Bankruptcy, a legal remedy for financial burdens, enables individuals and businesses struggling with debts to turn to the courts for assistance. By filing a petition, debtors detail their assets and liabilities, seeking a fresh financial start while ensuring fairness to creditors. Yet, bankruptcy dismissal disrupts this process by abruptly terminating the case before discharge is granted. The reasons for dismissal vary, from paperwork errors to missed payments or even potential abuse of the system. The consequences of such a dismissal are profound, leaving individuals facing an uncertain financial future. Therefore, comprehending the implications and exploring alternative solutions becomes imperative to safeguarding financial stability. Bankruptcy dismissal occurs when the court chooses to terminate the bankruptcy proceedings prematurely. This can happen either with prejudice (generally due to some form of fraud, abuse, or failure to adhere to court orders) or without prejudice, meaning the debtor can usually re-file immediately if the issue that led to the dismissal is corrected. Discharge and dismissal are two terms that are often confused when discussing bankruptcy. Discharge refers to the court's decision to eliminate certain debts, freeing the debtor from personal liability for the discharged debts. On the other hand, a dismissal is when the case is closed without the debtor receiving a discharge. In other words, a discharge signifies the successful conclusion of a bankruptcy case, while a dismissal, particularly when done with prejudice, can be a significant setback. Immediately after a bankruptcy case is dismissed, the automatic stay that protects the debtor from collection activities is lifted. This means that creditors can resume collection activities, including foreclosure, repossession, wage garnishments, and lawsuits. Debtors may find themselves in a more precarious financial situation, especially if the dismissal occurred due to their inability to adhere to a court-ordered payment plan. A bankruptcy dismissal remains on the debtor's credit report for a period, usually seven years for a Chapter 13 dismissal. This could make obtaining new credit or loans more challenging, as lenders may perceive the debtor as a high-risk borrower. In addition to this, if the debtor had any delinquent accounts prior to filing for bankruptcy, the dismissal could result in these accounts becoming active again, leading to further damage to the debtor's credit rating. Bankruptcy dismissal can significantly impact a person's future financial opportunities. Apart from the difficulty in obtaining new credit or loans, dismissed debtors may also find it more challenging to rent a home, as landlords often check potential tenants' credit history. In some cases, dismissed bankruptcy may even affect employment opportunities, especially in fields where financial integrity is crucial. Bankruptcy dismissal means that the debtor is back to square one regarding their debt situation. If the debtor had a plan in place to manage their debts, such as a Chapter 13 repayment plan, the dismissal would render that plan null. Therefore, the debtor would need to devise a new strategy for paying off their debts. If the debtor is unable to manage their debts independently, they may need to seek help from a credit counseling agency or consider other debt-relief options, such as debt settlement or consolidation. After a bankruptcy case has been dismissed, the debtor might consider re-filing for bankruptcy. However, the ability to do so depends on whether the dismissal was with or without prejudice. Dismissal without prejudice means the debtor can typically re-file immediately, but there may be exceptions depending on the circumstances. In contrast, if the dismissal was with prejudice due to reasons such as fraud, the court may impose a time restriction before the debtor can re-file. Re-filing for bankruptcy can provide another chance for debtors to get back on their feet financially, offering another opportunity to implement a repayment plan or eliminate some or all of their debts. On the flip side, another bankruptcy filing can further impact the debtor's credit report, prolonging the time it takes to improve their credit score. Moreover, it could potentially fail again if the debtor's financial situation or behavior doesn't change. Timing is a critical consideration when re-filing for bankruptcy. Rushing to re-file might lead to another dismissal if the underlying issues that led to the initial dismissal have not been resolved. Therefore, it's crucial to seek legal advice to identify and address these issues before re-filing. For example, if the dismissal was due to a failure to make plan payments, the debtor should ensure they have a realistic and manageable plan before re-filing. Debt consolidation involves combining all your debts into a single loan with a lower interest rate. This makes managing debt easier as it requires only one monthly payment. Debt consolidation can also potentially lower the overall interest paid on the debt. Debt settlement is an approach where the debtor or a representative negotiates with creditors to reduce the total amount of debt owed. While this could provide substantial relief, it may also have severe implications on the debtor's credit score. Credit counseling is another option, particularly for those struggling to manage their debt independently. Reputable credit counseling agencies can provide advice on managing debt and personal finance, helping individuals create a personalized plan to solve their financial problems. Effective financial planning is critical after bankruptcy dismissal. It involves creating a realistic budget, setting financial goals, and planning for emergencies. Regular financial planning can help avoid falling back into unmanageable debt, enabling individuals to take control of their financial future. Building and repairing credit is another crucial step post-dismissal. This involves paying all bills on time, keeping credit card balances low, and avoiding new debt. Over time, these actions can help improve the debtor's credit score, making it easier to qualify for credit or loans in the future. Finally, adopting healthy financial habits is key to long-term financial stability. These habits may include saving regularly, limiting unnecessary expenses, using credit responsibly, and seeking professional advice when necessary. The consequences of bankruptcy dismissal are far-reaching, impacting a debtor's immediate financial state and future prospects. Dismissals enable creditors to resume collection activities, adversely affect credit ratings, and impede future financial opportunities. A debtor can consider re-filing, yet the timing and strategy are crucial to avoid repeating the same mistakes. Alternatively, exploring options such as debt consolidation, settlement, or credit counseling may provide debt relief. Post-dismissal, individuals should prioritize effective financial planning, credit repair, and the adoption of healthy financial habits to regain control of their financial future and avoid a recurrence of unmanageable debt. If you're facing the challenges of bankruptcy dismissal, consider seeking the assistance of a qualified financial advisor. They can provide valuable guidance to help you navigate your unique financial situation, develop effective debt management strategies, and guide you toward a healthier financial future.Overview of Bankruptcy and Bankruptcy Dismissal

