A Certificate of Deposit (CD) is a type of time deposit offered by banks and credit unions. This type of financial product is a safe, low-risk investment that allows you to deposit a fixed sum of money for a set period, known as the term. In return, the financial institution pays you interest, typically at a higher rate than what you'd get from a regular savings account. CDs are federally insured, making them almost risk-free. CDs can play a vital role in financial planning, particularly for those with low-risk tolerance or specific short-to-medium term financial goals. They offer a reliable way to grow your money, albeit at a slower pace compared to more volatile investments like stocks. Due to their safety and predictable return, CDs are an attractive option for conservative investors. CDs can also serve as a hedge against market fluctuations when used as part of a diverse investment portfolio. Your first step is choosing where to open your CD account. Banks and credit unions each have their strengths. Banks may offer a wider variety of CD types, while credit unions typically provide higher interest rates. It's crucial to research and compare different institutions based on their CD offerings, interest rates, and customer service. The type and term of the CD account can influence your return on investment. The term can range from a few months to several years, while the type can include standard, jumbo, or high-yield CDs, among others. Each type comes with its own set of terms and conditions, so it's important to understand these before making your decision. You will then need to fill out the necessary paperwork to open the account. The specifics will depend on the institution, but you'll generally need your Social Security Number (SSN), a valid form of identification, and your initial deposit. Be prepared to provide other personal and financial information as needed. The last step is making your initial deposit. Some banks require a minimum deposit, often between $500 and $1,000, but this can vary greatly. It's worth noting that the size of your deposit can influence the interest rate you receive, with larger deposits often qualifying for higher rates. The Federal Reserve (Fed) plays a significant role in determining interest rates. When the Fed increases or decreases the federal funds rate, banks often follow suit by adjusting their own rates for loans and deposits, including CDs. Thus, Federal Reserve policies can indirectly influence the earnings on your CD account. Macro-economic factors also play a part in determining CD interest rates. For example, in times of economic uncertainty, banks may lower their rates to stimulate borrowing and spending. Conversely, during periods of economic growth, rates may rise as banks have less need to attract deposits. Banks also consider their own liquidity needs and the competitive landscape. If a bank needs to increase its liquidity, it may offer higher interest rates to attract more depositors. Furthermore, banks often adjust their rates to stay competitive within the market, aiming to balance attractive returns for depositors with their own profit margins. Generally, longer-term CDs come with higher interest rates. Banks reward you for letting them use your money for an extended period. Therefore, if you're looking to maximize your returns and don't require immediate access to your funds, a longer-term CD could be a beneficial choice. The term of a CD refers to the length of time until the CD reaches its maturity date. Common terms include three months, six months, one year, and five years, though terms can be as long as 10 years. The term you choose will directly impact your return and the length of time your funds are inaccessible. Choosing the right term length depends on your financial goals and liquidity needs. Shorter terms provide quicker access to your funds, while longer terms usually offer better returns. It's a balancing act between the desire for high returns and the need for liquidity. When your CD matures, you have a few options. You can cash it out, reinvest the money into another CD, or, if your bank offers a grace period, you can make additional deposits or withdrawals. Some banks may automatically renew your CD if you don't provide instructions during the grace period, so it's important to be proactive. Withdrawing from your CD before it matures usually comes with a penalty, often in the form of forfeited interest. It's