A financial plan is a comprehensive document that charts a business's monetary objectives and the strategies to achieve them. It encapsulates everything from budgeting and forecasting to investments and resource allocation. For small businesses, a solid financial plan provides direction, helping them navigate economic challenges, capitalize on opportunities, and ensure sustainable growth. The strength of a financial plan lies in its ability to offer a clear roadmap for businesses. Especially for small businesses that may not have a vast reserve of resources, prioritizing financial goals and understanding where every dollar goes can be the difference between growth and stagnation. It lends clarity, ensures informed decision-making, and sets the stage for profitability and success. Financial planning is the backbone of any successful business endeavor. It serves as a compass, guiding businesses toward profitability, stability, and growth. With proper financial planning, businesses can anticipate potential cash shortfalls, make informed investment decisions, and ensure they have the capital needed to seize new opportunities. For small businesses, in particular, tight financial planning can mean the difference between thriving and shuttering. Given the limited resources, it's vital to maximize every dollar and anticipate financial challenges. Through diligent planning, small businesses can position themselves competitively, adapt to market changes, and drive consistent growth. Every financial plan comprises several core components that, together, provide a holistic view of a business's financial health and direction. These include setting clear objectives, estimating costs, preparing financial statements, and considering sources of financing. Each component plays a pivotal role in ensuring a thorough and actionable financial strategy. For small businesses, these components often need a more granular approach. Given the scale of operations, even minor financial missteps can have significant repercussions. As such, it's essential to tailor each component, ensuring they address specific challenges and opportunities that small businesses face, from initial startup costs to revenue forecasting and budgetary constraints. Every business venture starts with a vision. Translating this vision into actionable financial goals is the essence of effective planning. Short-term goals could range from securing initial funding and achieving a set monthly revenue to covering startup costs. These targets, usually spanning a year or less, set the immediate direction for the business. On the other hand, long-term financial goals delve into the broader horizon. They might encompass aspirations like expanding to new locations, diversifying product lines, or achieving a specific market share within a decade. By segmenting goals into short-term and long-term, businesses can craft a step-by-step strategy, making the larger vision more attainable and manageable. Profitability and cash flow, while closely linked, are distinct concepts in the financial realm. Profitability pertains to the ability of a business to generate a surplus after deducting all expenses. It's a metric of success and indicates the viability of a business model. Simply put, it answers whether a business is making more than it spends. In contrast, cash flow represents the inflow and outflow of cash within a business. A company might be profitable on paper yet struggle with cash flow if, for instance, clients delay payments or unexpected expenses arise. For small businesses, maintaining positive cash flow is paramount. It ensures that they can cover operational costs, pay employees, and reinvest in growth, even if they're awaiting payments or navigating financial hiccups. When embarking on a new business venture, understanding costs is paramount. Fixed costs remain consistent regardless of production levels. They include expenses like rent, salaries, and insurance. These are predictable outlays that don't fluctuate with business performance. Variable costs, conversely, change in direct proportion to production or business activity. Think of costs associated with materials for manufacturing or commission for sales. For a startup, delineating between fixed and variable costs aids in crafting a more dynamic budget, allowing for adaptability as the business scales and evolves. Startups often grapple with numerous upfront costs. From purchasing equipment and setting up a workspace to initial marketing campaigns, these one-time expenditures lay the foundation for business operations. They differ from ongoing expenses like utility bills, raw materials, or employee wages that recur monthly or annually. For a small business owner, distinguishing between these costs is critical. One-time expenditures often demand a larger chunk of initial capital, while ongoing expenses shape the monthly and annual budget. By categorizing them separately, businesses can strategize funding needs more effectively, ensuring they're equipped to meet both immediate and recurrent financial obligations. This is often the most straightforward way to fund a startup. Entrepreneurs tap into their personal savings accounts to jumpstart their business. While this method has the benefit of not incurring debt or diluting company ownership, it intertwines the individual's personal financial security with the business's fate. The entrepreneur must be prepared for potential losses, and there's the evident psychological strain of putting one's hard-earned money on the line. Loans can be sourced from various institutions, from traditional banks to credit unions. They offer a substantial sum of money that can be paid back over time, usually with interest. The main advantage of taking a loan is that the entrepreneur retains full ownership and control of the business. However, there's the obligation of monthly repayments, which can strain a business's cash flow, especially in its early days. Additionally, securing a loan often requires collateral and a sound credit history. Investors, including angel investors and venture capitalists, offer capital in exchange for equity or a stake in the company. Angel investors are typically high-net-worth individuals who provide funding in the initial stages, while venture capitalists come in when there's proven business