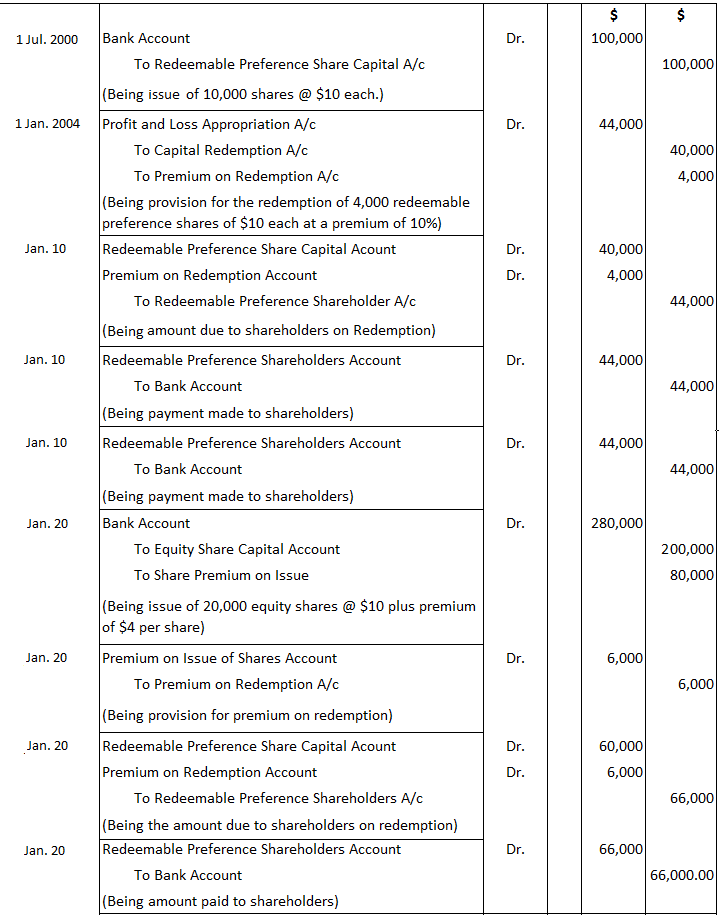

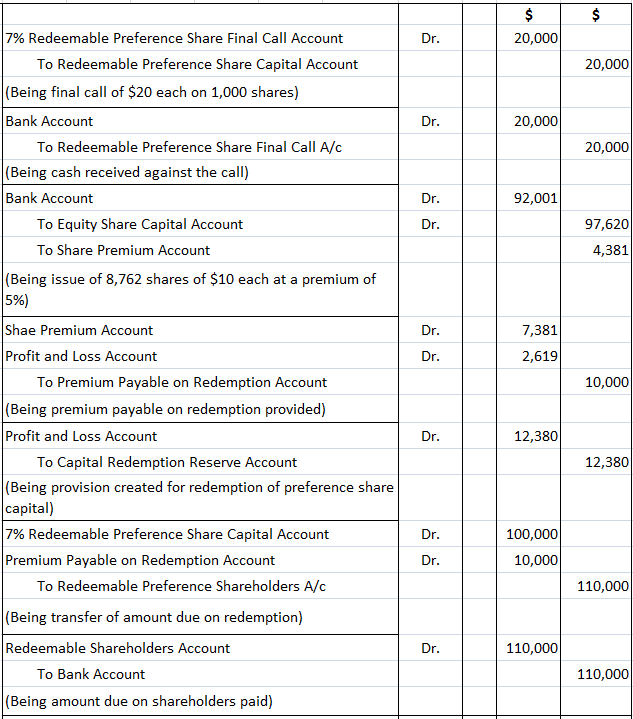

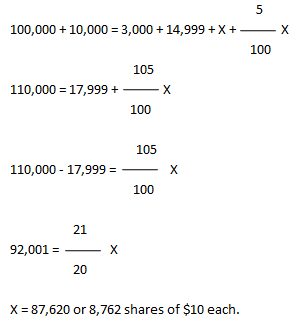

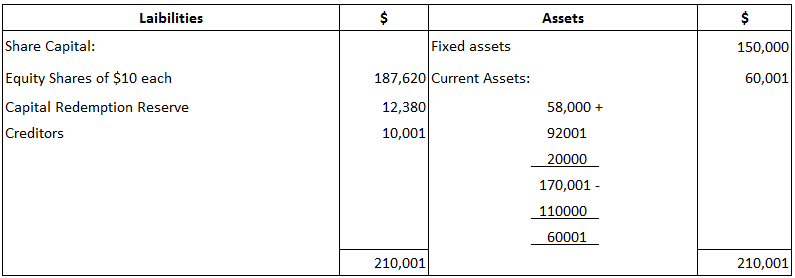

On 1 July 2000, a limited company issued 10,000 redeemable preference shares valued at $10 per share. The shares were redeemable at a premium of 10%. Two-fifths of the company's issue was redeemed out of profits on 10 January 2004. On 20 January 2004, the company issued 20,000 equity shares at $10 each at a premium of $4 per share. Out of the proceeds of the issue, the balance of redeemable preference shares was redeemed. Required: Make journal entries to record these transactions in the company's books. Journal Entries A company issued 50,000 equity shares at $10 per share and 3,000 redemption preference shares at $100 each. All shares were fully called and paid up. On 31 March 2004, the profit and loss account showed an undistributed profit of $50,000. The general reserve account stood at $120,000. On 2 April 2004, the directors decided to issue 1,500 6% preference shares at $100 per share for cash. They also redeemed the existing preference shares at $105, utilizing as much profits as required for the purpose. Required: On 31 March 2004, the cash balance amounted to $185,000 and Sundry Creditors stood at $87,000. Journal Entries The summarized balance sheet of a company is given as follows: The redeemable preference shares will be redeemed at a premium of 10%. The company's directors wish that only the minimum number of fresh equity shares of $10 each at a premium of 5% be issued to provide for the redemption of such preference shares, as could not otherwise be redeemed. Required: Give the journal entries and prepare the balance sheet after redemption. Journal Entries To calculate the minimum number of fresh shares to be issued, first let the dollar value of shares to be issued equal X. Alternatively, Balance SheetProblem 1: Redemption of Preference Shares at Premium

