Flood insurance is a type of insurance policy that provides coverage for damage caused by flooding to your property and belongings. Floods can occur due to natural disasters like hurricanes, heavy rain, or snowmelt, and they can cause extensive damage to your home or business. While standard homeowners insurance policies typically do not cover flood damage, flood insurance can provide the protection you need to recover from a flood-related loss. Flood insurance policies are typically offered through the National Flood Insurance Program (NFIP), which is administered by the Federal Emergency Management Agency (FEMA). The National Flood Insurance Program (NFIP) is a federally backed program established in 1968 to provide affordable flood insurance to homeowners, renters, and business owners in participating communities. The primary goal of the NFIP is to reduce the impact of flooding on individuals and communities by providing financial protection and promoting floodplain management. To be eligible for NFIP coverage, the property must be located in a participating community that has agreed to adopt and enforce floodplain management regulations. NFIP policies offer two types of coverage: building coverage and contents coverage. Policyholders can purchase one or both types of coverage. Private flood insurance is provided by private insurance companies as an alternative to the NFIP. It is designed to offer more flexible and comprehensive coverage options for homeowners and businesses that may not be eligible for NFIP coverage or require additional protection. Private flood insurance is available to homeowners and businesses in both participating and non-participating NFIP communities. Coverage options vary by company and may include building, contents, and excess flood insurance. Excess flood insurance provides additional coverage beyond the limits of NFIP or private flood insurance policies. It is designed to protect high-value properties and assets from catastrophic flood damage. Excess flood insurance is available to homeowners and businesses with NFIP or private flood insurance policies. Coverage amounts and options may vary depending on the insurer and the specific policy. Building coverage provides protection for the physical structure of the insured property, including its foundation, walls, roof, and other essential components. Building coverage may also include protection for appliances and utilities, such as heating and cooling systems, electrical wiring, and plumbing. Contents coverage provides protection for personal belongings within the insured property, including furniture, clothing, and electronics. Some flood insurance policies may offer coverage for valuables and collectibles, such as artwork and jewelry, up to a specified limit. Flood insurance policies typically exclude coverage for damage caused by gradual deterioration, such as mold or mildew. Flood insurance policies generally do not cover flooding caused by earth movements, such as landslides or earthquakes. Flood insurance premiums are primarily determined by the property's flood risk and zone classification, as determined by the Federal Emergency Management Agency (FEMA). The policyholder's choice of deductibles and coverage limits will also affect the cost of flood insurance. Higher deductibles and lower coverage limits can reduce premiums, but may also increase out-of-pocket expenses in the event of a claim. Building characteristics, such as age, construction materials, and elevation, can also influence flood insurance costs. Some insurers may offer discounts or premium reductions for properties with certain flood mitigation measures, such as elevation or floodproofing. To purchase an NFIP policy, property owners can contact a local insurance agent who is authorized to sell NFIP policies. The agent will help determine eligibility, coverage options, and policy costs. Once an agent has been selected, the property owner will need to complete an application and provide the necessary documentation to obtain the policy. There may be a 30-day waiting period before the policy becomes effective. To purchase private or excess flood insurance, property owners can compare coverage options and costs from different insurance companies. It is recommended to obtain quotes from multiple providers to find the best policy for their needs. Similar to the NFIP application process, property owners will need to complete an application and provide the necessary documentation to obtain a private or excess flood insurance policy. Waiting periods may vary depending on the insurer and specific policy. In the event of a flood, property owners should document the damage, take photographs or videos, and make a list of damaged items. They should then contact their insurance agent or company to initiate the claims process. An adjuster will be assigned to assess the damage and determine the claim payout. Property owners should cooperate with the adjuster by providing access to the property, answering questions, and submitting any requested documentation. Once the claim has been processed, the property owner will receive compensation based on the terms of their policy. Payout options may include actual cash value or replacement cost, depending on the policy. If a property owner disagrees with the adjuster's assessment, they may appeal the decision by providing additional documentation or requesting a reevaluation. After a flood, property owners should take steps to prevent further damage and reduce the risk of future flooding. This may include installing flood barriers, elevating utilities, and implementing proper drainage systems. Local, state, and federal assistance programs may be available to help property owners recover from flood damage and implement flood mitigation measures. As climate change continues to increase the frequency and severity of flooding events, the demand for flood insurance and the associated costs are expected to rise. Technological advancements, such as improved flood mapping and predictive modeling, may help insurance providers better assess flood risks and offer more accurate pricing. As the flood insurance landscape evolves, regulatory changes and policy updates may be implemented to address emerging challenges and ensure the continued availability of affordable flood insurance options. Flood insurance is a crucial component of disaster planning for property owners. It offers financial protection against losses that are typically excluded from standard homeowners' insurance policies, and helps individuals and communities recover from the devastating effects of flooding events. By understanding the different types of flood insurance, coverage options, and the claims process, homeowners and businesses can make informed decisions and better protect themselves from the financial impact of floods. However, as climate change continues to increase the frequency and severity of flooding events, the future of flood insurance remains uncertain. Insurance providers will need to adapt to changing risk profiles and invest in new technologies to accurately assess flood risks and offer affordable pricing. Furthermore, regulatory changes and policy updates will be necessary to ensure the availability of affordable flood insurance options. As such, it is crucial that property owners stay informed and be proactive in securing adequate flood insurance coverage to protect themselves and their property.What Is Flood Insurance?

