A canceled check is a check that has been processed and cleared by the bank, indicating that the funds have been transferred from the account of the person who wrote the check to the payee's account. Once a check has been canceled, it is marked as such by the bank and can no longer be used to withdraw funds. Canceled checks serve as proof of payment and are essential in banking transactions, as they provide a record of completed transactions and can be used to verify payments and resolve disputes. Canceled checks play a crucial role in banking and financial transactions. They serve as a record of payment, providing evidence that funds have been transferred from one party to another. This documentation is useful for various purposes, including tax reporting, account reconciliation, and dispute resolution. Additionally, canceled checks can help individuals and businesses track their expenses and maintain accurate financial records, which is essential for effective financial planning and management. The process of canceling a check begins when the payee, or the person receiving the check, presents it to their bank for deposit or cashing. The bank then sends the check to the check writer's bank, initiating the process of verifying the check and transferring the funds. Upon receiving the check, the check writer's bank verifies the account holder's information and confirms that there are sufficient funds in the account to cover the check amount. If everything is in order, the bank clears the check, transferring the funds to the payee's account. Once the funds have been transferred, the check is marked as canceled by the check writer's bank. This marking indicates that the check has been processed and can no longer be used to withdraw funds. The canceled check may be stamped or marked electronically, depending on the bank's practices. After the check has been marked as canceled, it is typically returned to the check writer as part of their monthly bank statement or as an electronic image through online banking services. This provides the check writer with a record of the completed transaction and serves as proof of payment. One reason a check may be canceled is due to insufficient funds in the check writer's account. If there are not enough funds to cover the check amount, the bank may return the check to the payee marked as "canceled" or "insufficient funds." In this case, the check writer may be subject to fees and penalties from both their bank and the payee's bank. A check may also be canceled if the account holder requests a stop payment on the check. A stop payment request can be made for various reasons, such as if the check has been lost or stolen, or if the account holder has a dispute with the payee. In this case, the bank will not process the check, and it will be returned to the payee marked as "canceled" or "stop payment." A check may be canceled if the bank suspects fraudulent activity, such as if the check has been altered or forged. In these cases, the bank may refuse to process the check and return it to the payee marked as "canceled" or "fraud." If a check contains an error, such as an incorrect date, amount, or payee name, the bank may cancel the check and return it to the payee. In this case, the check writer would need to correct the error and reissue the check to the payee. Banks have a responsibility to maintain accurate records of canceled checks, including images or physical copies of the checks, as well as details about the transactions, such as the date, amount, and payee information. These records are essential for resolving disputes, verifying transactions, and ensuring the accuracy of account statements. Account holders should also maintain records of their canceled checks, either by retaining physical copies or accessing electronic images through their bank's online services. Keeping track of canceled checks can help account holders monitor their expenses, reconcile their accounts, and verify transactions for tax and financial reporting purposes. The retention period for canceled checks varies depending on the bank's policies and any legal or regulatory requirements. Generally, banks are required to retain records of canceled checks for a minimum of seven years, although some may choose to keep them for a longer period. Account holders should consult their bank's policies to determine the appropriate retention period for their canceled checks. Account holders have certain rights and obligations when it comes to canceled checks. They are responsible for ensuring the accuracy of the checks they write and for ensuring that there are sufficient funds in their accounts to cover the check amounts. If a check is canceled due to insufficient funds or a stop payment request, the account holder may be subject to fees and penalties. Account holders also have the right to dispute any discrepancies or errors related to canceled checks, such as unauthorized transactions or incorrect amounts. In these cases, they should contact their bank to initiate an investigation and resolve the issue. Payees also have rights and obligations related to canceled checks. They are responsible for ensuring that the checks they receive are valid and for promptly presenting them to their banks for processing. If a check is canceled, the payee has the right to seek payment through alternative methods or pursue legal action if necessary. Payees also have the right to dispute any discrepancies or errors related to canceled checks, such as unauthorized transactions or incorrect amounts. In these cases, they should contact their bank and the check writer to resolve the issue. In the case of canceled checks, legal protection and liability may depend on the circumstances surrounding the cancellation. For example, if a check is canceled due to insufficient funds, the check writer may be held legally responsible for the unpaid amount and any associated fees or penalties. On the other hand, if a check is canceled due to a stop payment request or fraudulent activity, the account holder and the payee may have legal protections in place to help resolve the issue and determine liability. In any case, it's essential for both parties to understand their rights and obligations and to seek legal advice if necessary. Electronic payments, such as direct deposit and wire transfers, offer a more secure and efficient alternative to traditional checks. These payment methods allow for the immediate transfer of funds between accounts, reducing the risk of errors and fraud. Many banks now offer online banking services that allow account holders to manage their accounts, make payments, and transfer funds electronically. This can help reduce the reliance on paper checks and make it easier to track and verify transactions. Digital payment platforms, such as PayPal, Venmo, and Zelle, provide another alternative to canceled checks. These platforms enable users to send and receive payments electronically, often with just a few clicks or taps on a smartphone or computer. A canceled check is a check that has been processed and cleared by the bank, indicating that the funds have been transferred from the account of the person who wrote the check to the payee's account. Canceled checks are essential in banking transactions, as they provide a record of completed transactions and can be used to verify payments and resolve disputes. The process of canceling a check involves the presentation of the check to the bank, verification of the check, marking the check as canceled, and returning the canceled check to the account holder. This process ensures the accurate transfer of funds and helps maintain a record of transactions. Checks may be canceled for various reasons, including insufficient funds, stop payment requests, fraudulent activity, or errors in the check. It is essential for both the check writer and the payee to understand the implications of canceled checks and to take appropriate action when necessary. Canceled checks play a crucial role in banking and financial transactions, providing a record of payment and evidence that funds have been transferred between parties. This documentation is useful for tax reporting, account reconciliation, and dispute resolution, as well as for tracking expenses and maintaining accurate financial records.What Is a Canceled Check?

