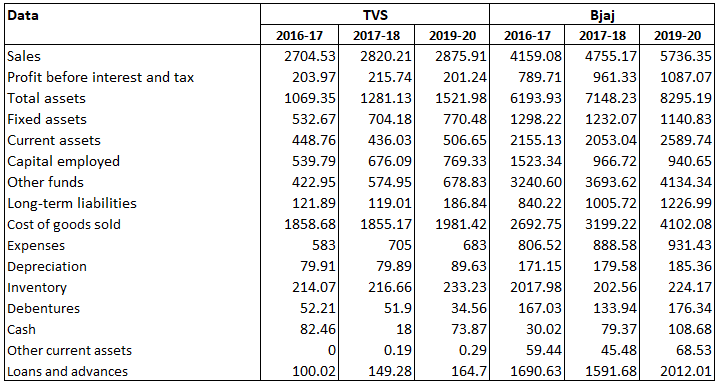

The table below shows data used to calculate all the ratios used in DuPont analysis. It shows a comparison of TVS and Bajaj over three years.

In terms of analysis, there are several points to note about the table above.

1. TVS has a lower ROCE mainly due to low operating profit (PBIT) and comparatively higher capital employed. This has been the trend for the past three years when TVS was trying to expand. Hence, it incurred greater costs.

As a result, TVS's non-trade investment is quite low compared to other competitors, particularly those that have been operating in the market for a long time.

2. PBIT/Sales is lower for TVS mainly due to a higher than average EXP/Sales for the industry.

3. Sales/TA of TVS is greater than the industry average mainly due to lower total assets, which in turn is due to lower current assets.

4. Sales/CA is also quite high for TVS compared to Bajaj, which is mainly due to lower amounts for Other CA and Loans and ADV (or in other words, huge Sales/Other CA and Sales/Loans and ADV).

5. As explained earlier, capital employed of TVS is low mainly because it has a low net worth and it has raised a lower amount of long-term loans when compared to Bajaj.

DuPont analysis, as a method of performance measurement, has gained importance and is being used to ascertain higher ROE.

Using the gross book value of assets instead of the net book value, the method can encourage investment in new, potentially risky ventures, namely, by estimating the return on investment appropriately.

One of the major advantages of DuPont analysis is that it decomposes return on net operating assets (RNOA) into two multiplicative components: profit margin and asset turnover. Both are largely driven by industry membership.

The components used in this analysis, being informative, facilitate data-adjusted industry comparisons, which helps to predict future changes in RNOA.

This analysis, if applied along with ratios suitable for investor analysis or market strength analysis, can help investors make good decisions for their investment portfolios.

Example of DuPont Analysis

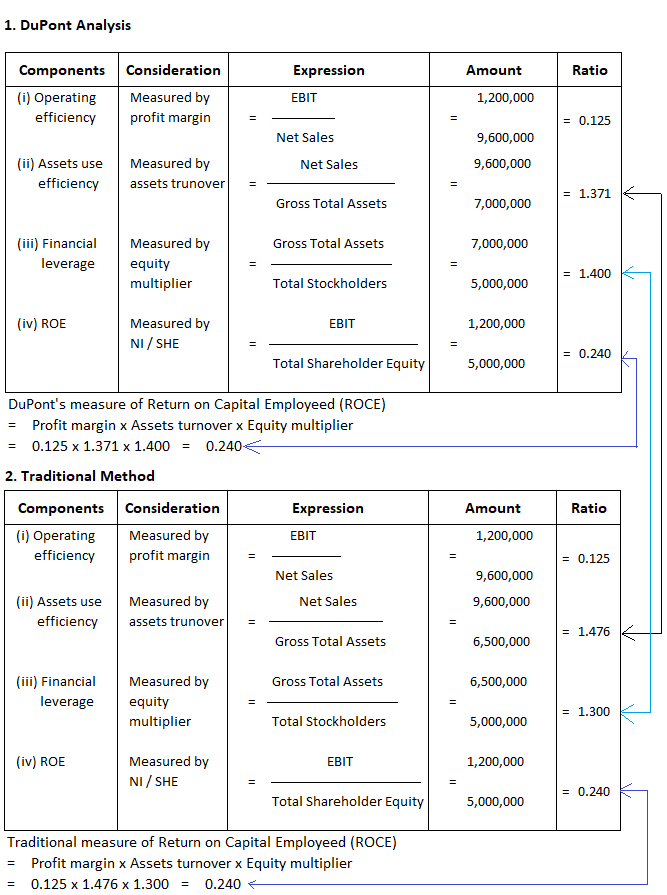

Here Company Ltd recorded the following information for the year 2019-20:

- Earnings before interest and tax (EBIT) $1,200,000

- Net sales $9,600,000

- Net assets $6,500,000

- Gross assets $7,000,000

- Equity share capital (shares of $10 each) 5,000,000

Required: Work out the following:

- Operating efficiency

- Asset use efficiency

- Financial leverage under:

- DuPont analysis

- Traditional analysis

- Compare the results and discuss from the viewpoint of a potential investor

Solution

(i) Under the traditional method, net assets turnover is considered.

(ii) The asset use efficiency under gross total assets is 1.371, whereas under net total assets it is 1.476. These results show that the use of the gross book value of assets removes the incentive to avoid investing in new assets.

(iii) ROE measured with EBIT divided by Total Stockholders Equity overlooks the role of operating activity, asset use, and financial leverage. However, DuPont analysis clearly shows the role of each component in ROE.

Modified DuPont Model

In modified DuPont analysis, an enterprise's operating decisions are analyzed using the operating profit margin (EBIT / Sales) and capital turnover (Sales / Invested Capital).

