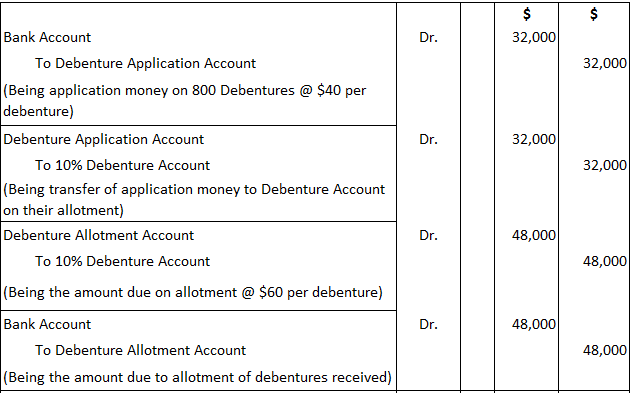

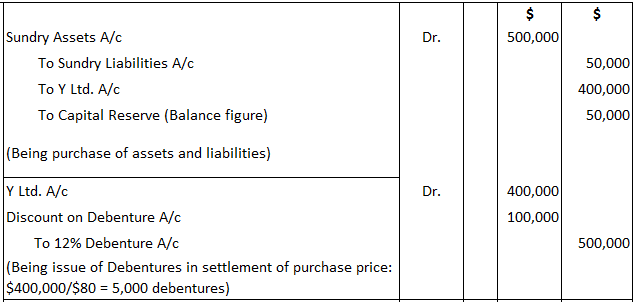

A company issued 1,000 10% debentures of $100 each at par, with $40 payable on application and the balance on allotment. The public applied for 800 debentures and the applications were accepted. All money was received. Required: Show the journal entries. X Ltd. acquired assets of $500,000 and took over the liabilities of Y Ltd., amounting to $50,000, at an agreed value of $400,000. It issued 12% debentures at a discount of 20% in full satisfaction of the purchase price. Required: Show the journal entries. John Ltd. secured an overdraft for $100,000 from the bank by depositing debentures worth $150,000 as collateral security. This will appear in the balance sheet as follows: A) No entry needs to be made in the books of accounts. However, a note is made in the balance sheet. B) Debentures that are issued to serve as collateral security can be recorded in the books of accounts. For instance, for the above example, the journal entry is: Balance Sheet A company issued $500,000 12% debentures at 94%. The terms of the issue include the repayment of the debentures in five equal installments, beginning with the end of the first year of issue. Required: Show the amount of discount that should be equitably written off for each of the five years. At the outset, it is worth noting that the discount comes to $4,000 (i.e., $100,000 x 0.4). Also, $800 is to be written off against the profit and loss account (i.e., equal annual installments). This is because each year has the benefit of the whole of the debentures. 10,000 7% redeemable preference shares of $10 each, fully paid, are outstanding on 1 January 2019 in a company. The company decides to redeem these shares on 1 March 2019 at $13 per share. To provide for redemption, the company issued 5,000 equity shares of $10 each at $14 each, payable in full on 20 February 2019. The profit and loss account shows a credit balance of $100,000. Required: Show the ledger account. 7% Redeemable Preference Share Capital Account Premium on Redemption Account 7% Redeemable Preference Shareholders Account Equity Share Capital Account Share Premium Account Capital Redemption Account Profit and Loss AccountIssue of Debentures Journal Entries

Practical Problem 1

Solution

Issue of Debentures for Non-cash Considerations

Practical Problem 2

Solution

Issue of Debentures as Collateral Security

Practical Problem 3

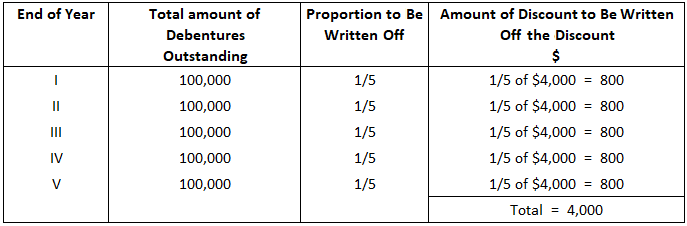

Discount on Debentures

Practical Problem 4

Solution

Redemption of Debentures

Practical Problem 5

Solution

Issue and Redemption of Debentures: Practical Problems and Solutions FAQs

Redemption of Debentures is the process by which the Debenture holders convert their investment into Equity Shares.

Redemption of Debentures is calculated by Debenture face value multiplied by a predetermined redemption rate. This calculation is based on formula fv = drr x d where fv= face value of Debenture drr= determined redemption rate d= number of days remaining till the redemption date from start day i.E. If the date of issue is 1-1-2017 and redemption date is 1-5-2020 then the number of days is 644 i.E., 365+(365/2)

The Debentures can be redeemed either by cash or by allotment of shares.

Redemption is important in Debentures because it ensures that companies do not keep on borrowing and roll over the debt. It also tells what the financial condition of a company is like (based on its ability to redeem loans) and, therefore, has an indirect relation with stock prices.

There are 2 types of redemption of Debentures; forced redemption and voluntary redemption.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.