essential to be aware of these potential consequences before investing in a CD. In most cases, you should only invest funds that you can afford to leave untouched for the duration of the term. With simple interest, you only earn interest on the initial amount deposited. However, compound interest enables you to earn interest on your initial deposit plus the interest that has already been added to your account. This means you're earning 'interest on interest,' which can make a significant difference over time. How often interest is compounded in a CD can vary from one institution to another. It can be daily, monthly, or annually, and this can significantly impact your overall return. As a general rule, the more frequently interest is compounded, the greater your returns will be. Compounding has a snowball effect on your savings. The more frequently interest is compounded, the more you earn. Over time, even a slightly higher interest rate or a slightly more frequent compounding schedule can lead to significantly higher returns, particularly for long-term CDs. Imagine you invest $10,000 in a CD with a term of five years and an annual interest rate of 2%, compounded annually. At the end of five years, you'll have about $11,040. Now, consider a similar account, but with interest compounded monthly. In this case, you'll end up with about $11,048. While this difference may seem small, it becomes more significant with larger deposits and longer terms. Laddering involves investing in multiple CDs with different maturity dates. This strategy provides a balance between higher returns and regular access to funds, mitigating the risk of tying up all your money in long-term CDs. By staggering the maturity dates, you also protect yourself against interest rate fluctuations and gain the flexibility to take advantage of higher rates as they become available. The barbell strategy involves investing half your money in short-term CDs and the other half in long-term CDs. This allows you to take advantage of higher interest rates on long-term CDs while still maintaining some liquidity. The short-term CDs provide funds for immediate needs, while the long-term CDs earn higher interest for future use. The bullet strategy is where you buy CDs that all mature at the same time. This strategy could be useful if you know you'll need a large sum of money at a specific future date. By aligning your CD maturities with your future cash needs, you ensure that your funds are accessible exactly when you need them. Different banks offer different terms and interest rates, so it's worth shopping around to find the best fit for your financial goals and risk tolerance. An institution with a slightly higher interest rate could lead to significantly higher earnings over the term of your CD. However, always make sure to also consider other factors, such as penalties for early withdrawal and the bank's reputation. Your financial goals and liquidity needs should guide your choice of CD. If you need easy access to your funds, a short-term CD or a CD with a mild early withdrawal penalty might be best. On the other hand, if you're saving for a long-term goal and don't need immediate access to your funds, a longer-term CD with a higher interest rate might be the better choice. Finally, the reputation and financial stability of the bank should be considered. A bank with a strong track record and sound financial health is more likely to provide reliable service and security for your investment. Online reviews, financial news, and the bank's financial statements can all provide insights into its reputation and stability. Certificates of Deposit (CDs) are an attractive investment option for individuals seeking a low-risk, predictable return on their money. From understanding the CD opening process, recognizing factors that affect interest rates, selecting the suitable term length, comprehending compounding principles to adopting the best strategy for maximum benefits – knowledge is your most powerful tool. Different institutions offer various terms and interest rates, so consider your financial goals, risk tolerance, and the institution's reputation when making your decision. Remember, smart and informed decisions today pave the way for a secure financial future. Embark on your financial journey today by seeking banking services to open a CD account that aligns with your financial goals.Certificate of Deposit (CD) Overview

