Variable annuitization is a retirement income strategy that converts a part of an individual's retirement fund into a stream of income. It differs from fixed annuitization, where the annuitant receives a fixed amount regularly. With variable annuitization, the amount received depends on the performance of chosen investments, typically mutual funds. The annuitant selects a group of investments, and the payout varies based on their returns. This strategy can provide inflation protection and potential for growth as the retirement fund is invested in the market. However, it also involves more risk, as the income can fluctuate with market conditions. Variable annuitization is often used by individuals who are willing to accept a certain level of risk to potentially increase their retirement income. During the accumulation phase, investors contribute to their variable annuity through periodic payments or a lump-sum investment. These contributions are invested in a selection of sub-accounts, which consist of various mutual funds or other investment vehicles. The investor can typically choose from a wide range of investment options, including stock and bond funds, as well as more conservative money market funds or fixed-income investments. Variable annuities offer tax-deferred growth, meaning that investment earnings are not subject to taxes until they are withdrawn. This allows investors to potentially accumulate more savings over time and defer taxes on their investment gains until they are in a lower tax bracket during retirement. Upon reaching the annuitization phase, the investor can elect to convert their accumulated savings into a series of periodic payments, either for a specified period or for their entire lifetime. The amount and frequency of these payments will depend on factors such as the value of the annuity, the investor's age, and the chosen payout option. Variable annuity payments can be made on a monthly, quarterly, semi-annual, or annual basis, depending on the investor's preference. Investors can choose from several payment options, including single-life annuities, which provide income for the life of the annuitant, or joint-life annuities, which continue payments for the life of both the annuitant and a designated survivor, typically a spouse. Variable annuities are associated with a variety of fees and expenses, including management fees for the underlying investment options, mortality and expense risk charges, and administrative fees. These costs can significantly impact the overall performance of the annuity and should be carefully considered when selecting a variable annuity product. Many variable annuities impose surrender charges if the investor withdraws funds from the annuity during the early years of the contract. These charges can be substantial and are designed to discourage early withdrawals, as they can impact the insurance company's ability to manage the annuity's investments effectively. Variable annuities often include a death benefit that guarantees a specified amount will be paid to the investor's beneficiaries upon their death. This amount can be the greater of the annuity's account value or a guaranteed minimum amount, providing a measure of protection for the investor's heirs. Guaranteed Minimum Income Benefit (GMIB): This is an optional feature that guarantees the annuitant a minimum level of income during the annuitization phase, regardless of the performance of the underlying investments. Guaranteed Lifetime Withdrawal Benefit (GLWB): allows annuitants to withdraw a specified percentage of their annuity account value each year for the rest of their lives without the risk of completely depleting their account. Assessing Client Needs and Risk Tolerance: Brokers should work closely with clients to assess their financial goals, retirement needs, and risk tolerance, ensuring that the selected annuity product aligns with the client's objectives and preferences. Comparing and Selecting Variable Annuity Providers: By thoroughly researching and comparing available options, brokers can help clients find the best possible annuity product for their individual needs. Educating Clients on Contract Terms and Potential Benefits: Insurance brokers should also educate clients on the specific terms of their variable annuity contracts, ensuring they understand the fees, expenses, and potential benefits. Monitoring and Managing Variable Annuity Investments: Brokers monitor and manage variable annuity investments, adjusting allocations as needed based on market conditions and client needs Variable annuities are subject to market and investment risk, meaning that the value of the annuity and the income it generates can fluctuate with changes in the performance of the underlying investments. Investors should carefully consider their risk tolerance and investment time horizon before selecting a variable annuity product. Variable annuities are also subject to interest rate risk, as the income generated during the annuitization phase may be impacted by changes in prevailing interest rates. If interest rates decline, the income generated by the annuity may be lower than anticipated, potentially affecting the annuitant's retirement