Annuities are contractual financial products that provide a steady income stream, usually designed for retirement income. They are offered by insurance companies, with the policyholder paying premiums into the annuity to grow the funds over time. At a specific time, known as the annuitization phase, the issuer begins to make regular payments back to the annuitant. Obtaining a license is not only a legal requirement for selling annuities but also a cornerstone in establishing one's credibility and trustworthiness in the financial services industry. Licensing ensures that the annuity seller has the required knowledge, skillset, and ethics to guide clients towards financial decisions that align with their long-term goals. The stringent licensing procedures and requirements are there to ensure that only qualified and competent individuals are authorized to sell complex financial products like annuities. Clients often entrust their life savings or retirement funds to annuity contracts, underscoring the vital importance of knowledgeable and ethically-minded professionals to guide them. The insurance license allows individuals to sell insurance products, including annuities. In the United States, each state has its insurance regulatory body, usually called the Department of Insurance, that governs the licensing process. While insurance licensing requirements can vary somewhat between states, they typically include pre-licensing education, a licensing exam, and a background check. Pre-licensing education is often the first step towards obtaining an insurance license. Most states require a specific number of hours of pre-licensing education, typically ranging from 20 to 40 hours. This education provides foundational knowledge about insurance principles, ethics, and state-specific laws and regulations. After completing the pre-licensing education, the next step is to pass the state's insurance licensing exam. This comprehensive test assesses the applicant's understanding of insurance laws, ethics, and various types of insurance, including annuities. Prior to applying for a license, applicants usually need to undergo a background check and fingerprinting. This step is to ensure that the applicant has a clean criminal record, demonstrating their suitability for a position of trust. Upon successful completion of the pre-licensing education, passing the exam, and clearing the background check, applicants can submit their license application to the state's insurance department. After reviewing and approving the application, the department will issue the insurance license. Once obtained, an insurance license is not valid indefinitely. Licensees must fulfill continuing education requirements and periodically renew their license according to state regulations. Continuing education ensures that insurance professionals stay up-to-date with industry changes and ethical standards. A Series 6 license, issued by the Financial Industry Regulatory Authority (FINRA), permits the holder to sell variable annuities and other investment products. The license indicates that the holder understands these complex financial products and has passed a comprehensive examination testing this knowledge. To begin the Series 6 licensing process, an individual must be sponsored by a FINRA member firm. This firm typically provides training and educational resources to prepare for the exam. This step involves an extensive study of investment product characteristics, regulatory standards, and ethical considerations. Many prospective licensees use exam preparation courses, study guides, and practice exams to prepare. The licensing process involves passing two exams: the SIE exam, which provides a broad overview of the securities industry, and the Series 6 exam, which focuses specifically on investment companies and variable contract products. Similar to an insurance license, the Series 6 license requires ongoing maintenance. Licensees must fulfill continuing education requirements and adhere to FINRA's standards of professional conduct to retain their license. The Certified Financial Planner designation, granted by the Certified Financial Planner Board of Standards, indicates that a financial advisor has met rigorous professional standards and adheres to a code of ethics. While not necessary to sell annuities, the CFP designation enhances a financial advisor's credibility and competency. The Chartered Financial Consultant designation, awarded by The American College of Financial Services, represents expertise in comprehensive financial planning. Like the CFP designation, the ChFC can boost a financial professional's reputation and skill set. The Chartered Life Underwriter designation, also awarded by The American College of Financial Services, indicates specialized knowledge in life insurance and estate planning. These agencies regulate the sale of insurance products, including annuities, within their respective states. They're responsible for licensing insurance agents and companies, approving insurance products for sale, and ensuring compliance with state insurance laws and regulations. They also investigate consumer complaints and take enforcement actions against agents or companies that violate state laws. FINRA is a self-regulatory organization that oversees broker-dealers and their registered representatives in the U.S. Although annuities are primarily regulated at the state level as insurance products, variable annuities fall under the purview of FINRA because they involve investment in securities. FINRA sets rules and guidelines for selling variable annuities, conducts examinations, and enforces compliance. It also offers dispute resolution services to consumers. The SEC is a federal agency that protects