How Do CD Accounts Work?

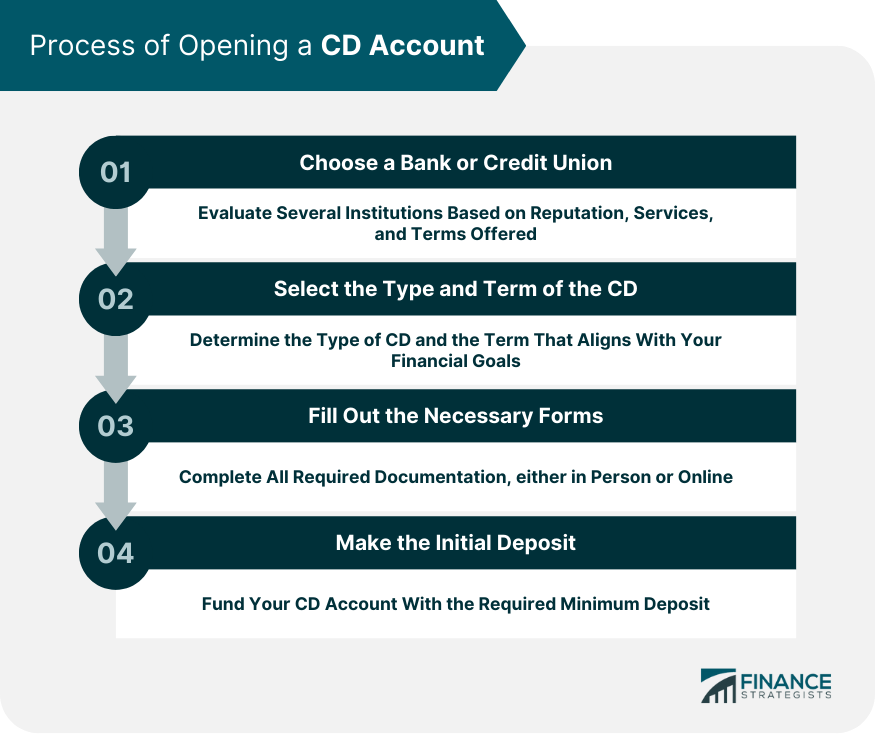

Opening a CD Account

Choose a Bank or Credit Union

Select the Type and Term of the CD

Fill Out the Necessary Forms

Make the Initial Deposit

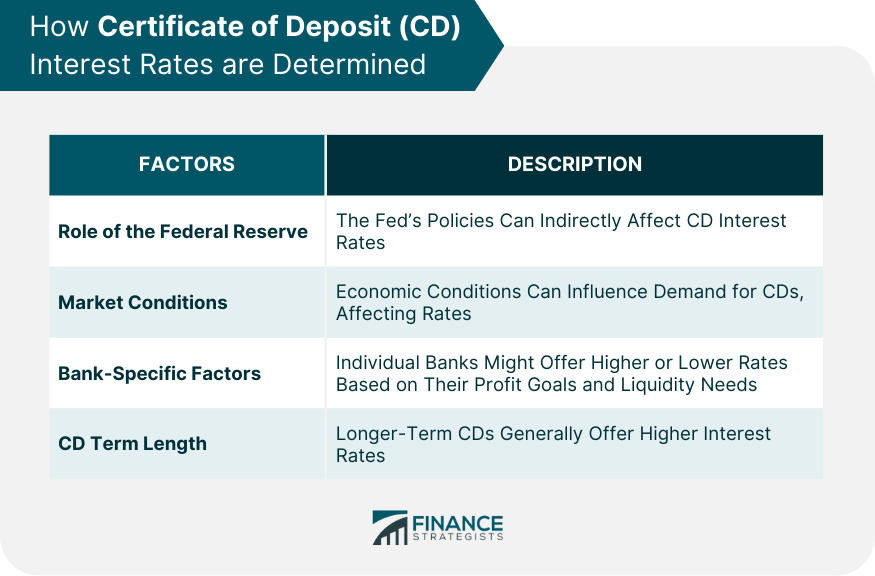

How CD Interest Rates Are Determined

Role of the Federal Reserve

Market Conditions

Bank-Specific Factors

CD Term Length

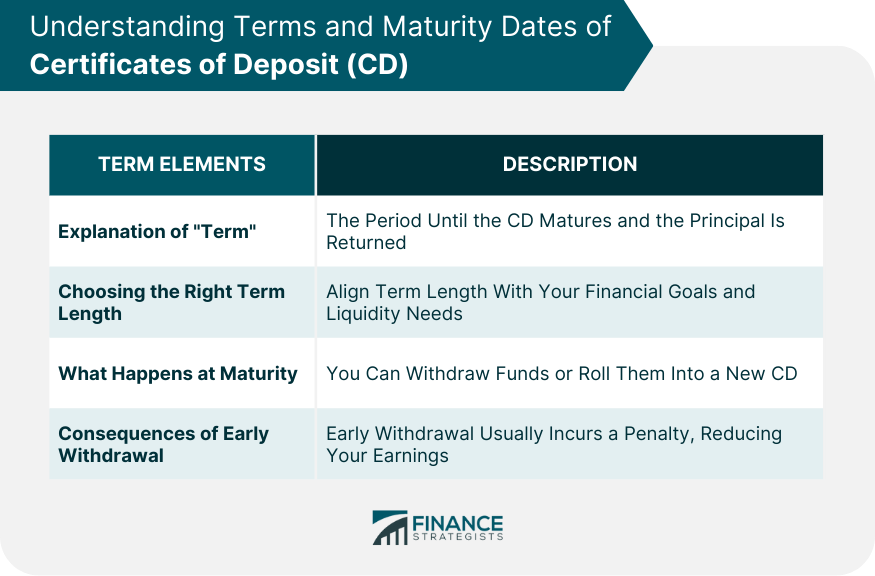

Understanding Terms and Maturity Dates of CDs

Explanation of "Term"

