The rate of return on an annuity is a crucial aspect to consider when evaluating the suitability of this retirement investment. Annuities offer different types of returns, depending on the specific product and its underlying investment options. Fixed annuities provide a guaranteed minimum interest rate, ensuring stability and predictability in returns. Variable annuities, on the other hand, offer returns that fluctuate based on the performance of chosen investment options, providing the potential for higher returns but also carrying greater market risk. The rate of return on an annuity is influenced by factors such as market conditions, investment performance, fees, and expenses. It is important to carefully assess the potential returns and associated risks before committing to an annuity, taking into account individual financial goals, risk tolerance, and time horizon. Calculating the rate of return on an annuity involves taking the annuity’s current value minus the contribution, then dividing it by the total contribution. Multiply the result by 100 to get a percentage value. The key variables involved in this calculation include the initial investment, the amount and timing of each payment, the amount and timing of each payout, and the number of years the annuity is held. Compounding plays a significant role in the rate of return on an annuity. The compounding of interest means that a low rate of return can generate substantial growth over time, especially for long-term investments like annuities. The rate of return on fixed annuities is often closely tied to prevailing market interest rates. When interest rates rise, the rate of return on new fixed annuity contracts also tends to increase. Inflation can erode the real value of the fixed payments received from an annuity, effectively reducing the rate of return. Inflation-indexed annuities, however, can provide protection against this risk. The growth of non-qualified annuity investments is tax-deferred, meaning investors won't owe taxes until they start receiving payments. This tax-deferred growth can enhance the effective rate of return. Many annuity contracts come with a variety of charges and fees, which can eat into the rate of return. These can include surrender charges, management fees for variable annuities, mortality and expense risk charges, and more. For variable annuities, the rate of return is tied to the performance of the investment options chosen. These can range from stock and bond funds to money market funds, and their performance can greatly impact the returns. One of the main advantages of fixed annuities is the guarantee of a certain rate of return and the safety of the principal, providing a level of security for investors. Annuities can provide a steady stream of income for life, making them a popular choice for retirement income planning. The growth of funds within an annuity is tax-deferred, meaning investors do not pay taxes on the earnings until they start receiving distributions. Variable annuities provide the potential for higher returns, depending on the performance of the underlying investments. However, this potential comes with greater risk. Like all investments, annuities come with risks. These include the risk of loss of principal for variable annuities, credit risk of the insurer for all annuities, inflation risk for fixed annuities, and more. Like fixed annuities, bonds provide regular interest payments. However, bonds are subject to credit and interest rate risk, while fixed annuities offer a guaranteed return and safety of principal (assuming the insurer remains solvent). Stocks offer the potential for higher returns than annuities but also come with a higher level of risk. Unlike annuities, they do not provide a guaranteed income stream. Mutual funds, like variable annuities, offer a range of investment options. However, the returns are not guaranteed, and there are usually management fees associated with mutual funds. Real estate can provide a good rate of return and tax benefits, but it also requires active management and comes with its own set of risks. It does not offer the predictable income stream that an annuity does. Choosing the right type of annuity can have a big impact on the rate of return. Factors to consider include risk tolerance, income needs, and investment horizon. Timing can play a role in the rate of return on annuities. For instance, buying an annuity when interest rates are high can lock in a higher return for fixed annuities. Keeping costs and fees to a minimum can help improve the rate of return. This may involve shopping around for the best annuity rates and terms and avoiding unnecessary features or riders. There may be other investment options that provide a higher rate of return than annuities, depending on an individual's risk tolerance and investment goals. While annuities offer tax-deferred growth, the distributions are taxed as ordinary income. This can be a disadvantage compared to other investments that receive more favorable tax treatment. Despite this, the benefit of tax deferral can be substantial, particularly for individuals in high tax brackets or those who anticipate being in a lower tax bracket in retirement. Premature withdrawals before age 59½ can result in a 10% penalty in addition to regular income taxes. Understanding the rate of return on annuities is vital for strategic financial planning. The rate can be fixed or variable, depending on the annuity type, and is influenced by several factors, including market interest rates, inflation, taxation, fees, and performance of underlying investments in the case of variable annuities. Knowing how to calculate this rate while factoring in compounding and cash flows is critical. Additionally, selecting the right annuity, optimal timing, minimizing costs, and considering alternatives can improve the rate of return. Despite being taxed as ordinary income, the tax-deferral benefit of annuities can be substantial, particularly for those in higher tax brackets. Balancing these elements effectively can optimize your annuity investment, helping align it with broader financial goals for a secure retirement. Remember, a comparison with other investment options helps clarify relative profitability, enabling informed decision-making.Rate of Return on Annuity Overview