Immediate Consequences of Bankruptcy Dismissal

Comparison Between Dismissal and Discharge

Impact on Debtors Immediately After Dismissal

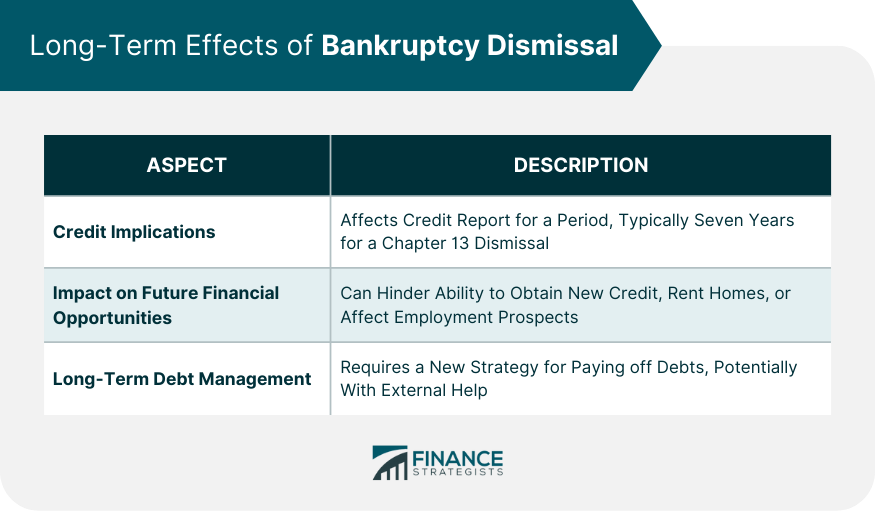

Long-Term Effects of Bankruptcy Dismissal

Credit Implications

Impact on Future Financial Opportunities

Long-Term Debt Management

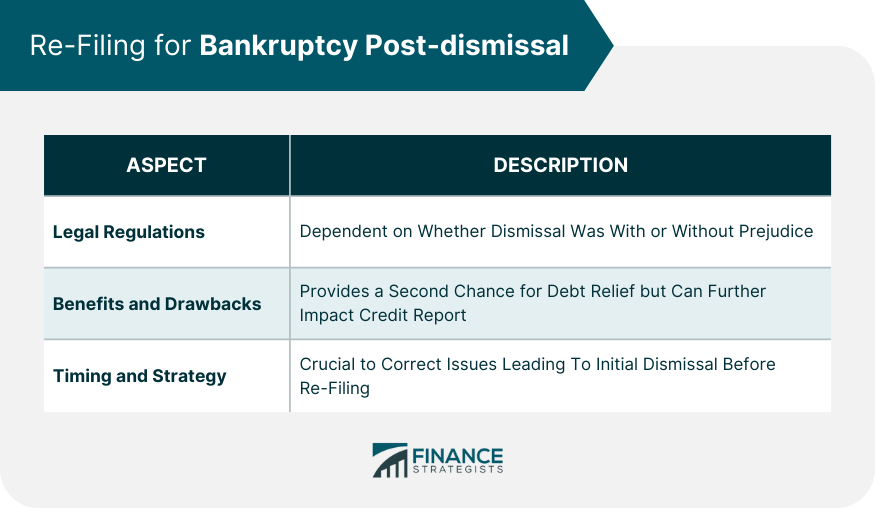

Re-Filing for Bankruptcy Post-dismissal

Legal Regulations Surrounding Re-Filing

Benefits and Drawbacks

Timing and Strategy for Re-Filing

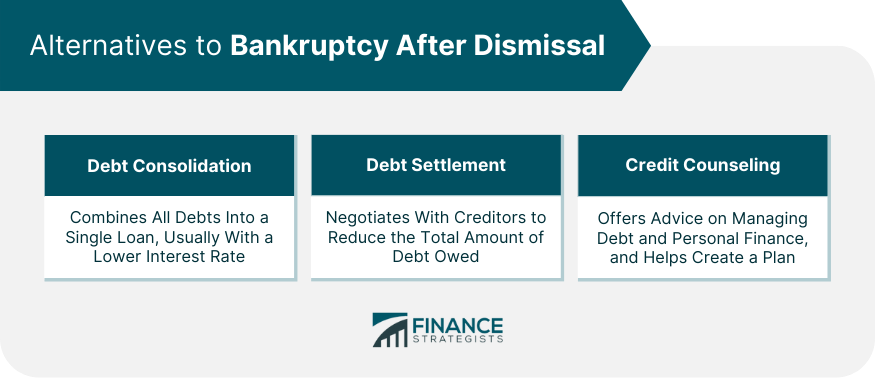

Alternatives to Bankruptcy After Dismissal

Debt Consolidation

Debt Settlement

Credit Counseling

Moving Forward Financially After Bankruptcy Dismissal

Financial Planning

Building and Repairing Credit

Incorporating Healthy Financial Habits

Bottom Line

What Happens After Bankruptcy Dismissal? FAQs

After a bankruptcy dismissal, the automatic stay is lifted, allowing creditors to resume collection activities, including foreclosures, repossessions, wage garnishments, and lawsuits.

A bankruptcy dismissal remains on your credit report for a certain period, usually seven years for a Chapter 13 dismissal, making obtaining new credit or loans more challenging.

Yes, you can re-file for bankruptcy after a dismissal. However, whether you can do so immediately or after a certain period depends on whether the dismissal was with or without prejudice.

Alternatives to bankruptcy after a dismissal include debt consolidation, debt settlement, and credit counseling.

Post dismissal, it's important to engage in financial planning, build and repair credit, and incorporate healthy financial habits. Consulting a financial advisor can be very beneficial in this process.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.