potential, often injecting larger sums. The advantage is substantial funding without the immediate pressure of repayments. However, in exchange for their investment, they often seek a say in business decisions, which might mean compromising on some aspects of the original business vision. Grants are essentially 'free money' often provided by government programs, non-profit organizations, or corporations to promote innovation and support businesses in specific sectors. The primary advantage of grants is that they don't need to be repaid, nor do they dilute company ownership. However, they can be highly competitive and might come with stipulations on how the funds should be used. Moreover, the application process can be lengthy and requires showcasing the business's potential or alignment with the specific goals or missions of the granting institution. An Income Statement, often termed as the Profit & Loss statement, showcases a business's financial performance over a specific time frame. It details revenues, expenses, and ultimately, profits or losses. By analyzing this statement, business owners can pinpoint revenue drivers, identify exorbitant costs, and understand the net result of their operations. For small businesses, this document is instrumental in making informed decisions. For instance, if a certain product line is consistently unprofitable, it might be prudent to discontinue it. Conversely, if another segment is thriving, it might warrant further investment. The Income Statement, thus, serves as a financial mirror, reflecting the outcomes of business strategies and decisions. The Balance Sheet offers a snapshot of a company's assets, liabilities, and equity at a specific point in time. Assets include everything the business owns, from physical items like equipment to intangible assets like patents. Liabilities, on the other hand, encompass what the company owes, be it bank loans or unpaid bills. Equity represents the owner's stake in the business, calculated as assets minus liabilities. This statement is crucial for small businesses as it offers insights into their financial health. A robust asset base, minimal liabilities, and growing equity signify a thriving enterprise. In contrast, mounting liabilities or dwindling assets could be red flags, signaling the need for intervention and strategy recalibration. While the Income Statement reveals profitability, the Cash Flow Statement tracks the actual movement of money. It categorizes cash flows into operating (day-to-day business), investing (buying/selling assets), and financing (loans or equity transactions) activities. This statement unveils the liquidity of a business, indicating whether it has sufficient cash to meet immediate obligations. For small businesses, maintaining positive cash flow is often more vital than showcasing profitability. After all, a business might be profitable on paper yet struggle if clients delay payments or unforeseen expenses emerge. By regularly reviewing the Cash Flow Statement, small business owners can anticipate cash crunches and strategize accordingly, ensuring seamless operations irrespective of revenue cycles. Budgeting is the financial blueprint for any business, detailing anticipated revenues and expenses for a forthcoming period. It's a proactive approach, enabling businesses to allocate resources efficiently, plan for investments, and prepare for potential financial challenges. For small businesses, a meticulous budget is often the linchpin of stability, ensuring they operate within their means and avoid financial pitfalls. Having a well-defined budget also fosters discipline. It curtails frivolous spending, emphasizes cost-efficiency, and sets clear financial boundaries. For small businesses, where every dollar counts, a stringent budget is the gateway to financial prudence, ensuring that funds are utilized judiciously, fostering growth, and minimizing wastage. When businesses buy supplies in large quantities, they often benefit from discounts due to economies of scale. This can significantly reduce per-unit costs. However, while bulk purchasing leads to immediate savings, businesses must ensure they have adequate storage and that the products won't expire or become obsolete before they're used. Regularly reviewing and renegotiating contracts with suppliers or service providers can lead to better terms and lower costs. This might involve exploring volume discounts, longer payment terms, or even bartering services. Building strong relationships with vendors often paves the way for such negotiations. Simple changes, like switching to LED lighting or investing in energy-efficient appliances, can lead to long-term savings in utility bills. Moreover, energy conservation not only reduces costs but also minimizes the environmental footprint, which can enhance the business's reputation. Modern software and technology can streamline business processes. Automation tools can handle repetitive tasks, reducing labor costs. Meanwhile, data analytics tools can provide insights into customer preferences and behavior, ensuring that marketing budgets are used effectively and target the right audience. Regularly reviewing and refining business processes can eliminate redundancies and improve efficiency. This might mean merging roles, cutting down on unnecessary meetings, or simplifying supply chains. A leaner operation often translates to reduced expenses. Instead of maintaining an in-house team for every function, businesses can outsource tasks that aren't central to their operations. For instance, functions like accounting, IT support, or digital marketing can be outsourced to specialized agencies, often leading to cost savings and access to expert skills. Encouraging employees to adopt a cost-conscious mindset can lead to collective savings. This can be fostered through incentives, regular training, or even simple practices like recycling and reusing office supplies. When everyone in the organization is attuned to the importance of cost savings, the cumulative effect can be substantial. Historical sales data is a foundational element in any forecasting effort. By reviewing previous sales figures, businesses can identify patterns, understand seasonal fluctuations, and recognize the effects of past initiatives. This information offers a baseline upon which