Fee-only planning is a model where financial planners are compensated solely through the fees paid directly by their clients rather than through commissions or incentives from product sales or referrals. This approach ensures that the advice given is unbiased and squarely focused on the client's best interests. In fee-only structures, planners might charge hourly rates, a fixed fee for specific services, a percentage of assets under management, or a retainer fee for ongoing advisory. The primary advantage of this model is the elimination of potential conflicts of interest, as there's no inherent incentive to recommend one financial product over another unless it genuinely serves the client's needs. Additionally, clients enjoy a high level of transparency, understanding exactly what services they're receiving and their associated costs. Clients pay for the planner’s time, similar to how you might pay an attorney or consultant. This is a set fee for a specific service, like creating a financial plan. Typically a percentage of the total assets the planner manages for the client. An ongoing fee, often monthly or quarterly, for continuous financial advice. Clients appreciate upfront knowledge about what they're paying for. With fee-only, there are no hidden costs or undisclosed commissions, ensuring clarity in financial transactions. Without commission-driven incentives, the planner's advice remains unbiased, fostering trust. Clients can be assured that recommendations are made in their best interest, not driven by a hidden financial agenda. The fee-only model facilitates tailored advice, as planners are not restricted to peddling specific financial products. Their sole focus is understanding and meeting the client's unique financial needs. Some clients, especially those with limited assets or straightforward financial situations, might find the fee-only model cost-prohibitive. Alternatives like robo-advisors or fee-based planners might be more economical. The fee-only model, particularly if it involves a fixed or hourly fee, can seem daunting to some clients. They might hesitate, fearing high upfront charges, even if it might be cost-effective in the long run. Though rare, some fee-only planners might have limited access to specific financial products, potentially depriving clients of a more comprehensive array of options. Ensure the planner has reputable certifications, like Certified Financial Planner (CFP). Not all fee-only planners offer the same services, so it’s essential to find one that fits your needs. Each fee structure resonates differently with clients. Hourly rates are straightforward and ideal for one-off consultations. Fixed fees often apply to specific planning packages or tasks. Lastly, a percentage of assets under management is common for ongoing investment advice, with planners earning a proportion of the client's portfolio. While both involve fees, fee-based planning also permits commissions from product sales. This dual revenue stream can muddy the waters, potentially diluting the objectivity of advice given. Fee-based structures, due to their allowance for commissions, can sometimes lead to potential conflicts. A planner might be swayed by a higher commission on a specific product, even if it's not the optimal choice for the client. It's essential for clients to discern when a recommendation is driven by the planner's financial gain. Knowledge of fee structures empowers clients to ask the right questions and demand transparency. Seek planners with recognized certifications like CFP® (Certified Financial Planner). Such credentials signify adherence to rigorous standards and ethical practices. A planner with a fiduciary duty is legally obligated to act in the best interest. This commitment further ensures that the advice given is genuine and beneficial. Prospective clients should inquire about the planner's experience, approach to financial planning, fee structures, and any potential conflicts of interest. The clarity and depth of their answers can offer invaluable insights. Fee-only financial planning emerges as a paradigm centered on transparent, unbiased advice, with compensation derived exclusively from client fees, eliminating commissions and associated potential conflicts. The diverse fee structures - hourly, fixed, asset-under-management, and retainer - offer flexibility to clients while preserving the planner's objective stance. While the model's advantages, such as unparalleled transparency and custom-tailored guidance, are clear, it's also essential to recognize its limitations, like potential upfront costs that might deter certain clients. Differentiating fee-only from fee-based models is crucial, as the latter introduces commissions, occasionally muddying objective advice. When selecting a planner, credentials like the CFP® designation and a committed fiduciary duty stand paramount. Ultimately, the fee-only model prioritizes the client's financial well-being, setting a gold standard in financial planning by intertwining trust, clarity, and fiduciary responsibility.Fee-Only Financial Planning Overview

