Overdraft protection is a service offered by many financial institutions to shield account holders from unintentional overdrafts in their checking accounts. This service, when activated, prevents individuals from experiencing declined transactions or bouncing checks because of insufficient funds. Historically, if an individual wrote a check or made a payment that exceeded their account balance, the transaction would either be declined or the account would go into the negative, incurring hefty fees. Overdraft protection emerged as a solution, providing a buffer for such transactions. In today’s digital banking era, overdraft protection not only covers traditional check payments but also extends to debit card transactions, online payments, and automated bill payments. The primary purpose of overdraft protection is to prevent accounts from being overdrawn. This means ensuring that account holders do not go into a negative balance, which can lead to additional financial complications. Overdraft fees can be substantial, often ranging from $10 to $45 per occurrence. Overdraft protection can prevent these fees from accruing, saving account holders a significant amount of money. Having a transaction declined, especially in essential situations such as paying bills or making necessary purchases, can be distressing. Overdraft protection ensures continuity in transactions, ensuring they go through even when funds are low. One of the most common ways overdraft protection works is by linking a checking account to a savings account. If the checking account runs low, funds from the savings account are automatically transferred to cover the deficit. Some institutions allow overdrafts to be covered by linking to a credit card. If an account is overdrawn, a cash advance is taken from the card to offset the shortfall. In some cases, individuals might have multiple checking accounts. They can set one account as a backup to cover overdrafts in the primary account. An overdraft line of credit is a special type of loan that banks offer to account holders. Unlike traditional loans with fixed terms, these lines of credit are only used when an account is overdrawn. They act as a temporary loan to cover the deficit. While overdraft lines of credit can be helpful, they come with their own set of costs. The borrowed amount accumulates interest, and there might be annual fees or transaction fees associated with the service. Some banks automatically enroll customers in an overdraft coverage service. This means that, by default, the bank will cover transactions that exceed the account balance. Not all transaction types may be covered. While some banks might cover checks and recurring debits, others might not cover ATM or everyday debit card transactions unless you opt in. Due to regulations, many banks require customers to explicitly opt-in for overdraft coverage for everyday debit card transactions. Customers also have the option to opt out if they do not want the service. No one likes the embarrassment or inconvenience of a declined transaction. Overdraft protection offers the reassurance that transactions will be honored, even if funds are momentarily low. Automatic bill payments, like utility or rent, are crucial. Overdraft protection ensures these payments go through, avoiding late fees or service interruptions. Many banks offer automated alerts when an account balance drops below a certain threshold. This, combined with overdraft protection, helps manage finances more efficiently. As previously highlighted, the potential savings from avoiding multiple overdraft fees can be substantial over time. In the event of unexpected expenses, overdraft protection can act as a temporary buffer, allowing individuals to navigate financial emergencies without declined transactions. Everyone goes through financial highs and lows. During challenging times, overdraft protection offers a brief reprieve, ensuring daily transactions aren’t disrupted. While overdraft lines of credit provide a buffer, the associated interest can accumulate, leading to higher costs in the long run. Some banks charge a fee each time an automatic transfer occurs due to an overdraft. Over time, these fees can add up. With overdraft protection in place, some individuals might not feel the urgency to regularly monitor their account balances, potentially leading to financial negligence. Knowing there's a safety net can sometimes lead to complacency or even increased spending, even when funds are low. It’s important to understand which transactions are covered under an overdraft protection plan and which are not to avoid unexpected declines or fees. Banks might have a cap on the number of consecutive or monthly overdrafts they'll cover, after which they may decline transactions or charge higher fees. If an overdraft line of credit is repeatedly accessed and not repaid promptly, it might negatively impact one’s credit score. Unsettled overdrafts can be sent to collections, further damaging one’s credit profile. Monitor and Regularly Review Account Activity: Active oversight of your financial accounts is essential. Regularly checking ensures you are aware of your financial standing and can make informed decisions. Set Alerts for Low Balances: Set up automated alerts for when your balance drops to a certain point. This can act as a reminder to either transfer funds or curb spending. Understand Terms and Costs: Always read the fine print. Understand the costs associated with your overdraft protection service, be it interest, transfer fees, or annual charges. Consider Alternatives Like Alerts Without Overdraft: If you're unsure about overdraft protection, consider alternatives. Some banks offer low balance alerts without the overdraft service, ensuring you’re informed without the added service. Overdraft protection serves as a crucial buffer for many, ensuring transaction continuity during financial shortfalls. This tool, prevalent in today's digital banking era, safeguards against hefty overdraft fees and the discomfort of declined transactions. By offering multiple methods of coverage, from linking to savings accounts to credit lines, it presents varied options tailored to individual needs. However, it's not without its challenges. The potential fees, the risk of promoting negligent financial behaviors, and their implications on credit health are factors one must consider. The essence of this service lies in its dual nature: it can be a financial lifesaver for some while posing risks for others. It underscores the importance of active account management, awareness of terms, and periodic reviews to harness its benefits while mitigating drawbacks.What Is Overdraft Protection?