to build future projections, accounting for known recurring variables in the business cycle. Understanding the larger market dynamics is crucial for accurate forecasting. This involves tracking industry trends, monitoring shifts in consumer behavior, and being aware of potential market disruptions. For instance, a sudden technological advancement can change consumer preferences or regulatory changes might impact an industry. For small businesses, localized insights can be especially impactful. Observing local competitors, understanding regional consumer preferences, or noting shifts in the local economy can offer precise data points. These granular details, when integrated into a larger forecasting model, can enhance prediction accuracy. Direct feedback from customers is an invaluable source of insights. Surveys, focus groups, or even informal chats can reveal customer sentiments, preferences, and potential future purchasing behavior. For instance, if a majority of loyal customers express interest in a new product or service, it can be indicative of future sales potential. This technique involves analyzing a series of data points (like monthly sales) by creating averages from different subsets of the full data set. For yearly forecasting, a 12-month moving average can be used to smooth out short-term fluctuations and highlight longer-term trends or cycles. Regression analysis is a statistical tool used to identify relationships between variables. In sales forecasting, it can help understand how different factors (like marketing spend, seasonal variations, or competitor actions) relate to sales figures. Once these relationships are understood, businesses can predict future sales based on planned actions or expected external events. The cash cycle encompasses the time it takes for a business to convert resource investments, often in the form of inventory, back into cash. This involves the processes of purchasing inventory, selling it, and subsequently collecting payment. A shorter cycle implies quicker cash turnarounds, which are vital for liquidity. For small businesses, a firm grasp of the cash cycle can aid in managing cash flow more effectively. By identifying bottlenecks or delays, businesses can strategize to expedite processes. This might involve renegotiating payment terms with suppliers, offering discounts for prompt customer payments, or optimizing inventory levels to prevent overstocking. Ultimately, understanding and optimizing the cash cycle ensures that a business remains liquid and agile. Seasonality affects many businesses, from the ice cream vendor witnessing summer surges to the retailer bracing for holiday shopping frenzies. By analyzing historical data and market trends, businesses can prepare for these cyclical shifts, ensuring they stock up, staff appropriately, and market effectively. Small businesses, often operating on tighter margins, need to be especially vigilant. Beyond seasonality, they must also brace for unexpected changes – a local construction project obstructing store access, a sudden competitor emergence, or unforeseen regulatory changes. Building a financial buffer, diversifying product or service lines, and maintaining flexible operational strategies can equip small businesses to weather these unforeseen challenges with resilience. When businesses seek external funding, they often grapple with the debt vs. equity conundrum. Debt financing involves borrowing money, typically via loans. While it doesn't dilute ownership, it necessitates regular interest payments, potentially impacting cash flow. Equity financing, on the other hand, entails selling a stake in the business to investors. It might not demand regular repayments, but it dilutes ownership and might influence business decisions. Small businesses must weigh these options carefully. While loans offer a structured repayment plan and retained control, they might strain finances if the business hits a rough patch. Equity financing, although relinquishing some control, might bring aboard strategic partners, offering expertise and networks in addition to funds. The optimal choice hinges on the business's financial health, growth aspirations, and the founder's comfort with sharing control. A staple in the lending arena, term loans offer businesses a fixed amount of capital that is paid back over a specified period with interest. They're often used for significant one-time expenses, such as purchasing machinery, real estate, or even business expansion. With predictable monthly payments, businesses can plan their budgets accordingly. However, they might require collateral and a robust credit history for approval. Unlike term loans that provide funds in a lump sum, a line of credit grants businesses access to a pool of funds up to a certain limit. Businesses can draw from this line as needed, only paying interest on the amount they use. This makes it a versatile tool, especially for managing cash flow fluctuations or unexpected expenses. It serves as a financial safety net, ready for use whenever required. As the name suggests, microloans are smaller loans designed to cater to businesses that might not need substantial amounts of capital. They're particularly beneficial for startups, businesses with limited credit histories, or those in need of a quick, small financial boost. Since they are of a smaller denomination, the approval process might be more lenient than traditional loans. A contemporary twist to the traditional lending model, peer-to-peer (P2P) platforms connect borrowers directly with individual lenders or investor groups. This direct model often translates to quicker approvals and competitive interest rates as the overheads of traditional banking structures are removed. With technology at its core, P2P lending can offer a more user-friendly, streamlined process. However, creditworthiness still plays a pivotal role in determining interest rates and loan amounts. In an increasingly digital age, crowdfunding platforms like Kickstarter or Indiegogo have emerged as viable financing avenues. These platforms enable businesses to raise small amounts from a large number of people, often in exchange for product discounts, early access, or other perks. This not only secures funds but also validates the business idea and fosters a community of supporters. Other