Calculating Rate of Return on Annuity

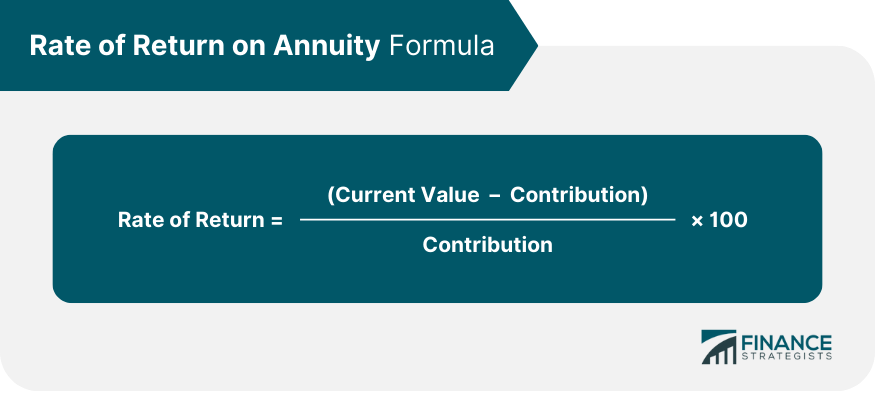

Methodology and Formula

Variables in the Calculation

Role of Compounding in Rate of Return

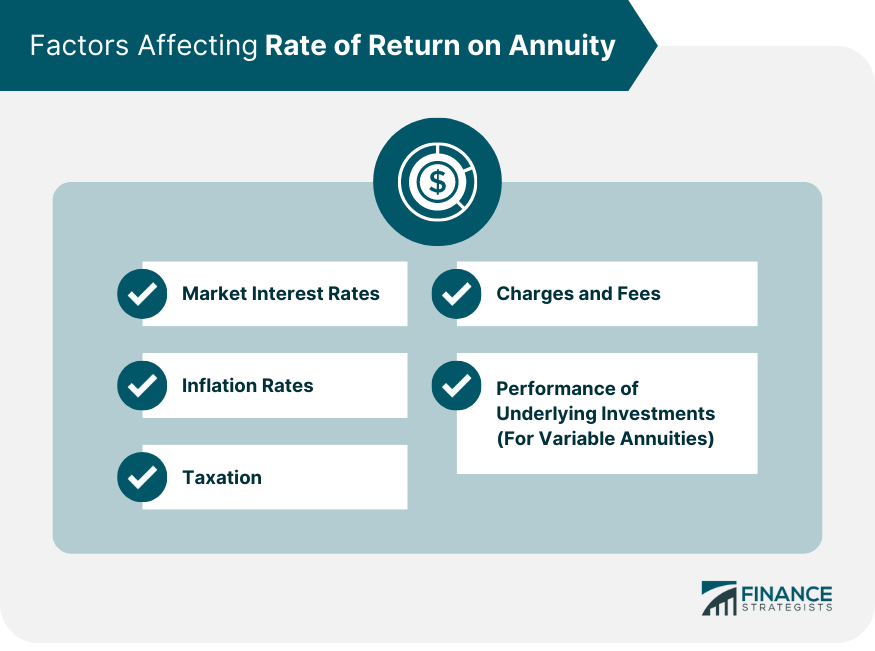

Factors Impacting Rate of Return on Annuity

Market Interest Rates

Inflation Rates

Taxation

Charges and Fees

Performance of Underlying Investments (for Variable Annuities)