Purpose and Importance of Overdraft Protection

Prevention of Overdrawn Accounts

Avoidance of Overdraft Fees

Protection Against Declined Transactions

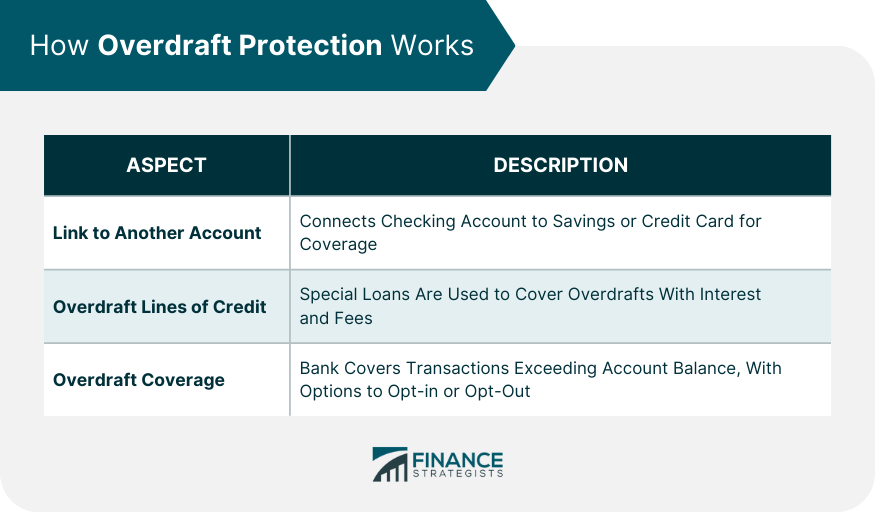

How Overdraft Protection Works

Link to Another Account

Savings Accounts

Credit Cards

Secondary Checking Accounts

Overdraft Lines of Credit

How They Differ From Traditional Loans

Interest and Fees

Overdraft Coverage

Automatic Coverage by the Bank

Transaction Types Covered

Opt-in and Opt-out Options

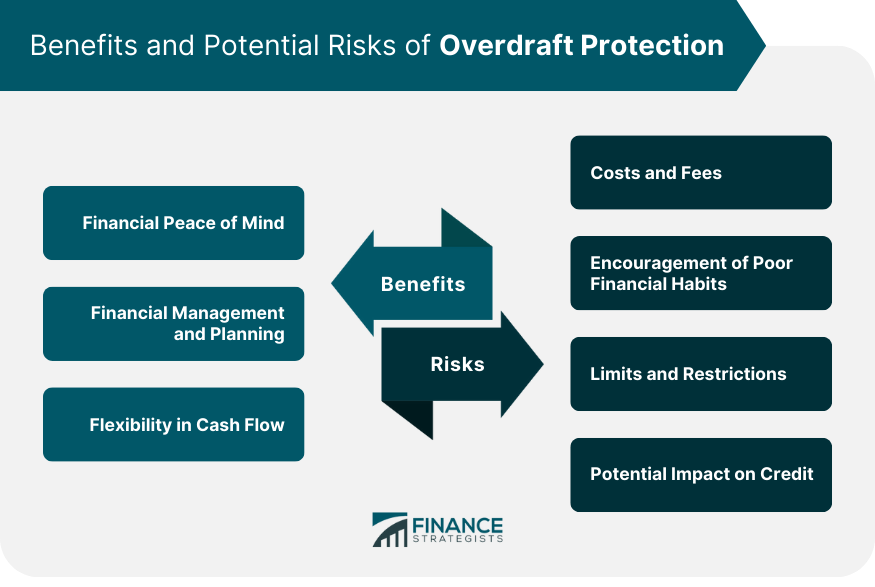

Benefits of Overdraft Protection

Financial Peace of Mind

Financial Management and Planning

Flexibility in Cash Flow

Potential Risks of Overdraft Protection

Costs and Fees

Encouragement of Poor Financial Habits

Limits and Restrictions

Potential Impact on Credit

Tips for Managing Overdraft Protection

Final Thoughts

Overdraft Protection FAQs

Overdraft protection is a banking service that prevents account holders from unintentionally overdrawing their checking accounts, shielding them from declined transactions or bouncing checks due to insufficient funds.

When a checking account is linked to a savings account, funds from the savings account are automatically transferred to the checking account if it runs low or goes negative, ensuring transactions are not declined.

Yes, while overdraft protection can save users from overdraft fees, there might be other costs involved, such as interest on overdraft lines of credit, transfer fees, or annual service charges, depending on the bank and the specific protection plan.

Regular overdraft protection (like linking to a savings account) typically doesn't affect your credit score. However, if you're using an overdraft line of credit and fail to repay it promptly, or it goes to collections, it could negatively impact your credit score.

Absolutely. Many banks require customers to opt-in for certain types of overdraft protection, especially for everyday debit card transactions. If you're enrolled and wish to opt out, you can usually do so through your bank's customer service or online portal.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.