alternatives include invoice financing, where businesses get an advance on pending invoices, or merchant cash advances tailored for businesses with significant credit card sales. Each financing mode offers unique advantages and constraints. Small businesses must meticulously evaluate their financial landscape, growth trajectories, and risk appetite to harness the most suitable option. Navigating the maze of taxation can be daunting, especially for small businesses. Yet, understanding and fulfilling tax obligations is crucial. Depending on the business structure—whether sole proprietorship, partnership, LLC, or corporation—different tax rules apply. For instance, while corporations are taxed on their earnings, sole proprietors report business income and expenses on their personal tax returns. In addition to income taxes, small businesses may also be responsible for employment taxes if they have employees. This covers Social Security, Medicare, federal unemployment, and sometimes state-specific taxes. There might also be sales taxes, property taxes, or special state-specific levies to consider. Consistently maintaining accurate financial records, being aware of filing deadlines, and setting aside funds for tax obligations are essential practices to avoid penalties and ensure compliance. Tax planning is the strategic approach to minimizing tax liability through the best use of available allowances, deductions, exclusions, and breaks. For small businesses, effective tax planning can lead to significant savings. This might involve strategies like deferring income to a later tax year, choosing the optimal time to purchase equipment, or taking advantage of specific credits available to businesses in certain sectors or regions. Several potential deductions can reduce taxable income for small businesses. These include expenses like rent, utilities, business travel, employee wages, and even certain meals. By keeping abreast of tax law changes and actively seeking out eligible deductions, small businesses can optimize their financial landscape, ensuring they're not paying more in taxes than necessary. While it's feasible for small business owners to manage their taxes, the intricate nuances of tax laws make it beneficial to consult professionals. An experienced accountant or tax consultant can not only ensure compliance but can proactively recommend strategies to reduce tax liability. They can guide businesses on issues like whether to classify someone as an employee or a contractor, how to structure the business for optimal taxation, or when to make certain capital investments. Beyond just annual tax filing, these professionals offer year-round counsel, helping businesses maintain clean financial records, stay updated on tax law changes, and plan for future financial moves. The investment in professional advice often pays dividends, saving businesses from costly mistakes, penalties, or missed financial opportunities. Like any strategic blueprint, a financial plan isn't static. It serves as a guiding framework but should be flexible enough to adapt to evolving business realities. Setting regular checkpoints—quarterly, half-yearly, or annually—can help businesses assess whether they're on track to meet their financial objectives. Milestones, such as reaching a specific sales target, launching a new product, or expanding into a new market, offer tangible markers of progress. Celebrating these victories can bolster morale, while any shortfalls can serve as lessons, prompting strategy tweaks. F or small businesses, where agility is an asset, regularly revisiting the financial plan ensures that the business remains aligned with its overarching financial goals while being responsive to the dynamic marketplace. Financial ratios offer a distilled snapshot of a business's health. Ratios like the current ratio (current assets divided by current liabilities) can shed light on liquidity, indicating whether a business can meet short-term obligations. The debt-to-equity ratio, contrasting borrowed funds with owner's equity, offers insights into the business's leverage and potential financial risk. Profit margin, depicting profitability relative to sales, can highlight operational efficiency. By consistently monitoring these and other pertinent ratios, small businesses can glean actionable insights, understanding their financial strengths and areas needing attention. In a realm where early intervention can stave off major financial setbacks, these ratios serve as vital diagnostic tools, guiding informed decision-making. In the ever-evolving world of business, flexibility is paramount. If financial reviews indicate that certain strategies aren't yielding anticipated results, it might be time to pivot. This could involve tweaking product offerings, revising pricing strategies, targeting a different customer segment, or even overhauling the business model. For small businesses, the ability to pivot can be a lifeline. It allows them to respond swiftly to market changes, customer feedback, or internal challenges. A robust financial plan, while offering direction, should also be pliable, accommodating shifts in strategy based on real-world performance. After all, in the business arena, adaptability often spells the difference between stagnation and growth. Financial foresight is integral for the stability and growth of small businesses. Effective revenue and cash flow forecasting, anchored by historical sales data and enhanced by market research, local trends, and customer feedback, ensures businesses are prepared for future demands. With the unpredictability of the business environment, understanding the cash cycle and preparing for unforeseen challenges is essential. As businesses contemplate external financing, the decision between debt and equity and the myriad of loan types, should be made judiciously, keeping in mind the business's health, growth aspirations, and risk appetite. Furthermore, diligent tax planning, with professional guidance, can lead to significant financial benefits. Regular reviews using financial ratios allow businesses to gauge their performance, adapt strategies, and pivot when necessary. Ultimately, the agility to adapt, guided by a well-structured financial plan, is pivotal for businesses to thrive in a dynamic marketplace.Financial Plan Overview

