A credit union is a kind of financial organization that is owned and controlled by its members, who are also its customers. It operates as a cooperative, meaning all profits are returned to its members through lower loan rates, higher interest on deposits, and other benefits. Credit unions are not-for-profit organizations. They are not driven by the goal of maximizing profits for shareholders. Instead, they exist to serve the financial needs of their members. Any surpluses produced by the credit union are reinvested back for the members. Credit unions provide various financial services, including savings accounts, checking accounts, loans, mortgages, credit cards, and investment products. They may also offer other services, such as financial education and counseling. Recently, online banking and mobile banking services have been added to the list of services offered by some credit unions. Additionally, most credit unions offer exclusive benefits and better customer service than traditional banks. Members of a credit union typically have to meet certain qualifications before they can join. They pool their funds together, allowing the credit union to create a source of loans, products, and a wide range of financial services to offer its members. Credit unions may pay back any excess profits to members as dividends and direct them towards improved or additional services for members. Interest charged on loans to members creates an income for the credit union, which is used to pay for operational expenses. Each credit union member gets a say in how the institution is run, allowing them to cast votes for the board of directors’ selections and other relevant decisions rather than wealthy shareholders dictating the rules. Bank deposits are insured by the Federal Deposit Insurance Corporation (FDIC). In contrast, federally chartered credit unions are insured by the National Credit Union Administration (NCUA), while those that operate under state law usually carry private insurance. Becoming a member of a credit union can offer several advantages. Here are three key benefits of credit union membership: Credit unions are not-for-profit organizations and are not obligated to pay corporate income tax on any profits earned. Because of this, they can often provide better rates than traditional banks. Members can get better deals on car loans, mortgages, student loans, and other types of financing. Some credit unions may also offer incentives such as loan deferrals or deferred payment options for those facing financial difficulties. Credit unions usually offer higher interest rates on savings accounts than traditional banks. Members can earn more interest on their deposits and grow their savings faster. There is usually a strong commitment between members to help each other out. Even if the current economic climate causes savings to lose value due to inflation or market volatility, there is still potential for other members to contribute and protect the investments within the community. Being part of a credit union provides personalized service. This could include anything from having specialist staff available who are dedicated solely to helping members understand different financial products or providing personal advice about debt management and budgeting. They are smaller, community-based institutions, meaning members can form relationships with the staff and receive more personalized attention. This can make banking more convenient and enjoyable for members. Credit unions offer numerous advantages, but it is important to be aware of the limitations that come with being a member: One downside to credit unions is that since they tend to be small-scale organizations, they usually have fewer physical branch locations. If an individual lives outside their credit union's region, accessing their funds in person may take time and effort. This can also make it challenging to receive face-to-face customer service. Some credit unions may also have fewer ATMs available, which can cause additional problems for members who need to withdraw money. Another limitation associated with using a credit union is the number and variety of products and services they offer compared to regular banks. Most credit unions will likely not have all the different types of accounts that might be found at a big bank. This can include limited investment options, fewer loan products, and a narrower range of financial products and services. Even if they do have these accounts, they probably will give fewer options when it comes to things like overdraft protection or loan products. Credit unions often have limited operating hours. It can be difficult for members to gain access to their accounts or get customer service after regular business hours, particularly for those who need access during weekends or holidays. When it comes to digital and online banking, credit unions may not be as technologically advanced as traditional banks and may not offer the same range of services. Mobile banking, online bill payments, and electronic account transfer services may not always be available. Membership criteria and restrictions vary for each credit union. However, typical requirements include being a resident of the same geographic region, working for a specific employer, or belonging to an affiliated organization or association. Some credit unions also have restrictions based on membership in a specific group or organization. For example, a credit union might be open only to employees of a particular company or members of a specific labor union. Once membership eligibility is secured, individuals typically need to open a savings account with a minimum deposit to become a member. Potential members should also consider any fees associated with becoming a member, such as annual maintenance fees. Determining eligibility for credit union membership involves researching credit unions in the area and checking membership requirements via their website or contacting them directly to find out more about their specific requirements. Traditionally, joining a credit union helps build and strengthen the financial well-being of a local community. The membership gives access to great banking solutions while contributing towards the greater good. The first step in joining a credit union is researching local options. Check out websites or call them to find out their membership eligibility. This typically includes location, working for specific employers, or belonging to particular associations. Review factors such as their services, interest rates, fees, and operating hours, and compare the options to determine which credit union is the most suitable. Also, confirm whether the credit union you are considering offers the products that you require. The next step is to fill out an application form, which can be found at the local branches or on the respective credit union's website. It is important that the information provided is accurate and checked for any discrepancies before submitting it for the process to go smoothly. After submitting the application form, open an account and complete additional paperwork, if needed. Once all this has been achieved, the new account should be ready for use. Credit unions and banks offer similar services, but there are some notable differences between the two that can be crucial when deciding which one to use for financial needs. Credit unions are nonprofit organizations owned by their members, while banks are privately or publicly-owned businesses run with their shareholders’ profit in mind. This difference allows credit unions to offer more competitive rates on fees and interest. Membership in credit unions is often limited to certain people, such as those who live in the same area, work for a particular company, or share a common bond. Banks, however, tend to be open to anyone with money to deposit or borrow. Credit unions usually only operate within a small area – such as a city or county – while banks often have numerous branches across multiple states. Moving away makes it difficult to continue banking with a credit union, while doing so at most big banks would still be an option. When it comes to product offerings, most credit unions and banks offer similar products. However, banks offer greater loan limits owing to their more significant deposits, and banks can provide a wide variety of more specialized services, such as international banking. Costs associated with running a credit union are much lower than those for running a bank, so credit unions offer better rates and affordable options on things like mortgages due to their nonprofit status. In contrast, some banks may charge higher fees for their services. Deposits at banks are insured by the FDIC, while the NCUA insures deposits at credit unions. Both organizations offer up to $250,000 in insurance per account holder in the event of an institutional failure. Credit unions are nonprofit institutions that are owned by their members. All profits are returned to its members through lower loan rates, higher interest on deposits, and other benefits. Members pool their funds together to create a source of financial services for their members. Eligibility differs from one institution to another. Some standard criteria include residing in the same area, being employed by a particular company, or having a connection to a specific organization or association. Credit unions are advantageous because they offer competitive rates and fees, fewer fees overall, more personalized service, and a sense of community. However, they may not have the same access due to their limited branches. Compared to traditional banks, their products, services, operating hours, and technology tend to be more limited. For example, they may not have international banking capabilities and do not always offer the scale offered by regular banks. Generally, credit unions and banks differ in structure, membership, service areas, product offerings, affordability, and insurance. But overall, credit unions are an excellent option for those looking for quality financial services at affordable fees and competitive ratesWhat Is a Credit Union?

