Suspicious Activity Reports are documents filed by financial institutions, such as banks, to report suspected criminal activity or violations of money laundering or terrorist financing laws. SARs are required under the Bank Secrecy Act (BSA) of 1970, which requires financial institutions to assist the U.S. government in detecting and preventing money laundering. Filing a SAR does not necessarily mean that a crime has occurred, but it alerts law enforcement agencies to potentially suspicious activities so that they can investigate further. The Bank Secrecy Act, enacted in 1970, laid the groundwork for SARs in the United States. The BSA requires financial institutions to maintain records, report cash transactions over a certain threshold, and submit SARs for any suspicious activities that may indicate a financial crime. FinCEN is a U.S. Department of the Treasury bureau that collects, analyzes, and disseminates financial intelligence to combat money laundering, terrorist financing, and other financial crimes. FinCEN establishes regulations and guidelines for SARs, sets reporting thresholds, and provides a platform for filing SARs electronically. Additionally, FinCEN shares SARs information with law enforcement agencies to aid in investigating and prosecuting financial crimes. The USA PATRIOT Act, enacted in 2001, expanded the BSA's scope and enhanced anti-money laundering (AML) regulations, including SARs reporting requirements. The act broadened the definition of financial institutions subject to SARs reporting and increased the penalties for non-compliance. The FATF is an intergovernmental organization that sets international standards for combating money laundering and terrorist financing. The FATF's recommendations form the basis for AML and SARs regulations in many countries. The European Union has issued a series of AML directives that establish a regulatory framework for combating money laundering and terrorist financing in EU member states. These directives set out the requirements for reporting suspicious activities, including SARs, and provide guidance on implementing AML programs. Other international bodies, such as the United Nations, the International Monetary Fund, and the World Bank, also issue guidance and recommendations on AML and SARs. Financial institutions that are required to file SARs include: Money service businesses (MSBs) Casinos and gaming institutions Other entities, such as insurance companies and real estate professionals, depending on the jurisdiction Financial institutions subject to SARs reporting must: Establish AML programs, including policies, procedures, and internal controls Identify and report suspicious activities that may indicate financial crime Maintain records and documentation related to SARs for a specified period Train staff and designate compliance officers to ensure adherence to AML regulations Ensure data privacy and protection in accordance with applicable laws Financial institutions should be vigilant for the following indicators of suspicious activities: Unusual transaction patterns or volumes Inconsistent customer behavior with their profile or expected activity Transactions lacking economic or business rationale Evasion of reporting requirements, such as structuring transactions to avoid thresholds Use of complex or multiple accounts to obscure the origin or destination of funds Different financial products may present unique risks and indicators of suspicious activities: Cash Transactions: Large cash deposits or withdrawals, unusual patterns, or transactions inconsistent with customer behavior Wire Transfers: Frequent, high-volume transfers to or from high-risk jurisdictions, or transfers with incomplete or nonsensical information Securities and investments: Rapid and unexplained trading patterns, market manipulation, or insider trading Trade Finance and Export/Import Businesses: Over- or under-invoicing, misrepresentation of goods, or transactions with sanctioned countries Cryptocurrency Transactions: Transactions involving privacy-focused cryptocurrencies, mixing services, or unregistered exchanges The process of filing SARs typically involves: Internal Identification and Investigation: Compliance officers and staff detect and investigate potential suspicious activities Decision-Making Process: Compliance officers determine whether to file a SAR based on the results of the investigation Filing the Sar With the Relevant Authority: The financial institution submits the SAR electronically through the designated platform A SAR should include: Reporting Entity Information: Identification and contact details of the financial institution Customer and Transaction Details: Identification of the parties involved and a description of the transaction(s) Description of Suspicious Activity: A detailed narrative explaining why the activity is considered suspicious Supporting Documentation and References: Any relevant documents or information that support the suspicion SARs are subject to strict confidentiality requirements. Financial institutions and their employees may not disclose the existence or content of a SAR to any person, including the subject of the report. Non-compliance with these requirements may result in civil and criminal penalties. However, "safe harbor" provisions protect financial institutions from legal liability for filing SARs in good faith. Law enforcement agencies use SARs to: Identify potential financial crimes and prioritize investigations Investigate and prosecute money laundering, terrorist financing, and other financial crimes, often in conjunction with other financial intelligence Effective collaboration between financial institutions and law enforcement can enhance the detection and prevention of financial crime. This cooperation may involve: Information sharing through formal channels, such as public-private partnerships Joint investigations and initiatives to target specific threats or criminal networks Suspicious Activity Reports are an important tool in the fight against financial crimes. SARs are documents filed by financial institutions to report suspected criminal activity or violations of money laundering or terrorist financing laws. They must be filed with the Financial Crimes Enforcement Network and are required under the Bank Secrecy Act of 1970. The legal and regulatory framework of SARs includes the BSA, FinCEN, the Financial Action Task Force, the European Union's Anti-Money Laundering Directives, and other international regulations. Reporting entities subject to SARs reporting must establish AML programs, identify and report suspicious activities, maintain records and documentation related to SARs, train staff, and ensure data privacy and protection. Financial institutions should be vigilant for common indicators of suspicious activities and red flags related to specific financial products. The SARs reporting process involves internal identification and investigation, decision-making, and filing the SAR with the relevant authority. SARs are subject to strict confidentiality requirements, and law enforcement agencies use them to identify potential financial crimes and prioritize investigations. Effective collaboration between financial institutions and law enforcement can enhance the detection and prevention of financial crime.What Are Suspicious Activity Reports (SARs)?