Understanding the Basics of Financial Planning for Small Businesses

Role of Financial Planning in Business Success

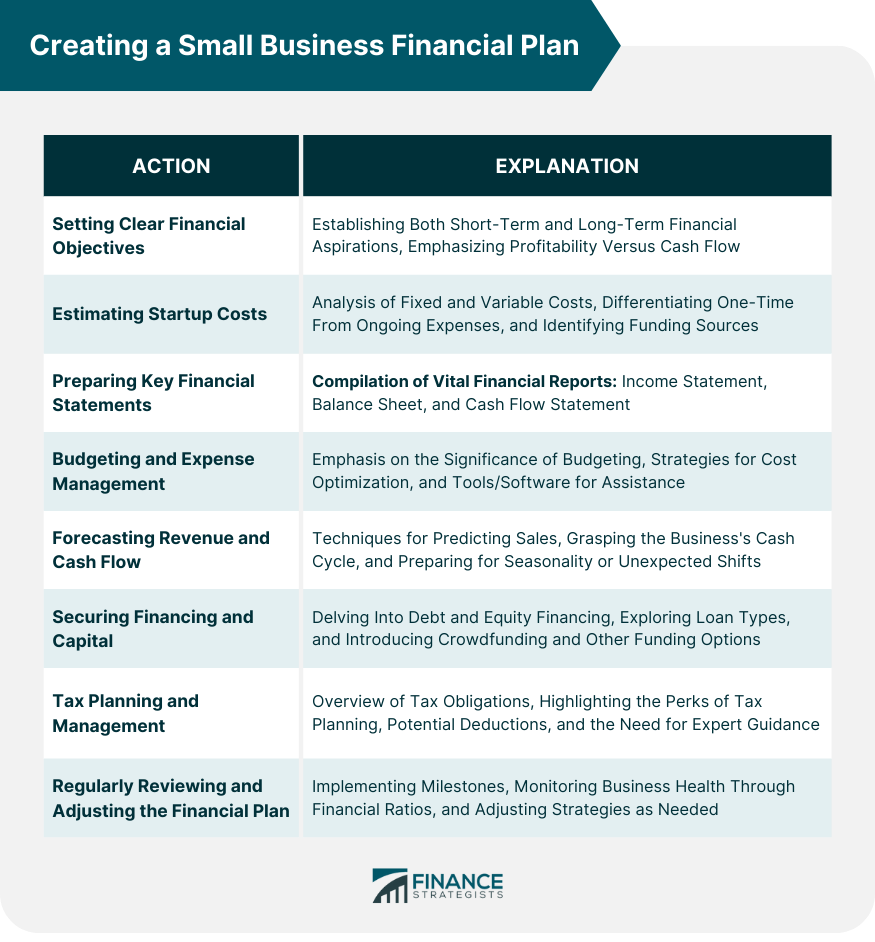

Core Components of a Financial Plan for Small Businesses

Setting Clear Small Business Financial Objectives

Identifying Business's Short-Term and Long-Term Financial Goals

Understanding the Difference Between Profitability and Cash Flow

Estimating Small Business Startup Costs (for New Businesses)