income. Inflation risk is another concern for variable annuity investors, as the purchasing power of their annuity payments may erode over time due to rising prices. To mitigate this risk, some annuity products offer inflation-adjusted payment options, which can help preserve the annuitant's purchasing power during retirement. Longevity risk is the risk that an annuitant will outlive their assets and face financial hardship during their retirement years. Variable annuities can help address this risk by providing a guaranteed income stream for the life of the annuitant, reducing the likelihood that they will exhaust their savings. As previously mentioned, variable annuities offer tax-deferred growth, allowing investors to defer taxes on their investment gains until they are withdrawn. This can be particularly beneficial for investors in higher tax brackets, who may be subject to lower tax rates during retirement. Variable annuities can be classified as either qualified or non-qualified, depending on the source of the funds used to purchase the annuity. Qualified annuities are purchased with pre-tax dollars, such as funds from an IRA or 401(k) plan. Non-qualified annuities, on the other hand, are funded with after-tax dollars, such as savings from a taxable brokerage account. Withdrawals from variable annuities are subject to income tax, and if made before the age of 59 1/2, may also be subject to a 10% penalty. Annuity payments during the annuitization phase are also subject to income tax, with the amount of tax owed based on the annuitant's tax bracket at the time of withdrawal. Variable annuities can also have implications for estate and gift tax planning. Upon the annuitant's death, any remaining funds in the annuity are typically paid out to the designated beneficiaries. These payments may be subject to estate tax, depending on the total value of the annuity and the annuitant's overall estate. Fixed annuities are similar to variable annuities in that they provide a stream of income during the annuitization phase, but they differ in that the value of the annuity and the income generated are fixed and do not fluctuate with market conditions. This can provide a measure of stability for investors concerned about market volatility. Indexed annuities offer a hybrid investment approach, combining features of both fixed and variable annuities. These products provide a guaranteed minimum return, similar to a fixed annuity, but also offer the potential for additional earnings based on the performance of a specified index, such as the S&P 500. In addition to annuities, investors have a variety of other investment options for generating retirement income. These may include IRAs, 401(k) plans, real estate investments, and dividend-paying stocks, among others. Each of these options has its own unique features and benefits and should be evaluated in the context of the investor's individual financial situation and retirement goals. Insurance brokers who offer variable annuity products are subject to regulation by the SEC, which oversees the sale and marketing of securities products. Brokers must comply with strict disclosure requirements and other regulations designed to protect investors and ensure transparency in the sales process. The FINRA is a self-regulatory organization that oversees the securities industry and establishes guidelines for broker-dealers and their associated agents. Brokers who sell variable annuities must comply with FINRA's strict suitability standards, ensuring that the products they recommend are appropriate for the investor's individual needs and risk tolerance. In addition to federal regulation, insurance brokers who offer variable annuities are also subject to state-specific licensing requirements and oversight by state insurance departments. These departments are responsible for enforcing state insurance laws and regulations and ensuring that brokers comply with all applicable licensing requirements and professional standards. Variable annuitization is a retirement income strategy that converts a portion of a retirement fund into a stream of income, with payouts based on the performance of chosen investments. It offers potential growth and inflation protection but involves market and investment risks. During the accumulation phase, investors contribute and invest in sub-accounts with mutual funds or investment vehicles. Tax-deferred growth is a key feature, allowing savings to grow without immediate taxation. In the annuitization phase, accumulated savings can be converted into periodic payments based on the annuity value, age, and chosen payout. Variable annuity payments can be customized in terms of options and frequency. Variable annuities come with contract terms, fees, surrender charges, death benefits, and optional features like guaranteed minimum income benefits. Insurance brokers play a role in assessing client needs, comparing annuity providers, educating clients, and monitoring investments. Risks include market, interest rate, inflation, and longevity risks. Variable annuitization has tax implications, with tax-deferred growth and varying tax treatment of withdrawals and annuity payments. What Is Variable Annuitization?

