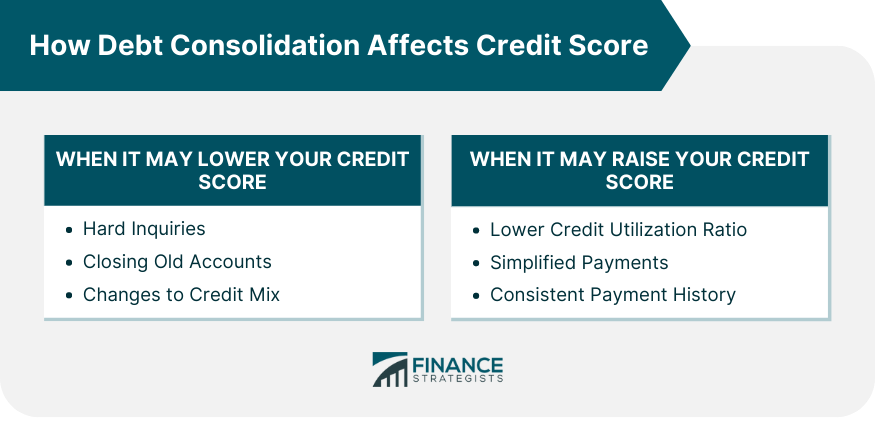

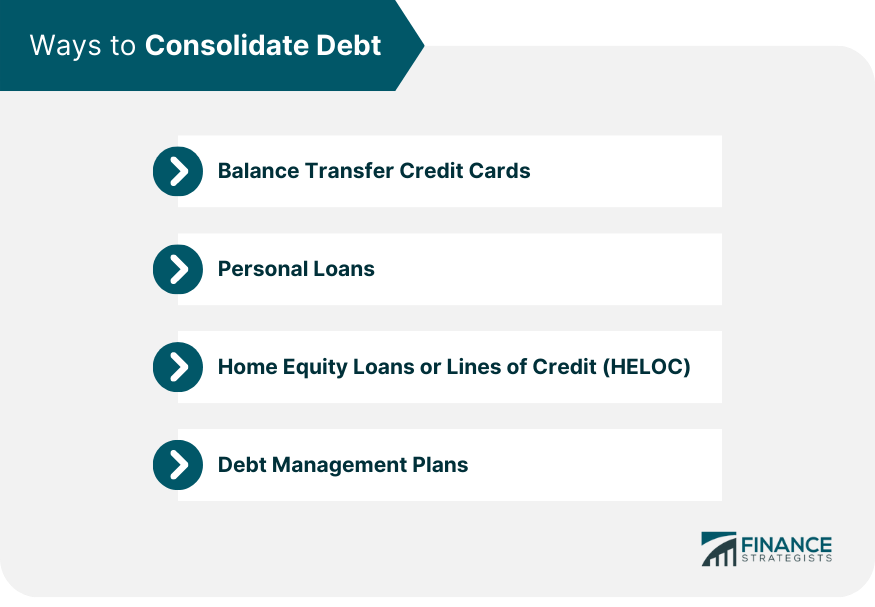

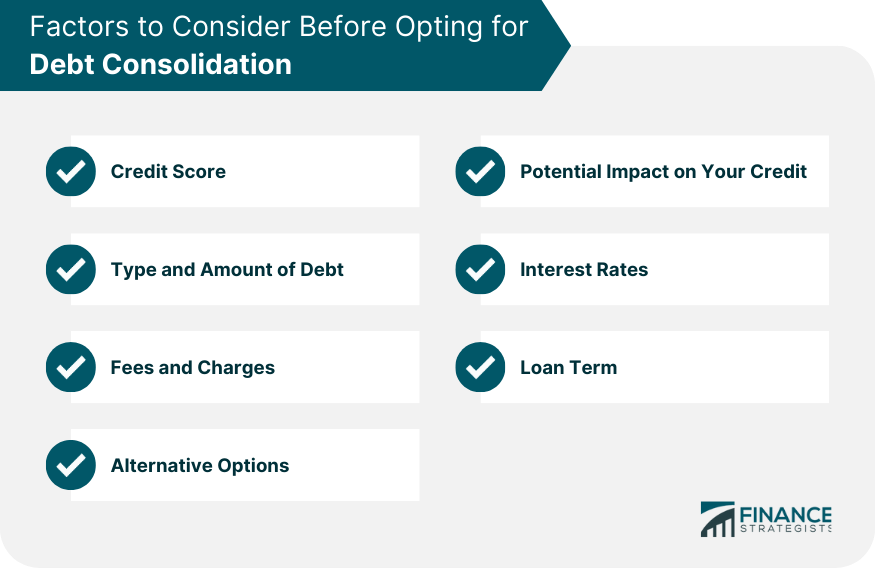

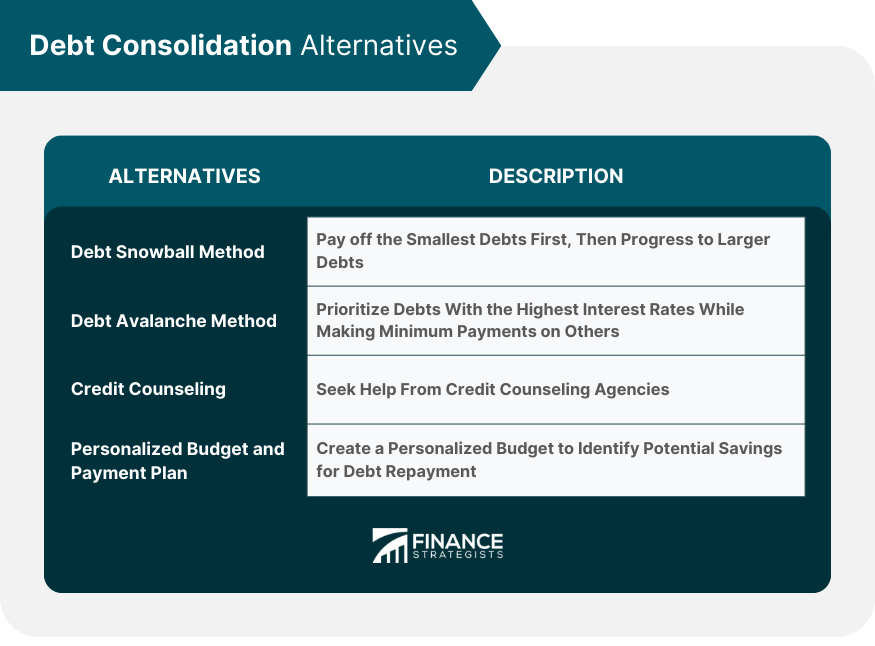

Debt consolidation involves merging multiple debts into one unified loan, often with the intent of securing lower monthly payments or achieving reduced interest rates. While this method offers a simplified solution for those juggling various debts, it's imperative to recognize its potential ramifications on your credit score. A credit score serves as a metric of an individual's financial reliability and plays a pivotal role in numerous financial decisions. It not only determines loan eligibility and interest rates but can also impact housing opportunities and potential employment offers. Given its importance, grasping the influence of debt consolidation on one's credit score becomes vital before making such a decision. Depending on your chosen method for debt consolidation, its impact on your credit score can vary in several ways. Debt consolidation can sometimes lead to a temporary dip in your credit score. Here are some reasons why this might happen: Hard Inquiries: When you apply for a debt consolidation loan, lenders will often perform a hard inquiry on your credit history to determine your creditworthiness. These inquiries can cause a slight decrease in your credit score. Closing Old Accounts: Debt consolidation usually involves paying off old debts, which could lead to closing old accounts. This process can lower the average age of your credit accounts, an important factor in credit score calculations. Changes to Credit Mix: When you consolidate, particularly if you're moving from multiple credit types (credit cards, auto loans, etc.) to a single loan, it might make your credit mix less diverse, potentially lowering your score. Contrary to the potential negatives, debt consolidation can also present opportunities for improving your credit score: • Lower Credit Utilization Ratio: By consolidating high-interest credit card debt into a personal loan, you can lower your credit utilization rate - the ratio of your credit card balances to their limits. Credit utilization is a key component of your credit score, and a lower rate can have a positive effect on your score. • Simplified Payments: Consolidating multiple debts into one loan simplifies your payment structure. You'll only have one payment date, interest rate, and loan balance to manage. This can result in fewer missed or late payments, which can boost your credit score. • Consistent Payment History: By ensuring regular and timely payments on your new loan, you create a consistent payment history. Over time, this reliability can considerably enhance your score. There are several ways to consolidate debt: Balance Transfer Credit Cards: These cards often offer introductory 0% APR periods. You can transfer balances from other cards and pay no interest for a set period. Personal Loans: These are fixed-term loans that you can use to pay off other debts. They often have lower interest rates than credit cards. Home Equity Loans or Lines of Credit (HELOC): If you own a home, you might qualify for these loans based on your home's equity. However, your home becomes the collateral. Debt Management Plans: These are programs offered by credit counseling agencies. They negotiate with creditors to lower your interest rates and monthly payments. If you're contemplating debt consolidation, it's vital to weigh various factors before making a decision. Here's a comprehensive look at the considerations to keep in mind: Your current credit score can significantly influence the terms of a debt consolidation loan. Those with higher scores are likely to receive