Yes, you can open a bank account with bad credit. While bad credit may present challenges and potentially limit the types of accounts available to you, there are specific account options designed for individuals with less-than-perfect credit histories. Basic bank accounts, second-chance bank accounts, and prepaid debit cards are examples of such options. To improve your chances of opening a bank account with bad credit, consider researching banks and credit unions that offer specialized account options for individuals with poor credit. Address any outstanding issues contributing to your bad credit before applying for an account. Providing proof of financial stability, such as steady income or employment, may also bolster your application. Remember, while bad credit may present obstacles, taking proactive steps to improve your creditworthiness and exploring alternative banking options can help you gain access to essential financial services and work towards a more stable financial future. Your credit history significantly influences the process of opening a bank account. Financial institutions consider your creditworthiness based on your credit history and credit score. A positive credit history and a high credit score indicate responsible financial behavior, making it more likely for banks to approve your account application. Conversely, bad credit or a low credit score may lead to a denial of your account application, as banks may perceive individuals with poor credit as higher-risk customers. Moreover, your credit may impact the types of account options available to you, with better credit often granting access to a broader range of accounts with various benefits and features. Banks may conduct credit checks and review your ChexSystems report, which can affect your account application. If you have bad credit, exploring banks that offer second chance bank accounts or seeking a co-signer with good credit can improve your chances of opening an account. Over time, working to improve your credit can lead to better opportunities for financial services and products in the future. Opening a bank account with bad credit may require a bit more effort and consideration, but it is certainly possible. The following are the steps to increase your chances of successfully opening a bank account: Look for financial institutions that offer account options specifically designed for individuals with bad credit. Basic bank accounts are accessible to individuals with bad credit or no credit history, offering minimal requirements and fees. Second chance bank accounts provide an opportunity for those who have faced financial difficulties in the past to rebuild trust with financial institutions and access essential banking services. Prepaid debit cards are not linked to a bank account and require preloaded funds, making them a viable alternative for budgeting and online transactions. Before applying for a bank account, review your credit report for any inaccuracies and address outstanding debts. Paying off any overdue balances and resolving issues on your credit report can improve your chances of approval. Opt for a basic bank account or a second chance bank account, as they are more likely to be accessible to individuals with bad credit. These accounts may have fewer requirements and lower fees, making them a better fit for your situation. Prepare the necessary identification and verification documents required by the bank or credit union. Common documents include a government-issued ID, proof of address, and Social Security number. If possible, consider asking someone with good credit to co-sign on your account. A co-signer takes responsibility for the account in case of any issues, providing added security for the bank and potentially increasing your chances of approval. While some banks offer online account opening, visiting a branch in person can allow you to explain your situation to a bank representative. This personal touch may positively impact their decision-making process. Be honest about your credit history and financial situation when applying for the account. Transparency can build trust with the bank and show your commitment to improving your financial standing. As you maintain the account responsibly, work on improving your credit by paying bills on time, reducing debt, and managing your finances wisely. Over time, this can lead to better credit opportunities and financial stability. Several factors influence an individual's ability to open a bank account. These factors are taken into consideration by financial institutions to assess the applicant's eligibility and creditworthiness. The key factors include: • Credit Score and History: A higher credit score indicates better creditworthiness, making it easier to open a bank account. On the other hand, a low credit score or a history of defaults can raise concerns for banks and may result in a denied application. • ChexSystems Report: Banks often check the applicant's ChexSystems report, which contains information about their banking history. Negative entries, such as bounced checks, overdrafts, or account closures, may lead to account denials or limited account options. • Identity Verification: Financial institutions require valid identification to verify the applicant's identity. Lack of proper identification can be a barrier to opening an account. • Residency Status: Some banks may have specific requirements regarding residency status. Non-residents or individuals without a permanent address may encounter difficulties in opening an account. • Financial Stability: Banks may consider the applicant's financial stability and income to assess their ability to maintain the account and avoid potential overdrafts. Here are some useful tips to help you manage your bank account: Regularly Monitor Your Account: Keep a close eye on your account balance and transaction history. Regularly review your statements, online banking, or mobile app to identify any unauthorized transactions or errors. Set-up Account Alerts: Many banks offer account alert services via email or text messages. Set up alerts for low balances, large transactions, or account activity to stay informed about your account's status. Create a Budget: Establish a budget to track your income and expenses. Categorize your spending to understand where your money goes and identify areas where you can save or cut back. Automate Bill Payments: Set up automatic bill payments for recurring expenses like rent, utilities, and loan payments. This helps avoid late fees and ensures your bills are paid on time. Avoid Overdrafts: Keep track of your account balance to avoid overdrawing your account. Overdraft fees can quickly add up and strain your finances. Check for Account Fees: Review your bank's fee schedule and be aware of any charges associated with your account. Look for ways to minimize fees, such as meeting account requirements to waive monthly service charges. Reconcile Your Account: Regularly reconcile your account to ensure that your records match the bank's records. This involves comparing your transactions and balances to your bank statement. Review Account Benefits: Familiarize yourself with any additional benefits or perks offered by your bank. Some accounts may provide discounts, cashback rewards, or other incentives that can save you money. Be Wary of Overdraft Protection: While overdraft protection can prevent declined transactions, it may come with fees. Consider opting out if you prefer to manage your account balance carefully. Opening a bank account with bad credit is indeed possible through specialized account options like basic bank accounts, second-chance bank accounts, and prepaid debit cards. To improve your chances of approval, research banks and credit unions offering such accounts and address any outstanding credit issues. Consider a co-signer or prepaid debit card if necessary. Additionally, building a positive credit history over time can lead to better opportunities for financial services. Your credit significantly influences the account opening process, affecting account approval, denial, and the types of account options available. Being aware of your credit situation, regularly monitoring your account, setting up alerts, and adhering to a budget are essential for managing your bank account effectively. By following the tips and demonstrating responsible financial behavior, you can enhance your creditworthiness and work towards financial stability.Can You Open a Bank Account With Bad Credit?

