This article compares the effect of different cost flow assumptions—FIFO, average cost, and LIFO—on ending inventory, cost of goods sold, and gross margin for the Cerf Company.

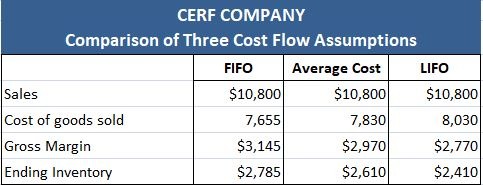

As shown in the table below, the highest gross margin and ending inventory, as well as the lowest cost of goods sold, resulted when FIFO was used.

The lowest gross margin and ending inventory and highest cost of goods sold resulted when LIFO was used.

The average cost fell between these two extremes for all three accounts. This is because the acquisition price of the inventory consistently rises during the year, from $4.10 to $4.70.

We deliberately constructed this example to reflect rising prices. This is because, in today's economy, rising prices are more common than falling prices.

However, in some sectors of the economy, such as electronics, prices have been falling.

In this case, the income statement and balance sheet effects of LIFO and FIFO would be the opposite of the rising-price situation.

That is, LIFO would produce the highest gross margin and the highest ending inventory cost.

Note: The figures in this table are taken from the example shown in the article entitled "Application of different cost flow assumptions."

Rising Prices and FIFO

In a period of rising prices, FIFO produces the highest gross margin and the highest ending inventory.

The high gross margin is produced because the earliest (and, therefore, the lowest) costs are allocated to the cost of goods sold.

Thus, cost of goods sold is the lowest of the three inventory costing methods, and gross margin is correspondingly the highest of the three methods.

Ending inventory reflects the highest cost under FIFO because the latest and highest costs are allocated to ending inventory.

These results are logical, given the relationship between ending inventories and gross margin.

On the one hand, many accountants approve of using FIFO because ending inventories are recorded at costs that approximate their current acquisition or replacement cost.

Thus, inventories are realistically valued on the firm's balance sheet.

On the other hand, other accountants criticize FIFO because it matches the earliest cost against sales and results in the highest gross margin.

Some accountants argue that these profits are overstated because, in order to stay in business, a going concern must replace its inventory at current acquisition prices or replacement costs.

These overstated profits are often referred to as inventory profits.

Example

To illustrate the concept of inventory profits, suppose that a firm enters into the following transactions:

- 2 January: Purchases one unit of inventory at $60

- 15 December: Purchases another unit of inventory at $85

- 31 December: Sells one unit at $100—current replacement cost of inventory at $85

On a FIFO basis, the firm reports a gross margin of $40 ($100 — $60). However, if it is to stay in business, the firm will not have $40 available to cover operating expenses.

This is because it must replace the inventory at a cost of at least $85.

Therefore, in reality, the firm has only $15 ($100 — $85) available to cover its operating expenses.

The $25 difference between the $85 replacement cost and the $60 historical cost is the inventory profit.

The inventory profit is considered a holding gain caused by the increase in the acquisition price of the inventory between the time that the firm purchased and then sold the item.

This holding gain is not available to cover operating costs because it must be used to repurchase inventory at new, higher prices.

Rising Prices and LIFO

In an economy where prices are rising, LIFO results in the lowest gross margin and the lowest ending inventory.

The low gross margin results when the latest and highest costs are allocated to cost of goods sold.

Thus, cost of goods sold is the highest of the three inventory costing methods, and gross margin is the lowest of the three methods.

Also, under LIFO, the ending inventory is recorded at the lowest cost of the three methods because the earliest and lowest prices are allocated to it.

In fact, if a company switched to LIFO 20 years ago, the original LIFO layers, if unsold, would be costed at 20-year-old prices.

In terms of its effects on the balance sheet and income statement, LIFO has the opposite effect of FIFO.

Consequently, LIFO is criticized because the inventory cost on the balance sheet is often unrealistically low.

Therefore, working capital, the current ratio, and current assets tend to be understated. The potential consequences may be drastic, as illustrated by the following excerpt from the 2019 Safeway annual report:

Consolidated working capital increased to $303 million in 2019 from $231 million and $218 million in 2018 and 2017, respectively. The current ratio increased to 1.19 from 1.15 and 1.16 in those years.

Had the company valued its inventories using FIFO, its current ratio would have been 1.40, 1.35, and 1.36, and working capital would have been $621 million, $520 million, and $508 million at the year-ends of 2019, 2018, and 2017, respectively.

Many accountants argue, however, that LIFO provides a more realistic income figure. The reason is that it eliminates a substantial portion of inventory profit.

If you refer back to the simple example on this page, you'll see that on a LIFO basis, the firm's gross margin is $15. This is because the 15 December 2019 purchase is matched against the $100 sale.

In this case, the acquisition price of the inventory did not change between the last purchase on 15 December and its sale on 31 December. Therefore, all the inventory profits are eliminated.

In reality, LIFO will not eliminate all inventory profits but will substantially reduce them. The elimination of these inventory profits on the income statement can be drastic.

For example, according to the Safeway annual report, the application of the LIFO inventory method reduced gross profits by $29.3 million in 2019. This is a substantial figure, considering that Safeway's net income for 2020 was $185.0 million.

In summary, in a situation of rising prices, FIFO and LIFO have opposite effects on the balance sheet and income statement.

LIFO usually provides a realistic income statement at the expense of the balance sheet. Conversely, FIFO provides a realistic balance sheet at the expense of the income statement.

In a period of falling prices, the opposite is true. In either case, the average cost will provide figures between those of FIFO and LIFO.

Comparison Between Different Cost Flow Assumptions FAQs

The term 'LIFO' stands for last-in, first-out. It means that the cost of the items which were most recently purchased is the cost that will be used for valuation purposes.

The term 'FIFO' stands for first-in, first-out. It means that the cost of the items which were most recently purchased is the cost that will be used for valuation purposes.

In a rising market, fifo is better for the balance sheet because it ensures that cogs will be higher than acb. In fact, fifo increases both cogs and ending inventory whereas the other two methods do not change ending inventory. In a falling market, lifo improves the balance sheet by increasing cogs and reducing ending inventory. This is because lifo increases both cogs and ending inventory whereas the other two methods do not change either of these figures.

Some companies prefer the conservatism of lifo, whereas others may feel that it is too conservative and opt for fifo. Others choose to use the average cost method, which provides a balance between fifo and lifo in terms of matching costs with sales revenue.

The average cost method calculates the total cogs for a certain period and then divides it by the number of units sold to provide an average unit cost. This figure is used as cogs in each reporting period. This provides figures between those of fifo and lifo, which may be viewed as less conservative than lifo but more conservative than fifo.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.