investors, maintains fair, orderly, and efficient markets, and facilitates capital formation. Like FINRA, the SEC also regulates variable annuities as securities products. The SEC requires that a prospectus be given to consumers when selling variable annuities to inform them about the investment's objectives, strategies, risks, and costs. One of the key regulations in selling annuities is the suitability rule. This rule requires that annuity recommendations made by financial advisors must be suitable for the client's financial situation and long-term goals. This requires an understanding of the client's risk tolerance, financial situation, tax status, and investment objectives. Many states have also adopted a best interest standard, which requires financial advisors to act in the best interest of their clients, even if it conflicts with their interests. Another crucial regulation pertains to disclosure. The financial advisor is required to provide clear, detailed information about the annuity product. This includes the terms and conditions, the fees and charges, the potential risks and returns, and the potential penalties for early withdrawal. For variable annuities, which are considered securities, the SEC requires the provision of a prospectus to the buyer. This document should contain detailed information about the investment, including the risks, performance, and costs associated with the annuity. Annuity sales are subject to anti-fraud provisions under both federal and state law. These provisions prohibit deceptive practices, such as misrepresentation or omission of material facts. Financial advisors are also subject to recordkeeping requirements. These requirements mandate that advisors keep accurate, detailed records of their interactions with clients, including their recommendations, the basis for those recommendations, and any disclosures provided. To provide the best advice, understand your client's financial situation, needs, and long-term goals. Consider factors such as the client's risk tolerance, retirement plans, health status, and potential future expenses. By fully understanding your client's financial needs and goals, you can match them with the most suitable annuity product. Annuities can be complex financial products. Therefore, it's essential to have a thorough understanding of the features, benefits, and potential drawbacks of the annuities you sell. This includes being able to explain complex terms and conditions in a manner that clients can easily understand. Transparency is key. Be clear about the terms and conditions, benefits, risks, and costs of the annuity products you're selling. Full disclosure builds trust and helps clients make informed decisions. Also, transparency is not just an ethical mandate; it's a regulatory requirement. Every client is unique, and so are their financial needs and goals. Tailor your service to each client's needs. Regularly review and adjust their financial plan and annuity contracts as their circumstances change. The financial services industry is continuously evolving. Stay updated with industry trends, product changes, and regulatory updates. This knowledge allows you to provide relevant advice and helps you stay compliant with industry regulations. Participate in continuing education to deepen your financial knowledge and stay informed about industry changes. Further, many financial licenses require ongoing education for renewal. Avoid high-pressure sales tactics that might lead clients to make rushed decisions. Instead, prioritize your client's best interests and guide them to make well-informed choices. Selling annuities isn't about making quick sales. It's about building long-term relationships based on trust. By showing your clients that you genuinely care about their financial well-being, you're more likely to retain them as clients and earn their referrals. Always adhere to the regulations set by regulatory bodies like FINRA, SEC, and state insurance departments. Non-compliance can lead to severe consequences, including fines, license revocation, and legal liability. Obtaining a license to sell annuities is not only a legal requirement but also a vital step in establishing credibility and trustworthiness in the financial services industry. The primary need for selling annuities is an insurance license, which involves fulfilling pre-licensing education requirements, passing a licensing exam, and undergoing a background check. Additionally, the Series 6 license issued by FINRA allows individuals to sell variable annuities and other investment products, requiring sponsorship from a member firm and passing comprehensive exams. Obtaining additional certifications like the Certified Financial Planner, Chartered Financial Consultant, or Chartered Life Underwriter can enhance a financial advisor's credibility and expertise in selling annuities. Ethical and compliance considerations play a significant role in selling annuities, with regulatory bodies such as state insurance departments, FINRA, and the SEC overseeing the industry and enforcing suitability, best interest standards, disclosure requirements, and anti-fraud provisions. Besides licensing, financial advisors should understand clients' needs, have in-depth knowledge of the products they sell, be transparent, provide personalized service, stay updated, practice ethical sales techniques, build long-term relationships, and follow regulatory guidelines. By meeting licensing and regulatory requirements and adhering to these best practices, financial advisors can ensure they are well equipped to guide clients through the complexities of annuity products, earn their trust, and navigate the ever-evolving financial services industry responsibly.Overview of Annuities