How Credit Unions Work

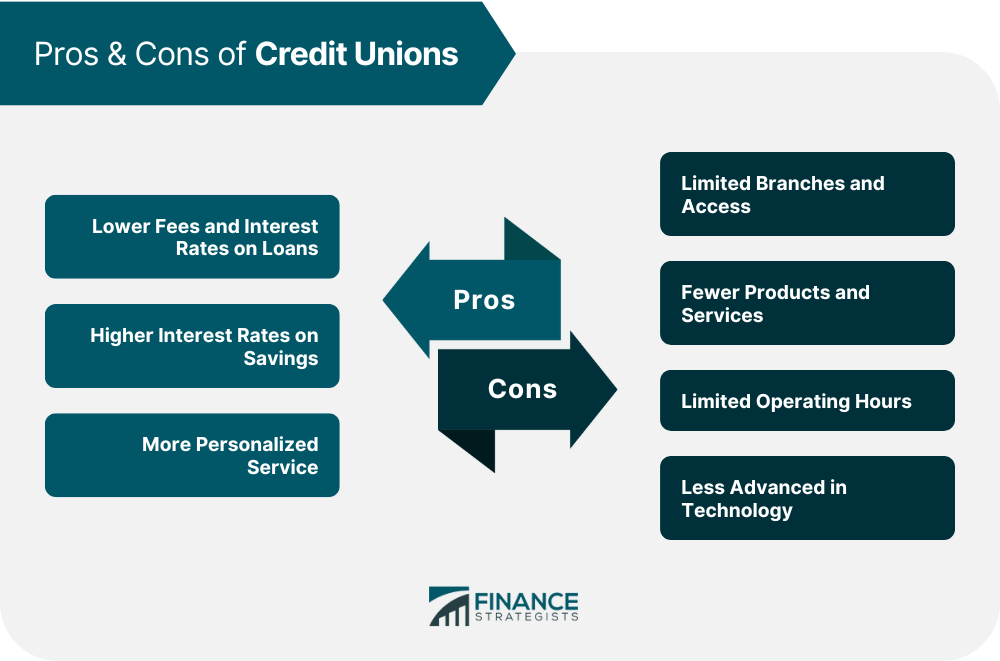

Advantages of Credit Unions

Lower Fees and Interest Rates on Loans

Higher Interest Rates on Savings

More Personalized Service

Disadvantages of Credit Unions

Limited Branches and Access

Fewer Products and Services

Limited Operating Hours

Less Advanced in Technology

Credit Union Membership Requirements

How to Join a Credit Union

Credit Unions vs Banks

Structure

Membership

Service Areas

Product Offerings

Affordability

Insurance

Final Thoughts

Pros and Cons of Credit Unions FAQs

The key difference between a bank and a credit union is their structure. Banks are privately or publicly owned businesses that seek profit, while credit unions are nonprofit organizations owned by their members. The differences in structure can have notable effects, such as credit unions being able to offer more competitive rates on fees and interest. Credit unions also typically have a limited membership base that requires criteria to be met, whereas banks tend to be open to anyone with money.

Credit unions typically offer more competitive rates on fees and interest and fewer fees overall than banks. Additionally, they are known for providing a more personal touch as members can get to know the staff who work at their credit union. Credit unions also often offer members rewards and access to exclusive products or services, such as special loan offers. Finally, many credit unions have a sense of community that banks may not offer

Credit unions make money by earning income from the interest on loans, the fees charged for services, and the profits from investment activities. Additionally, they may earn income from non-interest-bearing accounts and other sources, such as investments in securities.

No, not everyone is eligible to join a credit union. Credit unions typically have specific eligibility criteria for membership, including factors such as residing in a particular geographic area, working for a specific employer, or belonging to a particular organization or association.

Credit unions typically have fewer branches, products, and operating hours than banks. Additionally, they may not have access to international banking services or the same scale of services that regular banks can provide. Additionally, digital banking with credit unions may be more limited than with banks.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.