Choosing the Right Term Length

What Happens at Maturity

Consequences of Early Withdrawal

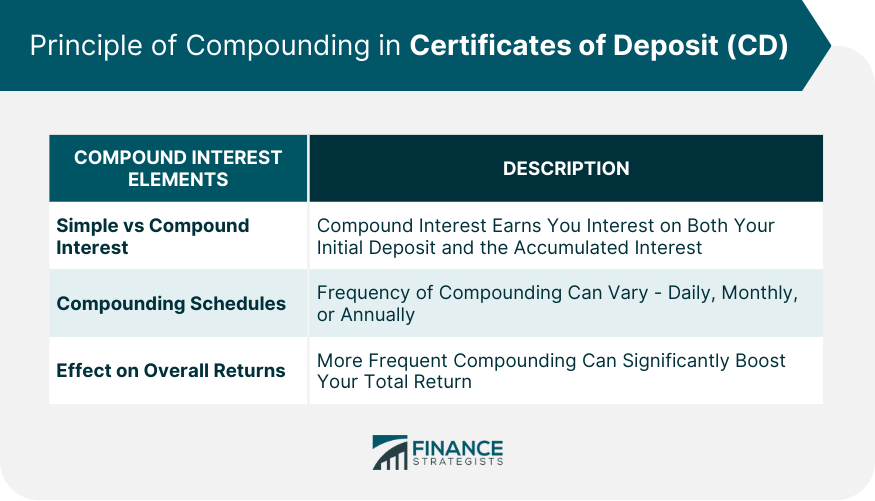

Explaining the Principle of Compounding

Simple vs Compound Interest

How Often Interest Is Compounded in CDs

Effect of Compounding on Overall Returns

Examples to Illustrate Compounding

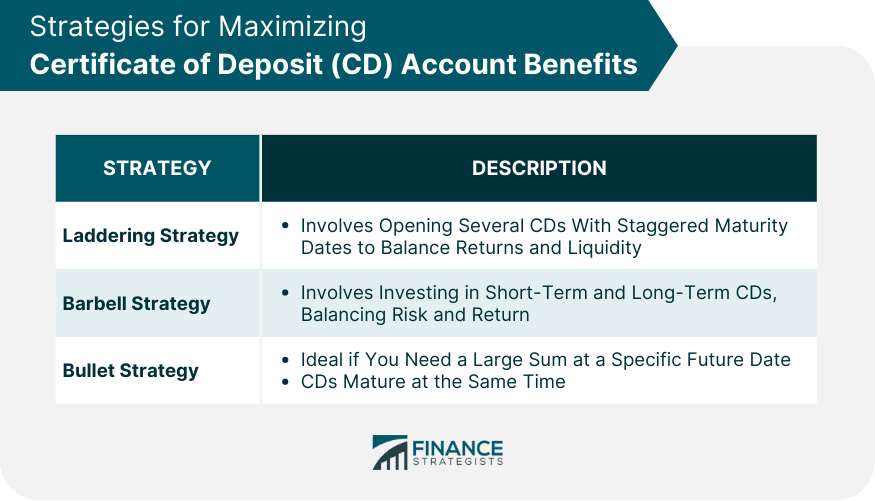

Strategies for Maximizing CD Account Benefits

Laddering Strategy

Barbell Strategy

Bullet Strategy

Things to Consider When Choosing a CD Account

Comparison of Terms and Interest Rates

Understanding Your Financial Goals and Liquidity Needs

Reputation and Financial Stability of the Bank

Bottom Line

Understanding How CD Accounts Work FAQs

A Certificate of Deposit (CD) is a time deposit offered by banks and credit unions that pays interest over a set term.

CD interest rates are influenced by the Federal Reserve's policies, market conditions, bank-specific factors, and the CD term length.

The 'term' in a CD account refers to the length of time until the CD reaches its maturity date.

Compounding in a CD account refers to earning interest on your initial deposit plus the interest that has already accumulated.

Laddering, barbell, and bullet strategies can be used to balance returns and liquidity, and to mitigate the risks associated with interest rate fluctuations.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.