A high-yield savings account is a deposit account designed to help individuals grow their savings by offering a higher interest rate compared to traditional savings accounts. These accounts are ideal for people looking to save for short-term or long-term financial goals, such as an emergency fund, a down payment on a house, or a major purchase. High-yield savings accounts differ from traditional savings accounts mainly in the interest rate they offer. While traditional savings accounts typically offer relatively low interest rates, high-yield accounts provide a higher return on the account holder's savings, making them a more attractive option for savers looking to grow their money more quickly. High-yield savings accounts offer several benefits, including competitive interest rates, increased savings growth, and easy access to funds. These accounts can help individuals reach their financial goals faster while still providing the safety and security of a federally insured deposit account. Interest on high-yield savings accounts is typically calculated daily and compounded monthly, which means that interest is added to the account balance regularly and continues to earn interest over time. This compound interest can significantly boost the growth of savings over time. Interest rates on high-yield savings accounts are influenced by several factors, including the federal funds rate set by the Federal Reserve, economic conditions, and competition among banks and credit unions. Banks with more funds to lend may offer higher interest rates to attract more deposits. High-yield savings accounts are often found at online banks rather than traditional brick-and-mortar institutions. Online banks have lower operating costs, allowing them to offer higher interest rates on their savings products. However, some traditional banks and credit unions also offer competitive high-yield savings accounts. Credit unions are member-owned financial institutions that often provide competitive interest rates on high-yield savings accounts. As not-for-profit organizations, credit unions can pass on savings to their members in the form of higher interest rates and lower fees. Many high-yield savings accounts provide ATM access, allowing account holders to withdraw funds easily. However, some banks may charge fees for using out-of-network ATMs, so it's essential to understand the bank's ATM policy when choosing a high-yield savings account. High-yield savings accounts generally offer mobile and online banking features, making it easy for account holders to manage their accounts, check balances, and transfer funds. This increased accessibility is especially helpful for those using online banks, which may not have physical branches. Some high-yield savings accounts charge monthly maintenance fees, which can reduce the account's overall interest earnings. However, many banks waive these fees if account holders maintain a minimum balance or meet other requirements. Federal Regulation D limits the number of monthly withdrawals or transfers from a savings account to six. Exceeding this limit may result in fees or account closure. Additionally, some banks may charge fees for excessive withdrawals or transfers, so it's essential to be aware of these limitations when choosing a high-yield savings account. Many high-yield savings accounts have minimum balance requirements, which means account holders must maintain a certain balance to earn the advertised interest rate or avoid fees. Understanding these requirements and choosing an account that aligns with your financial situation and savings goals is essential. • Interest Rates - When looking for a high-yield savings account, compare interest rates among different banks and credit unions. Higher interest rates can lead to greater savings growth over time. • Bank Reputation and Customer Service - Consider the reputation and customer service of the financial institution offering the high-yield savings account. Reading customer reviews and researching the bank's history can help you find a trustworthy institution with a strong track record. • Account Features and Requirements - Review the account features and requirements, such as minimum balance requirements, fees, and accessibility options, to find a high-yield savings account that best suits your needs. Required Documentation - When opening a high-yield savings account, you will need to provide personal information and documentation, such as your Social Security number, government-issued ID, and proof of address. Account Funding - You will also need to fund the account by depositing an initial amount, which may vary depending on the bank's requirements. This can usually be done through a transfer from an existing bank account, a check, or a wire transfer. Approval and Account Setup - Once your application is approved, you will receive account details, such as your account number and routing number. You can then set up online and mobile banking access to manage your new high-yield savings account. Regularly Reviewing Interest Earned - Monitoring the interest earned on your high-yield savings account is essential. This will help you track your savings growth and ensure that you are receiving the advertised interest rate. Comparing Interest Rates With Other Institutions - Periodically compare the interest rate on your high-yield savings account with those offered by other banks and credit unions. If you find a higher rate elsewhere, consider switching accounts to maximize your savings growth. Automatic Transfers - Set up automatic transfers from your checking account to your high-yield savings account to ensure consistent savings growth. This can be done monthly or bi-weekly, depending on your financial situation and goals. Direct Deposit - Consider setting up a direct deposit from your employer to your high-yield savings account. This can help you save a portion of your paycheck automatically, making it easier to achieve your savings goals. Wire Transfers - Wire transfers can be used to deposit or withdraw funds from your high-yield savings account. However, keep in mind that wire transfers may come with fees, so it's essential to understand the costs associated with this method. • Setting up Automatic Savings Plans - Establish automatic savings plans to help you reach your financial goals more quickly. This can involve setting up regular transfers, direct deposits, or using budgeting tools and apps to help you save more effectively. • Utilizing Budgeting Tools and Apps - Many budgeting tools and apps can help you track your spending, set savings goals, and monitor your high-yield savings account's performance. These tools can be useful in managing your personal finances and maximizing your savings growth. • Inflation - Inflation can erode the value of your savings over time. If the interest rate on your high-yield savings account is lower than the rate of inflation, your savings may lose purchasing power. • Interest Rate Fluctuations - Interest rates on high-yield savings accounts can fluctuate due to changes in the federal funds rate or market conditions. It's important to monitor interest rates regularly and adjust your savings strategy accordingly to ensure your savings continue to grow. Federal Regulation D - Federal Regulation D limits the number of withdrawals or transfers from a savings account to six per month. This can be a disadvantage for individuals who require more frequent access to their funds. Penalty Fees - Exceeding the withdrawal or transfer limits set by Federal Regulation D can result in penalty fees or account closure. It's essential to be aware of these limitations and manage your high-yield savings account accordingly. • Bank Mergers and Acquisitions - Bank mergers and acquisitions can lead to changes in account terms, fees, or interest rates. It's important to stay informed about any changes to your high-yield savings account and adjust your savings strategy as needed. • Changes in Account Terms - Banks may change the terms of high-yield savings accounts, such as interest rates or fees, at any time. Regularly review your account's terms and conditions to ensure you are still receiving the best possible rate and account features. Certificates of Deposit (CDs) are time-based deposit accounts that generally offer higher interest rates than high-yield savings accounts. However, CDs have fixed terms and may charge penalties for early withdrawals, making them less flexible than high-yield savings accounts. Money market accounts are similar to high-yield savings accounts, offering higher interest rates and limited check-writing capabilities. However, they may come with higher minimum balance requirements and fees compared to high-yield savings accounts. Investment accounts, such as stocks, bonds, or mutual funds, can offer higher returns than high-yield savings accounts but come with greater risks. It's essential to consider your risk tolerance and investment goals carefully before choosing this option. Retirement accounts, such as Individual Retirement Accounts (IRAs) or 401(k) plans, offer tax advantages and potential long-term growth for retirement savings. While these accounts may have restrictions on withdrawals and contribution limits, they can be an excellent complement to a high-yield savings account for long-term financial planning. High-yield savings accounts offer a higher interest rate than traditional ones, making them an attractive option for savers looking to grow their money more quickly. They provide competitive interest rates, increased savings growth, and easy access to funds, making them ideal for short-term or long-term financial goals. When choosing a high-yield savings account, it's essential to consider factors such as interest rates, account types, accessibility, fees, and minimum balance requirements. It's also important to monitor account performance, manage deposits and withdrawals, and understand the risks and limitations. While there are alternatives to high-yield savings accounts, such as CDs, money market accounts, investment accounts, and retirement accounts, high-yield savings accounts remain a popular and effective savings tool. So, if you're looking to grow your savings, consider opening a high-yield savings account in a bank today.What Are High-Yield Savings Accounts?