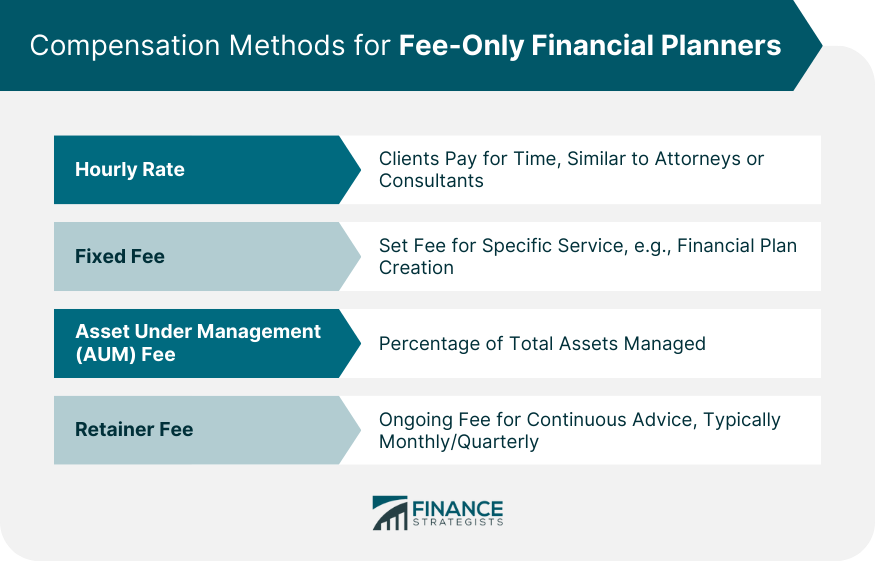

Compensation Methods for Fee-Only Financial Planners

Hourly Rate

Fixed Fee

Asset Under Management (AUM) Fee

Retainer Fee

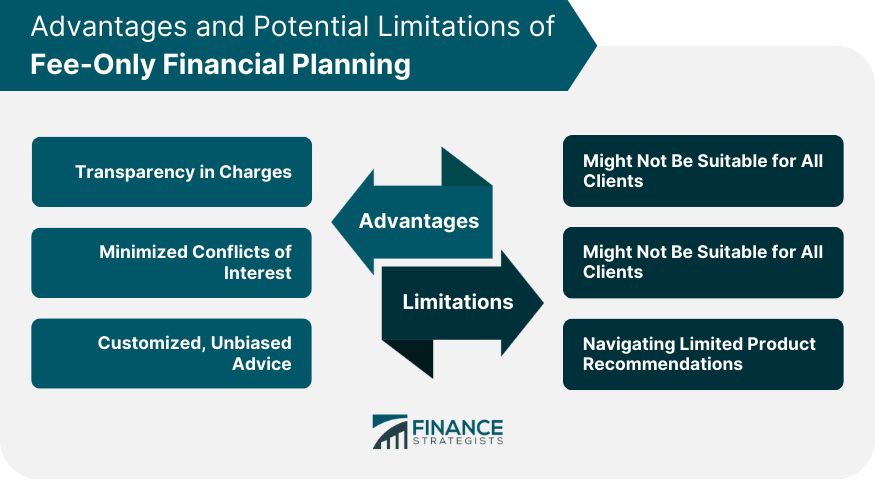

Advantages of Fee-Only Financial Planning

Transparency in Charges

Minimized Conflicts of Interest

Customized, Unbiased Advice

Potential Limitations of Fee-Only Financial Planning

Might Not Be Suitable for All Clients

Possible Perception of High Upfront Costs

Navigating Limited Product Recommendations

Selecting the Right Fee-Only Planner

Check Credentials

Understand Services Offered

Discuss Fee Structures

Fee-Only vs Fee-Based Financial Planning

Key Differences and Potential Confusion

Implications for Potential Conflicts of Interest

Understanding Commission-Driven Recommendations

How to Choose a Fee-Only Financial Planner

Credentials and Qualifications to Look For

Importance of Fiduciary Duty

Questions to Ask During Initial Consultations

Conclusion

Fee-Only Financial Planning FAQs

Fee-only financial planning is a compensation model where financial planners are paid solely by their clients and not from third-party commissions or incentives, ensuring transparency and unbiased advice.

While both models involve fees from clients, fee-based planning also permits planners to earn commissions from product sales, potentially leading to conflicts of interest. Fee-only financial planning strictly prohibits earning from commissions, ensuring unbiased advice.

Not necessarily. Although the upfront cost might appear higher, fee-only financial planning often proves cost-effective in the long run due to its transparency and absence of hidden charges.

Look for planners with recognized certifications like CFP® and those who uphold a fiduciary duty. This ensures they are legally obligated to act in your best interest.

Generally, yes. Fee-only financial planners aim to provide tailored advice without the constraints of pushing specific products. However, it's essential to ensure your planner has access to a wide array of financial products for a comprehensive overview.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.