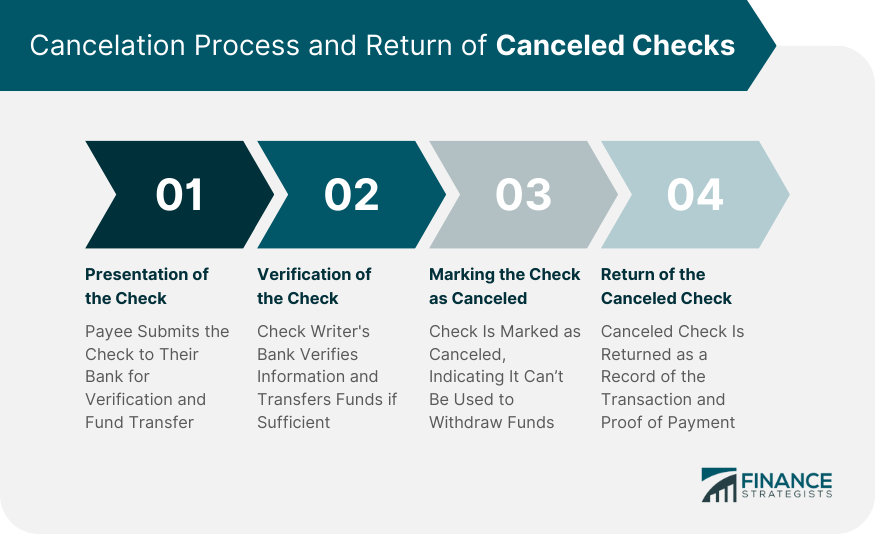

The Process of Cancelation

Presentation of the Check

Verification of the Check

Marking the Check as Canceled

Return of the Canceled Check to the Account Holder

Reasons for Canceling a Check

Insufficient Funds

Stop Payment Request

Fraudulent Activity

Error in the Check

Recordkeeping and Documentation

Bank's Responsibility in Recordkeeping

Account Holder's Responsibility in Recordkeeping

Retention Period for Canceled Checks

Legal Implications and Protections

Rights and Obligations of the Account Holder

Rights and Obligations of the Payee

Legal Protection and Liability in Case of Canceled Checks

Alternatives to Canceled Checks

Electronic Payments

Online Banking Services

Digital Payment Platforms

Final Thoughts

Canceled Check FAQs

A canceled check is a check that has been processed and cleared by the bank, indicating that the funds have been transferred from the check writer's account to the payee's account. Canceled checks serve as proof of payment and provide a record of completed transactions.

A check is marked as canceled by the check writer's bank, either by stamping it physically or marking it electronically. This indicates that the check has been processed and can no longer be used to withdraw funds.

Checks can be canceled for various reasons, including insufficient funds in the check writer's account, stop payment requests, fraudulent activity, or errors in the check.

Legal implications and protections related to canceled checks depend on the circumstances surrounding the cancellation. Both account holders and payees have rights and obligations related to canceled checks, and legal protection and liability may vary depending on the situation.

Alternatives to canceled checks include electronic payments, such as direct deposit and wire transfers, online banking services, and digital payment platforms like PayPal, Venmo, and Zelle.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.