better interest rates. If your score is on the lower side, you might want to consider strategies to improve it before opting for consolidation. Though debt consolidation can streamline your payments and potentially improve your credit over time, the initial act of opening a new loan and closing multiple accounts can temporarily lower your score. Being aware of this impact will help you make a more informed decision. Different types of debts come with their own sets of terms and conditions. For example, consolidating secured debts like mortgages might differ from unsecured debts such as credit cards. Also, evaluate the total amount you owe. If your debt is relatively small and you believe you can pay it off in a year, consolidation might not be worth the effort or costs. One of the primary reasons people opt for debt consolidation is to secure a lower interest rate. It's imperative to compare the interest rates of your current debts with the rate offered for a consolidation loan. If the consolidation loan doesn't provide a significantly lower rate, it may not offer the cost savings you're seeking. Many debt consolidation options come with fees, such as origination fees, balance transfer fees, or early repayment penalties. These charges can eat into the savings you'd make from a lower interest rate. Always ensure you're aware of all costs associated with a consolidation loan to determine if it's financially worthwhile. While a longer loan term might offer the allure of smaller monthly payments, it also means you'll be in debt for a more extended period. Moreover, a longer term can result in more interest paid over the life of the loan. Assess how comfortable you are with the duration of the loan and its long-term implications. Before committing to debt consolidation, explore other avenues of debt relief. Options like debt settlement, credit counseling, or even bankruptcy might be more suited to your unique financial situation. If you're contemplating alternatives to debt consolidation, here are several strategies you can explore: Endorsed by several financial experts, this method is designed to build momentum in debt repayment. You begin by listing all your outstanding debts, from the smallest to the largest, regardless of their interest rates. You then pay off the smallest debt while paying minimum amounts on the others. Once the smallest debt is cleared, you direct the funds previously allocated to it to the next smallest debt. The idea is that as you clear off each debt, your confidence and determination grow, much like a snowball growing as it rolls downhill. Though it can be immensely satisfying to see debts cleared quickly, a potential drawback is that you might end up paying more interest over time if larger debts also come with higher interest rates. In contrast to the Snowball approach, the Debt Avalanche Method targets the most mathematically significant debts first. You categorize your debts starting with the highest interest rate. The primary focus then becomes paying off the debt with the highest interest while maintaining minimum payments on the others. Over time, this method can save you more in interest. It's a strategy designed for those who are driven by numbers and are looking for long-term financial efficiency. However, it may not offer the quick psychological wins that the snowball method does, which can be motivating for some individuals. For those feeling the weight of their financial obligations, credit counseling can offer a lifeline. Credit counseling agencies provide invaluable sessions with certified counselors who can review your financial situation holistically. After understanding your unique financial challenges, many of these