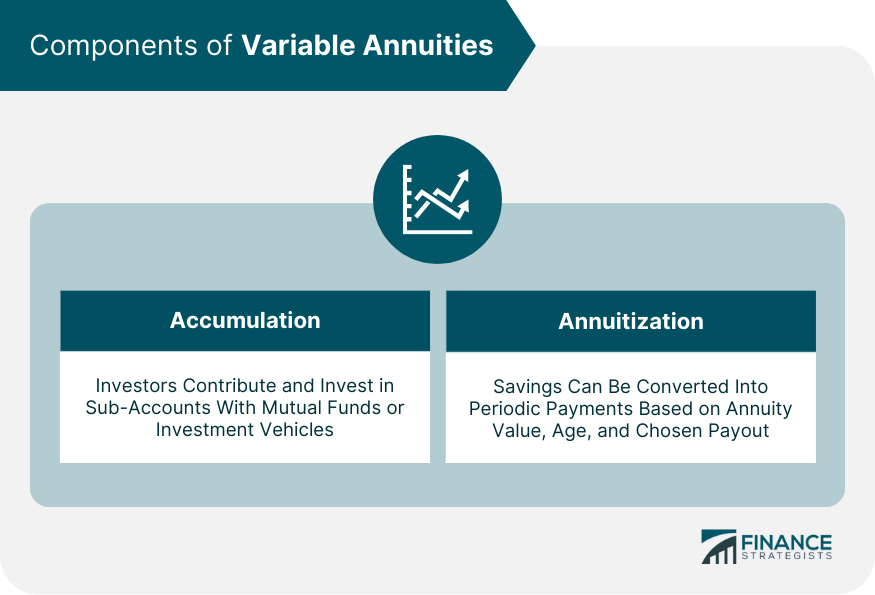

Components of Variable Annuities

Accumulation Phase

Contributions and Investment Options

Tax-Deferred Growth

Annuitization Phase

Transition From Accumulation to Annuitization

Payment Options and Frequency

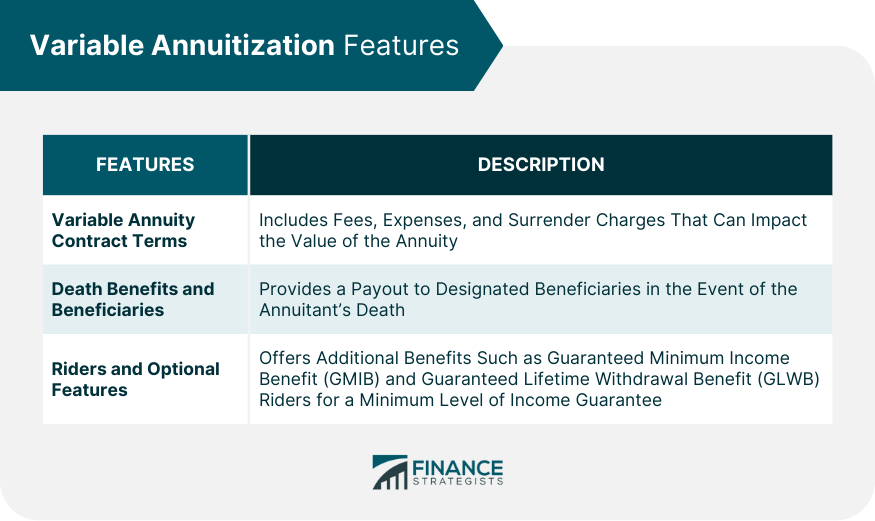

Variable Annuitization Features

Variable Annuity Contract Terms

Fees and Expenses

Surrender Charges

Death Benefits and Beneficiary Provisions

Riders and Optional Features

Insurance Broker's Role in Variable Annuitization

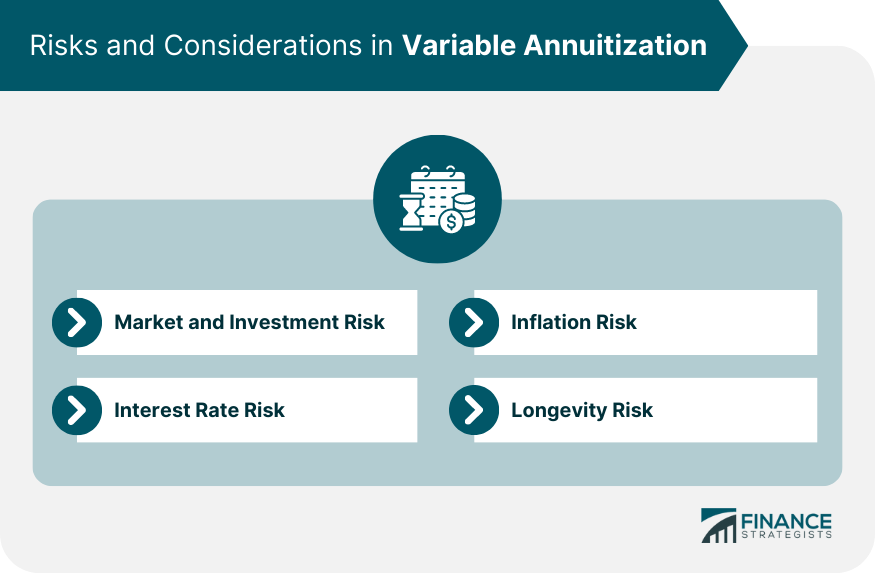

Risks and Considerations in Variable Annuitization

Market and Investment Risk

Interest Rate Risk

Inflation Risk

Longevity Risk

Tax Implications of Variable Annuitization

Tax-Deferred Growth

Qualified and Non-qualified Annuities

Tax Treatment of Withdrawals and Annuity Payments

Estate and Gift Tax Considerations

Alternatives to Variable Annuitization

Fixed Annuities

Indexed Annuities

Other Investment Options for Retirement Income

Regulatory Environment and Compliance for Insurance Brokers

Securities and Exchange Commission (SEC) Regulations

Financial Industry Regulatory Authority (FINRA) Guidelines

State Insurance Departments and Licensing Requirements

Bottom Line

Variable Annuitization FAQs

Variable annuitization is a financial strategy for retirement that offers a regular income stream derived from a portion of a person's retirement savings. Variable annuitization offers an income that varies based on the performance of selected investment assets, typically mutual funds. This strategy involves two phases: the accumulation phase, where individuals contribute to their annuity, and the annuitization phase, where the accumulated savings are converted into periodic payments.

The key components of variable annuities include the accumulation phase, where investors contribute to their annuity through periodic payments or lump-sum investments, and the annuitization phase, where they convert their accumulated savings into a series of periodic payments.

Variable annuities are subject to market and investment risk, interest rate risk, inflation risk, and longevity risk. Investors should carefully consider these risks, along with the fees and expenses associated with variable annuities, before investing in them.

Insurance brokers can play a critical role in helping investors understand and select appropriate variable annuity products. They can assist with assessing client needs and risk tolerance, comparing and selecting variable annuity providers, educating clients on contract terms and potential benefits, and monitoring and managing variable annuity investments.

Variable annuities offer several features, including optional riders, such as the guaranteed minimum income benefit (GMIB) and the guaranteed lifetime withdrawal benefit (GLWB), death benefits, and surrender charges.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.