Financing decisions are checked with the financial cost ratio (EBIT / EBIT) and financial structure ratio (Invested Capital / Equity).

Even the incidence of business taxation is taken care of using the tax effect ratio (EAT / EBT).

The relationship that ties these five ratios together is that ROE is equal to their combined product.

In 1999, Hawawini and Viallet offered a modification to DuPont's model. This modification resulted in five different ratios that combine to form ROE.

They were of the opinion that the financial statements that enterprises prepare for their annual reports are not always useful for managers who need to make operating and financial decisions.

Therefore, Hawawini and Viallet restructured the traditional balance sheet into a managerial balance sheet, which is a more appropriate tool for assessing the contribution of operating decisions to the enterprise's financial performance.

This restructured balance sheet uses the concept of "invested capital" in place of total assets and the concept of "capital employed" in place of total liabilities and owner's equity found on the traditional balance sheet.

The primary difference is in the treatment of the short-term working capital account.

The managerial balance sheet uses a net figure called working capital requirement as a part of invested capital (this is determined receivables + inventories + prepaid expenses minus accounts payable + accrued expenses).

The modified DuPont model is constructed as follows:

In this model,

Invested capital = Cash + Working capital requirement + Net fixed assets

Noteworthily, the modified DuPont model still maintains the importance of the impact of operating decisions (i.e., profitability and efficiency) and financing decisions (leverage) upon ROE.

However, it uses a total of five ratios to uncover what drives ROE and gives insight as to how to improve this important ratio.

To improve ROE, it is necessary to increase operating profits, become more efficient in using existing assets to generate sales, use debt more effectively, control the cost of borrowing, and find ways to reduce the enterprise's tax liability.

Each of these choices leads to a different financial strategy. The five ratios combination model suggests better options for the decision-maker.

Key Points

- ROE is the most comprehensive measure of the profitability of the enterprise.

- It considers the operating and investing decisions made as well as financing and tax-related decisions.

- The model dissects ROE into five easily computed ratios that can be examined for potential strategies for improvement.

- It serves as an efficient tool for decision-makers (e.g., owners, managers, consultants, and others) when evaluating an enterprise and offering recommendations for improvement.

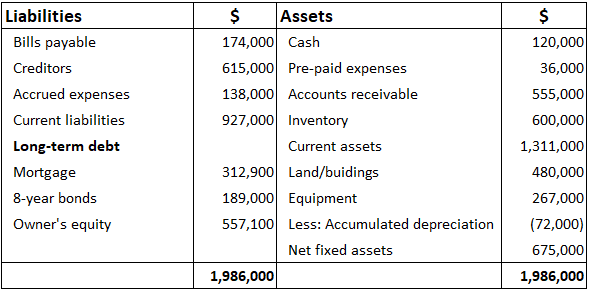

Exhibit

The exhibit below shows how the modified DuPont's model works.

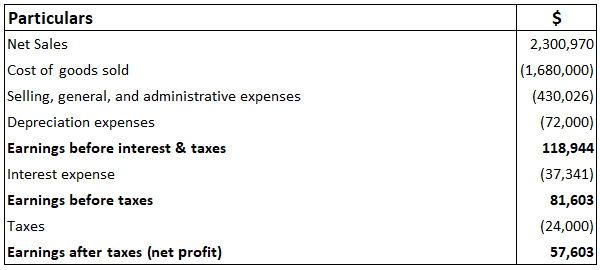

Income Statement

Balance Sheet

Calculation of ROE

1. Operating Profit Margin

= EBIT / Net sales = $118,944 / $2,300,970 = 0.571

2. Capital Turnover

= Net Sales / Invested capital = $2,300,970 / $1,233,000 = 1.866

3. Financial Cost Ratio

= Earnings before taxes / Earning before interest and taxes = $81,603 / $118,944 = 0.6861

4. Financial Structure

= Invested capital / Owner's equity = $1,233,000 / $557,100 = 2.2132

5. Tax Effect Ratio

= Earnings after tax / Earnings before tax = $57,603 / 81,603 = 0.7059

ROCE = 0.517 x 0.6861 x 2.1232 x 0.7059 = 0.1034 or 10.34%

Invested capital = Cash + Working capital + Net fixed assets

Working capital = [(PP expenses + Accounts receivable + Inventory) - (Creditors + Accrued expenses)]

Working capital = [($36,000 + $555,000 + $600,000) - ($615,000 + $138,000)]

Working capital = $1,191,000 - $753,000 = $438,000

Cash = $120,000 and Net fixed assets = $675,000

Therefore,

Invested capital = Cash ($120,000) + WC ($438,000) + Net fixed assets ($675,000) = $1,233,000)

Note: It is the same as conventional computation of ROCE.

= Earnings after tax / Owner's equity

= $57,603 / $557,100 = 10.34%

Original & Modified DuPont Analysis FAQs

The dupont identity reveals that roe is composed of three distinct components: operating profit margin, financial leverage and taxes.

The model is unable to identify which factors have a greater impact on roe. It cannot determine whether improving one component will lead to an improvement of roe.

Yes, it is useful in finding ways to control costs and increase sales volumes while maintaining solid financial structure.

This model delivers a clear message to decision-makers what drivers affect roe. With this information, they can make informed decisions that will lead to improved roe. The five-part formula is simple to use and understand which makes it more practical for them.

Yes, it works for all types of enterprises. It can uncover the major drivers and patterns of roe at different levels and stages of development. It helps decision-makers determine what factors need to be controlled and which ones need improvement.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.