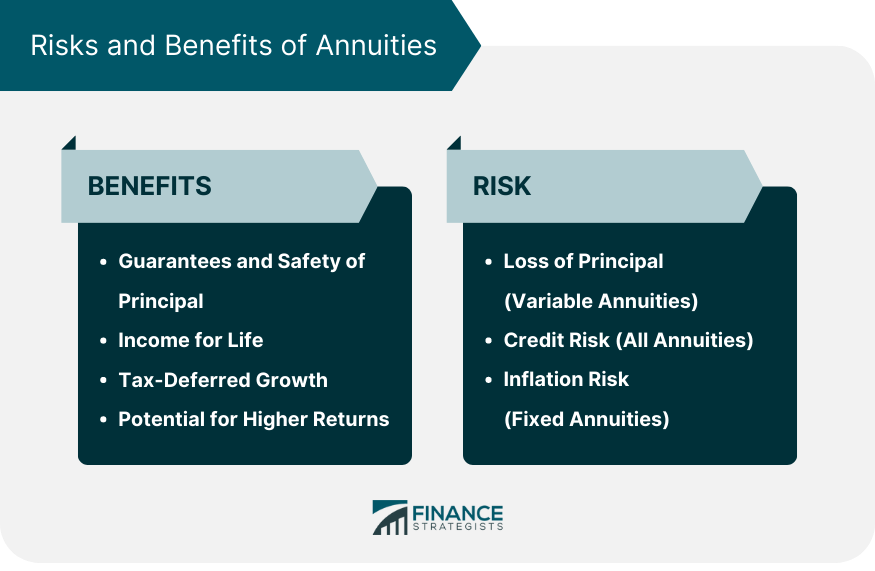

Risks and Benefits of Annuities

Guarantees and Safety of Principal

Income for Life

Tax-Deferred Growth

Potential for Higher Returns

Risks Associated With Annuities

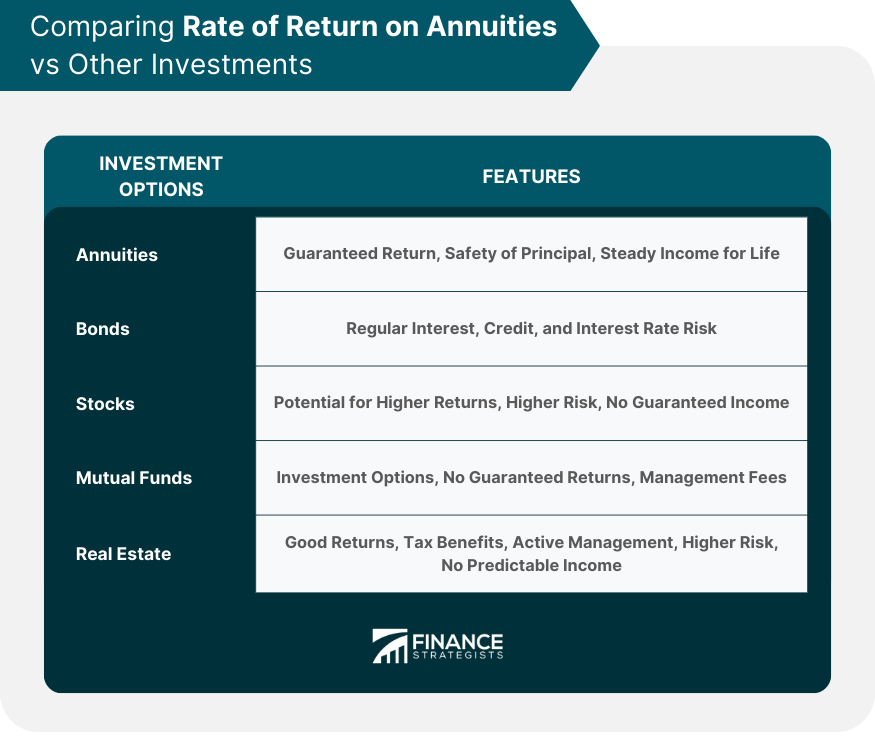

Comparing Rate of Return on Annuities vs Other Investments

Bonds

Stocks

Mutual Funds

Real Estate

How to Improve the Rate of Return on Annuities

Selecting the Right Type of Annuity

Timing of Investment

Reducing Costs and Fees

Considering Annuity Alternatives for Higher Returns

Impact of Tax on Rate of Return on Annuity

Annuity Taxation Basics

Tax Deferral Benefits

Tax Consequences of Withdrawals

Conclusion

Rate of Return on Annuity FAQs

The rate of return on an annuity is the gain or loss made on the annuity investment relative to the amount of money invested. It is calculated by summing up all the cash flows (including both the payments made into the annuity and the payouts received) and setting this sum equal to the initial investment multiplied by (1 + rate of return) to the power of the number of years. This equation can then be solved for the rate of return.

Market interest rates significantly influence the rate of return on fixed annuities. When interest rates rise, the rate of return on new fixed annuity contracts also tends to increase. However, variable annuities are less directly affected by market interest rates, as their rate of return depends on the performance of the underlying investments.

Several factors can impact the rate of return on an annuity, including market interest rates, inflation rates, taxation, the charges and fees associated with the annuity contract, and the performance of underlying investments for variable annuities.

Improving the rate of return on an annuity can be achieved by selecting the right type of annuity based on your risk tolerance, income needs, and investment horizon. Timing your investment to capitalize on high-interest rates, reducing costs and fees, and considering alternatives to annuities for higher returns can also help.

The growth of non-qualified annuity investments is tax-deferred, meaning investors won't owe taxes until they start receiving payments, which can enhance the effective rate of return. However, withdrawals are taxed as ordinary income, and premature withdrawals can incur additional penalties, which may reduce the overall rate of return on the annuity.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.