SARs are used to flag potential criminal activity, such as transactions involving large amounts of money inconsistent with the account holder's known income or transactions with no apparent business or lawful purpose.

SARs must be filed with the Financial Crimes Enforcement Network (FinCEN), which is a bureau of the U.S. Department of the Treasury responsible for collecting and analyzing information related to financial crimes.

The filing of SARs is an important tool in the fight against financial crime and helps to ensure that the U.S. financial system is not used to facilitate illegal activities.Legal and Regulatory Framework of Suspicious Activity Reports (SARs)

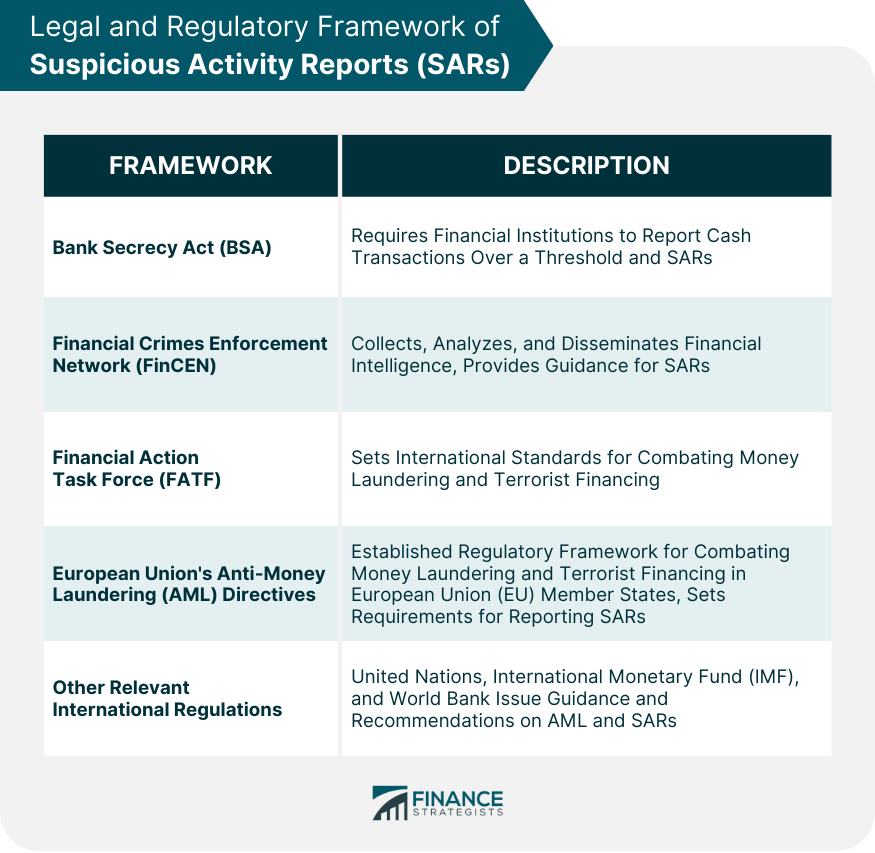

The Bank Secrecy Act and Its Impact on SARs

The Financial Crimes Enforcement Network

FinCEN oversees the implementation of the BSA and issues guidance for financial institutions regarding SARs.FinCEN's Role in SARs Regulation

The USA PATRIOT Act and Its Influence on SARs

International Regulations and Guidelines

Financial Action Task Force (FATF)

European Union's Anti-Money Laundering Directives

Other Relevant International Regulations

Reporting Entities and Their Obligations

Financial Institutions Subject to SARs Reporting

Requirements for Reporting Entities

Identifying Suspicious Activities

Common Indicators of Suspicious Activities

Red Flags Related to Specific Financial Products

Filing SARs

SARs Reporting Process

Contents of a SAR

SAR Confidentiality and Disclosure

SARs and Law Enforcement

How Law Enforcement Agencies Use SARs

Cooperation Between Financial Institutions and Law Enforcement

Conclusion

Suspicious Activity Reports (SARS) FAQs

A Suspicious Activity Report (SAR) is a document that financial institutions file with the Financial Crimes Enforcement Network (FinCEN) to report suspicious transactions that may indicate potential criminal activity, such as money laundering or fraud.

Under the Bank Secrecy Act (BSA), financial institutions, including banks, credit unions, and money services businesses, are required to file SARs if they detect suspicious activity in their customers' transactions.

Suspicious activities that should be reported in a SAR include any transaction that appears to be unusual, out of the ordinary, or inconsistent with a customer's known financial activity, which may indicate potential criminal activity, such as money laundering or terrorist financing, fraud, or cybercrime.

When a financial institution detects suspicious activity, it files a SAR with FinCEN, which analyzes the report and may share the information with law enforcement agencies to investigate potential criminal activity. SARs are confidential and protected from disclosure, except in limited circumstances.

Financial institutions that fail to file SARs when required may face significant penalties, including fines, regulatory enforcement actions, and reputational harm. In addition, failure to file SARs may impede efforts to detect and prevent criminal activity, which can have serious consequences for the financial system and society at large.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.