agencies can help devise a Debt Management Plan—a structured repayment strategy that might come with reduced interest rates or eliminated fees. An added advantage is that these counselors can negotiate better repayment terms with your creditors. However, it's essential to choose a reputable agency, as some might charge exorbitant fees or might not have your best interests at heart. Taking the reins of your financial destiny often begins with a thorough understanding of your income and expenses. A personalized budget outlines your monthly earnings against your fixed and variable costs, offering clarity on where your money goes. By identifying and then trimming unnecessary expenditures, you can reallocate funds to expedite debt repayment. Discipline and financial literacy can be improved by this technique, as well as having feasible financial goals and possibly automating payments. The challenge lies in adhering to the budget and continuously revisiting and adjusting it as life circumstances change. Debt consolidation can be a valuable tool for simplifying payments and potentially improving your credit score over time. However, it is crucial to understand its potential impact on your credit before making a decision. Consolidating debts may lead to a temporary dip in your credit score due to hard inquiries. On the other hand, it can raise your credit score by lowering your credit utilization ratio, consistent payment history, and simplifying payment structures. Before opting for debt consolidation, consider factors such as your current credit score, the potential impact on your credit, and explore alternative options like the debt snowball and debt avalanche methods, credit counseling, and personalized budgeting. Remember that responsible financial management and a clear understanding of your unique financial situation are essential in making the most informed decision for your financial future.Debt Consolidation and Credit Score

How Debt Consolidation Affects Credit Scores?

When Debt Consolidation May Lower Your Credit Score

When Debt Consolidation May Raise Your Credit Score

Ways to Consolidate Debt

Factors to Consider Before Opting for Debt Consolidation

Credit Score

Potential Impact on Your Credit

Type and Amount of Debt

Interest Rates

Fees and Charges

Loan Term

Alternative Options

Debt Consolidation Alternatives

Debt Snowball Method

Debt Avalanche Method

Credit Counseling

Personalized Budget and Payment Plan

Conclusion

How Does Debt Consolidation Affect Your Credit Score? FAQs

Debt consolidation can impact your credit score in both positive and negative ways. It may cause a temporary dip due to hard inquiries and changes in the credit mix, but it can also raise your score by improving your payment history and lowering credit utilization.

In some cases, yes. Debt consolidation can lead to a temporary decrease in your credit score due to hard inquiries and closing old accounts. However, with responsible repayment, it can eventually improve your score.

Yes, debt consolidation can improve your credit score over time. By making timely payments and lowering your credit utilization ratio, you can positively impact your credit score.

The potential negatives of debt consolidation on your credit score include temporary score dips due to hard inquiries, closing old accounts, and potential changes in the credit mix.

Consolidating high-interest credit card debt into a personal loan or using a balance transfer credit card with a 0% APR period can be beneficial for credit scores. By lowering credit utilization and maintaining consistent payments, these methods can positively affect your credit score.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.