How Does Your Credit Affect Opening a Bank Account?

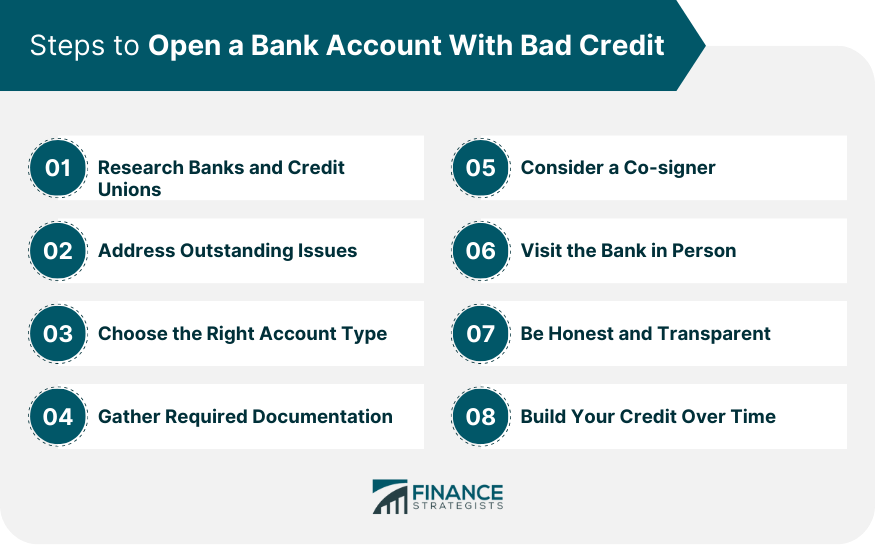

How to Open a Bank Account With Bad Credit

Research Banks and Credit Unions

Address Outstanding Issues

Choose the Right Account Type

Gather Required Documentation

Consider a Co-signer

Visit the Bank in Person

Be Honest and Transparent

Build Your Credit Over Time

Factors That Influence Your Ability to Open a Bank Account

Tips for Managing Your Bank Account

Conclusion

Opening a Bank Account With Bad Credit FAQs

Yes, you can open a bank account with bad credit. While it may present challenges, there are specialized account options designed for individuals with poor credit histories.

Individuals with bad credit can consider basic bank accounts, second-chance bank accounts, or prepaid debit cards as suitable options to open a bank account.

Yes, bad credit can impact the approval process for opening a bank account. Banks may consider your creditworthiness and may be more cautious in offering certain account options.

To enhance your chances, research banks offering specialized accounts for bad credit. Address any outstanding credit issues and consider a co-signer or prepaid debit card if necessary.

Yes, improving your credit over time may make you eligible for more traditional bank accounts with additional benefits and features once you demonstrate better creditworthiness.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.