Net method of recording purchase discounts is a method of recording purchase discounts in which the purchase and accounts payable are recorded at the net of the allowable discount. The net method of recording purchase discounts records the purchase and the accounts payable net of the allowable discount. If the payment is made within the discount period, Accounts Payable should be debited, and Cash should be credited for the amount at which the payable was originally recorded. If the firm does not pay within the discount period, the full invoice price is paid. The difference between the amount at which Accounts Payable is debited and Cash is credited is debited to an account titled Purchase Discounts Lost. $100 Purchase – Stated terms 2/10, n/30 This account is treated as either an operating expense or an interest expense. The argument for treating discounts lost as interest expense is based on the fact that the firm consciously chose not to pay within the allowable discount period, thus causing an additional cost. This additional cost represents a cost for the use of money and therefore is considered interest. As in the case of sales discounts, net method is preferable. Accounts payable are recorded at their expected cash payment at the time of purchase. Furthermore, the use of the account, Purchase Discounts Lost; highlights the total cost of not paying within the discount period. As we noted previously, this can be a significant cost, and it is generally in the firm’s best interest to pay within the discount period.What Is the Net Method of Recording Purchase Discounts?

Explanation

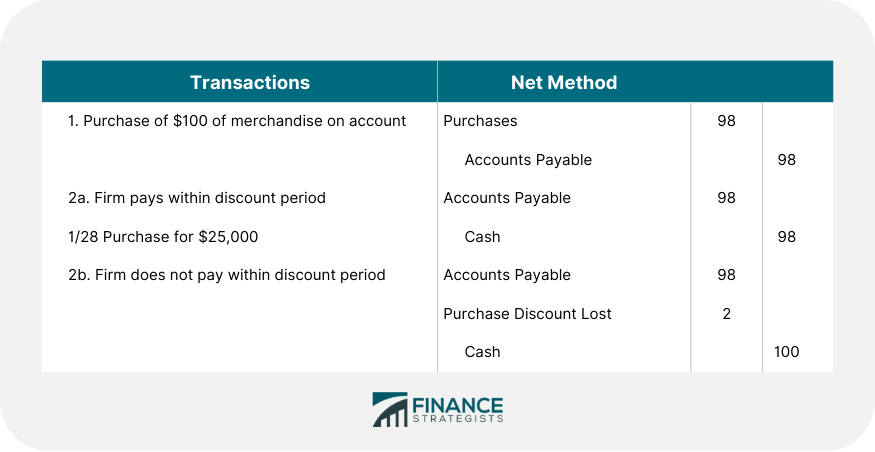

Journal Entries to Record Purchase Discounts Under Net Method

Net Method of Recording Purchase Discounts FAQs

Net Method of Recording Purchase Discounts is a method of accounting for discounts on purchases from suppliers in which the purchase discount taken by the company is recorded as an immediate offset to the cost of goods purchased, rather than being treated as a separate transaction or deferred until payment.

The net method works by recording any purchase discounts obtained from suppliers as an immediate offset to the cost of goods purchased. This means that the purchase amount will be reduced by the value of any discounts and only the net total (after taking into account discounts) will be recorded in accounts payable.

The net method should be used when discounts are taken on purchases from suppliers. This is because it records the effect of the discount at the time of purchase, rather than later when payment is made.

Using the net method has many benefits, including improved cash flow, as it immediately reduces accounts payable and increases cash available to the company; better budgeting, as there will be less money spent on goods without discounts; and increased efficiency in accounting processes as only one entry is required instead of two separate transactions for each purchase.

The main drawback to using the net method is that it does not record any information about the discounts taken or when they were taken. This means that if there is an audit, it will be difficult to prove that the discounts have been properly accounted for and recorded. Additionally, it may result in overstating profits by not recognizing any purchase discounts at the time of payment.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.