Definition

Importance of Licensing in Selling Annuities

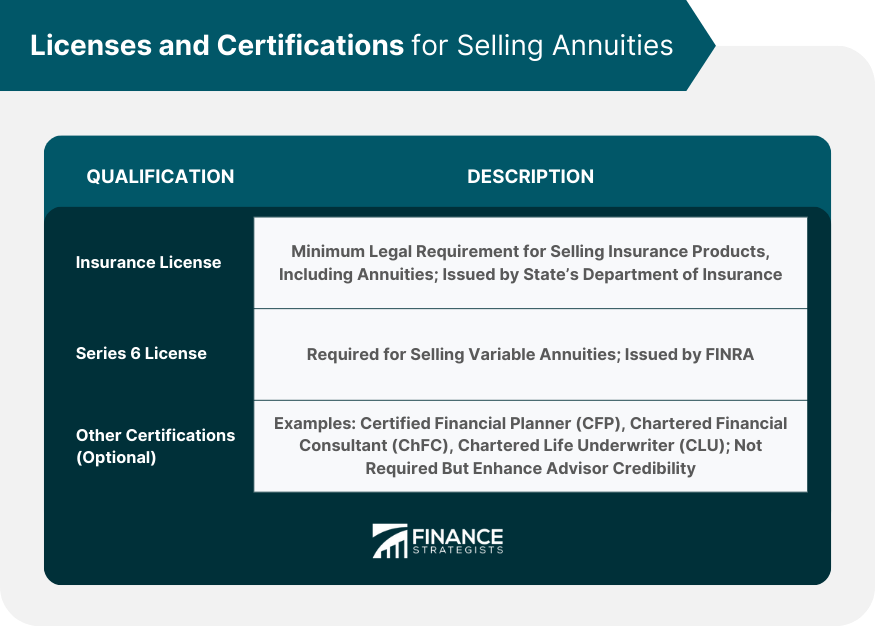

Primary Need: Insurance License

Definition

Steps to Acquire an Insurance License

Pre-licensing Education

Examination

Background Check and Fingerprinting

Submitting License Application

Maintenance and Continuing Education

Series 6 License: For Selling Variable Annuities

Definition

Procedure to Obtain a Series 6 License

Sponsorship From FINRA Member Firm

Preparation for the Examination

Passing Securities Industry Essentials (SIE) and Series 6 Exams

Maintenance and Continuing Education

Additional Certifications for Selling Annuities

Certified Financial Planner (CFP)

Chartered Financial Consultant (ChFC)

Chartered Life Underwriter (CLU)

This designation can be particularly beneficial for professionals selling annuities, given the close relationship between annuities and life insurance.

Ethical and Compliance Considerations in Selling Annuities

Regulatory Bodies

State Insurance Departments

Financial Industry Regulatory Authority

US Securities and Exchange Commission (SEC)

Key Regulations Besides Licensing

Suitability and Best Interest Standards

Disclosure Requirements

Anti-fraud Provisions

Recordkeeping Requirements

Best Practices for Selling Annuities

Understand Your Client's Needs

Know Your Product

Be Transparent

Provide Personalized Service

Keep Up With Industry Trends and Changes

Engage in Continuing Education

Practice Ethical Sales Techniques

Build Long-Term Relationships

Follow Regulatory Guidelines

Final Thoughts

What License Is Needed to Sell Annuities? FAQs

In the United States, individuals who wish to sell annuities typically need to obtain a state-specific insurance license. This license allows them to legally sell insurance products, including annuities, within that particular state. Additionally, individuals would need a Series 6 License from the Financial Industry Regulatory Authority (FINRA) to sell variable annuities and other products.

Yes, the requirements to obtain an insurance license to sell annuities may vary by state. However, common prerequisites include completing a pre-licensing education course, passing a licensing exam, and undergoing a background check. Additionally, some states may have additional training or continuing education requirements.

Generally, financial advisors who want to sell annuities need to hold an insurance license in addition to their financial advisor credentials. While financial advisors may provide guidance and advice regarding annuities, the actual sale of annuity products usually requires the appropriate insurance license.

Yes, if you intend to sell annuities in multiple states, you will generally need to obtain a license in each individual state where you plan to conduct business. The process and requirements for obtaining licenses may vary from state to state.

No, professional designations alone do not typically grant individuals the ability to sell annuities without an insurance license. Even if someone holds a recognized financial designation, such as a Certified Financial Planner (CFP), they would still need to obtain the necessary insurance license to sell annuities legally. However, financial designations boost a financial advisor’s credibility and expertise in selling annuities.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.