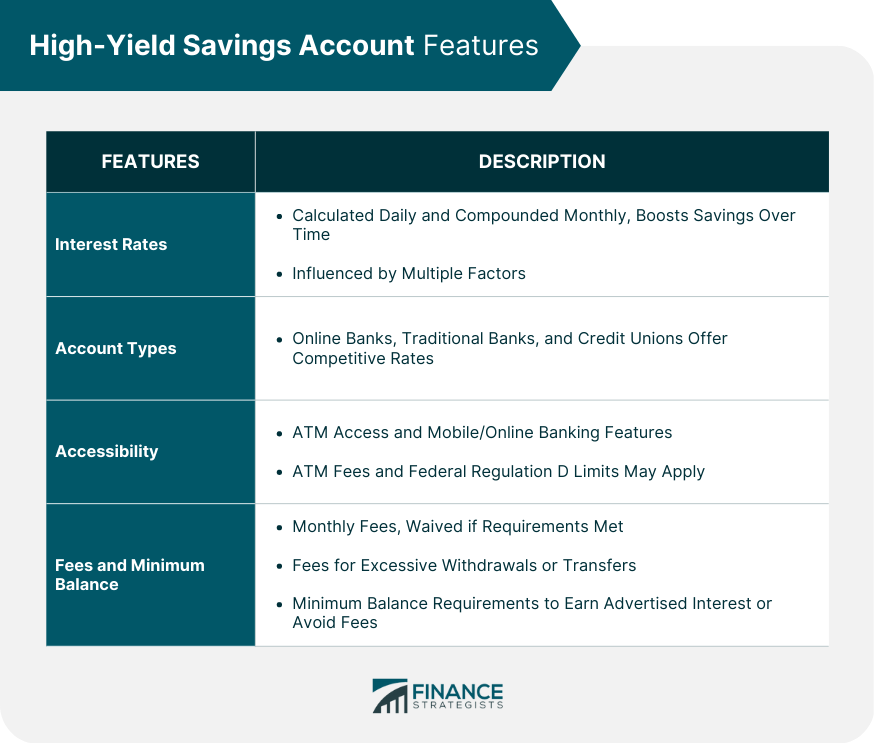

Features of High-Yield Savings Accounts

Interest Rates

Account Types

Accessibility

Fees and Minimum Balance Requirements

Opening a High-Yield Savings Account

Researching and Comparing Options

Application Process

Managing Your High-Yield Savings Account

Monitoring Account Performance

Making Deposits and Withdrawals

Maximizing Savings

Risks and Limitations of High-Yield Savings Accounts

Economic Factors

Withdrawal Limitations

Account Closure or Changes by the Bank

Alternatives to High-Yield Savings Accounts

Certificates of Deposit (CDs)

Money Market Accounts

Investment Accounts

Retirement Accounts

Final Thoughts

High-Yield Savings Accounts FAQs

A high-yield savings account is a deposit account designed to help individuals grow their savings by offering a higher interest rate compared to traditional savings accounts.

High-yield savings accounts differ from traditional savings accounts mainly in the interest rate they offer. Interest on high-yield savings accounts is typically calculated daily and compounded monthly, which means that interest is added to the account balance regularly and continues to earn interest over time.

High-yield savings accounts offer several benefits, including competitive interest rates, increased savings growth, and easy access to funds. These accounts can help individuals reach their financial goals faster while still providing the safety and security of a federally insured deposit account.

When choosing a high-yield savings account, it's essential to consider factors such as interest rates, account types, accessibility, fees, and minimum balance requirements. It's also important to review the bank's reputation and customer service to find a trustworthy institution with a strong track record.

Economic factors such as inflation and interest rate fluctuations can affect the value of savings over time. Additionally, Federal Regulation D limits the number of withdrawals or transfers from a savings account to six per month, and exceeding this limit may result in penalty fees or account closure. It's essential to be aware of these limitations and manage your high-yield savings account accordingly.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.