Fixed vs Variable Costs

One-Time Expenditures vs Ongoing Expenses

Funding Sources for Small Businesses

Personal Savings

Loans

Investors

Grants

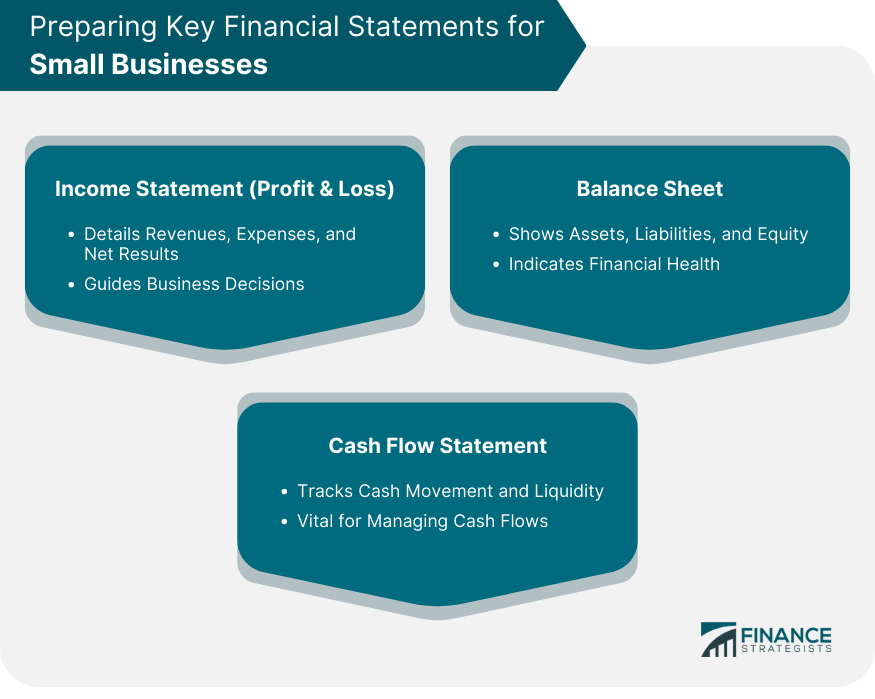

Preparing Key Financial Statements for Small Businesses

Income Statement (Profit & Loss)