Solution

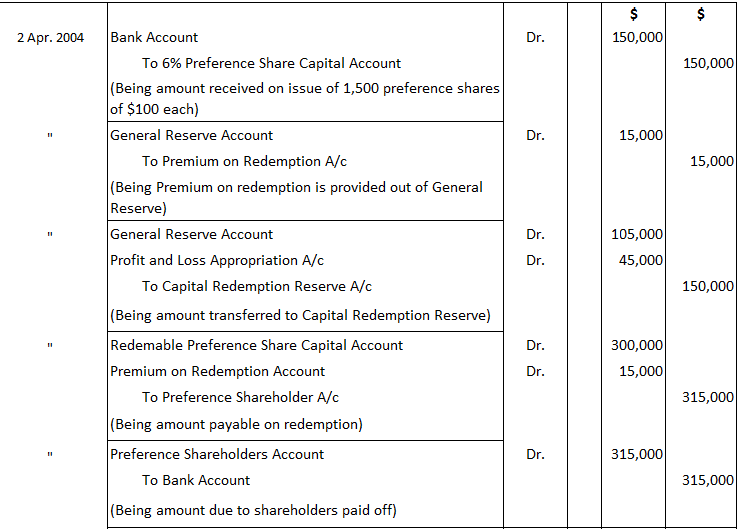

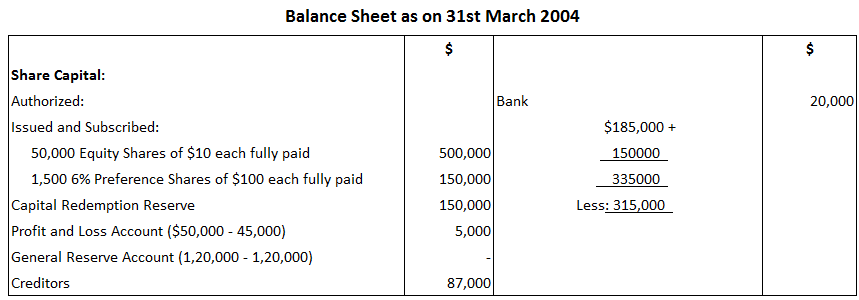

Problem 2: Redemption of Shares at Premium, Partly Out of Profits and Partly Out of Fresh Issue

Solution

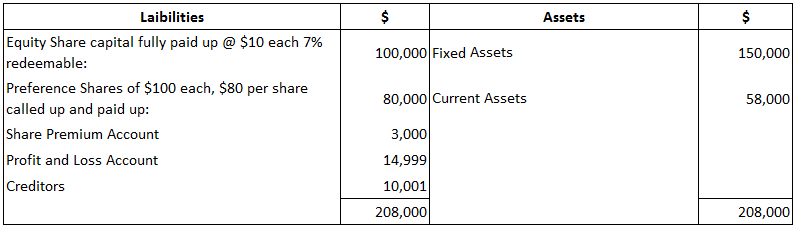

Problem 3: Where Minimum Number of Equity Shares Is to Be Issued for Redemptions

Solution

Redemption of Preference Shares: Practical Problems and Solutions FAQs

The redemption of preference shares is the process by which a company repurchases its own preferred stock from shareholders.

They are hybrid securities, which generally combine debt and equity. Depending on their terms, the australian taxation office (ATO) may classify them as a debt interest rather than an equity interest. This may have tax implications for shareholders.

Price of preference = (total number of redeemable preferred shares / number of preference shares issued) x 100

The cash account should be debited to record redemption of preference shares. If the preference shares are redeemed for $10 per share, a debit entry will be made to the cash account. Likewise, if preference shares are redeemed for Rs 10 per share, a credit entry will be made to the cash account.

Upon redemption, the redeemable preference shares are canceled. You should remember that a company’s redemption of the shares eliminates any dividend rights attached to them. An exception to this is where the terms of issue specify otherwise.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.