Balance Sheet

Cash Flow Statement

Small Business Budgeting and Expense Management

Importance of Budgeting for a Small Business

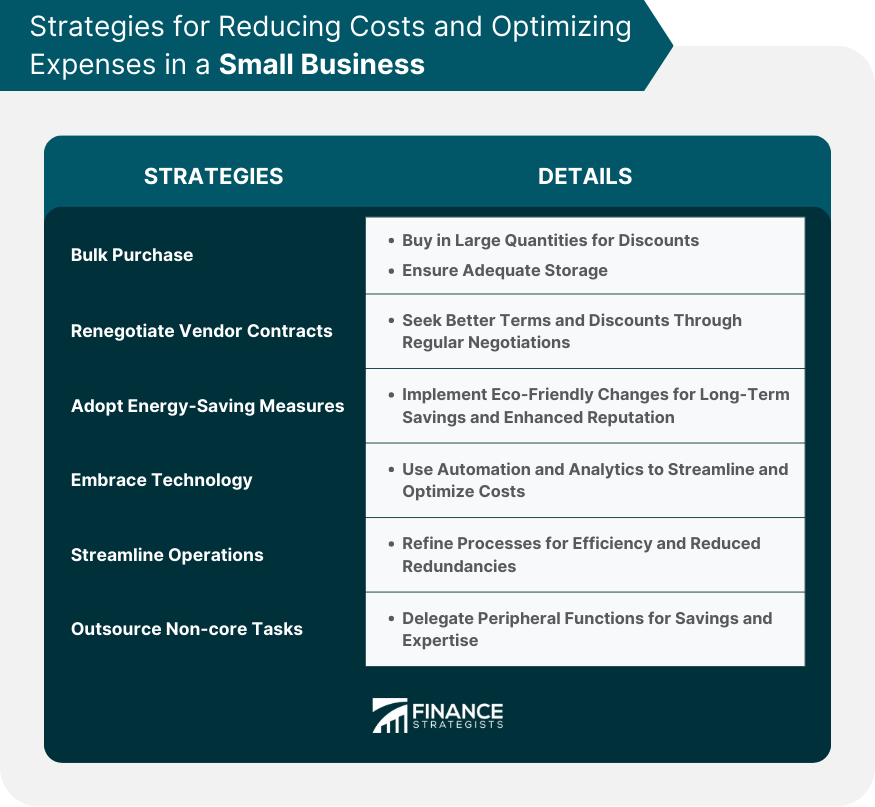

Strategies for Reducing Costs and Optimizing Expenses

Bulk Purchasing

Renegotiating Vendor Contracts

Adopting Energy-Saving Measures

Embracing Technology

Streamlining Operations

Outsourcing Non-core Tasks

Cultivating a Culture of Frugality

Forecasting Small Business Revenue and Cash Flow

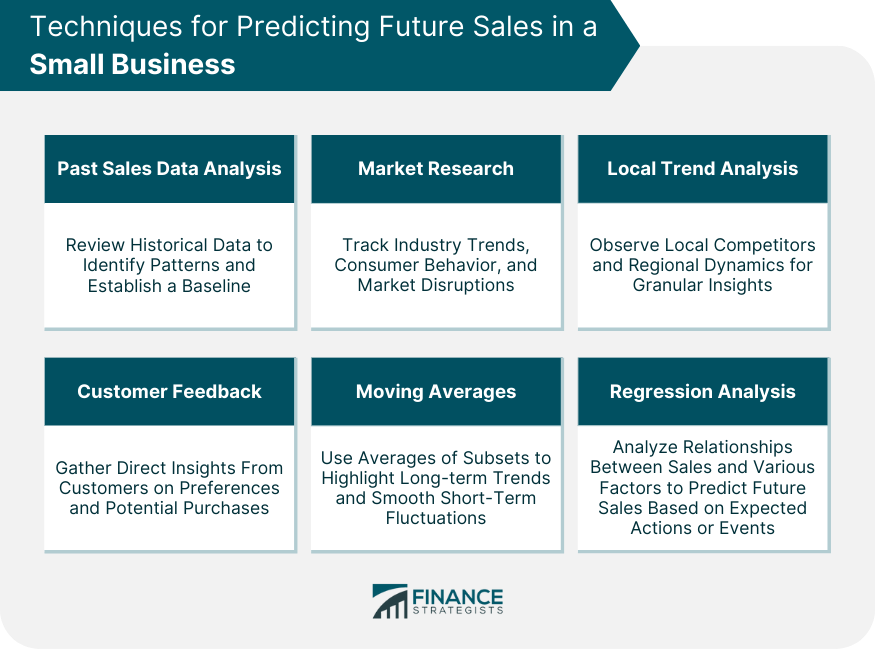

Techniques for Predicting Future Sales in a Small Business

Past Sales Data Analysis

Market Research

Local Trend Analysis

Customer Feedback

Moving Averages

Regression Analysis

Understanding the Cash Cycle of Business

Preparing for Seasonality and Unexpected Changes

Securing Small Business Financing and Capital

Role of Debt and Equity Financing

Choosing Between Different Types of Loans

Term Loans

Lines of Credit

Microloans

Peer-To-Peer Lending

Crowdfunding and Alternative Financing Options

Small Business Tax Planning and Management

Basic Tax Obligations for Small Businesses

Advantages of Tax Planning and Potential Deductions

Importance of Hiring a Tax Professional or Accountant

Regularly Reviewing and Adjusting the Small Business Financial Plan

Setting Checkpoints and Milestones

Using Financial Ratios to Monitor Business Health

Pivoting Strategies Based on Financial Performance

Bottom Line

Creating a Small Business Financial Plan FAQs

A financial plan offers a structured roadmap, guiding businesses in making informed decisions, ensuring growth, and navigating financial challenges.

Forecasting provides insights into expected income, aiding in budget allocation, while understanding cash cycles ensures effective liquidity management.

Core components include setting objectives, estimating startup costs, preparing financial statements, budgeting, forecasting, securing financing, and tax management.

Tax planning ensures compliance, optimizes tax liabilities through available deductions, and helps businesses save money and avoid penalties.

Regular reviews, ideally quarterly or half-yearly, ensure alignment with business goals and allow for strategy adjustments based on real-world performance.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.