Types of Flood Insurance

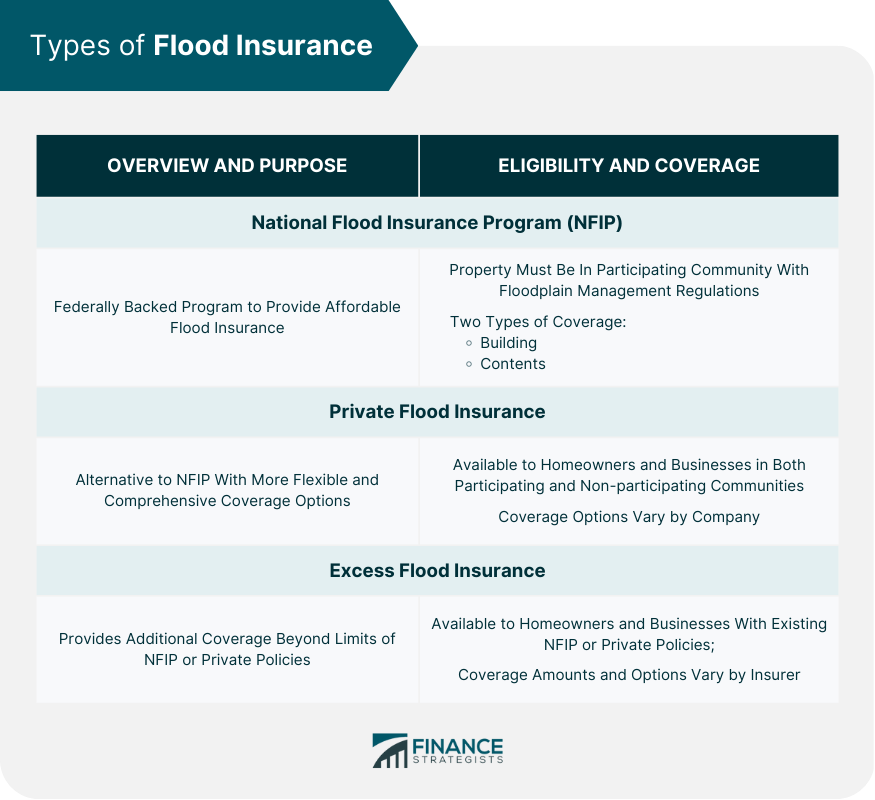

National Flood Insurance Program (NFIP)

Overview and Purpose

Eligibility and Coverage

Private Flood Insurance

Overview and Purpose

Eligibility and Coverage

Excess Flood Insurance

Overview and Purpose

Eligibility and Coverage

Flood Insurance Coverage

Building Coverage

Structural Elements

Appliances and Utilities

Contents Coverage

Personal Belongings

Valuables and Collectibles

Exclusions and Limitations

Gradual Damage

Earth Movement-Related Flooding

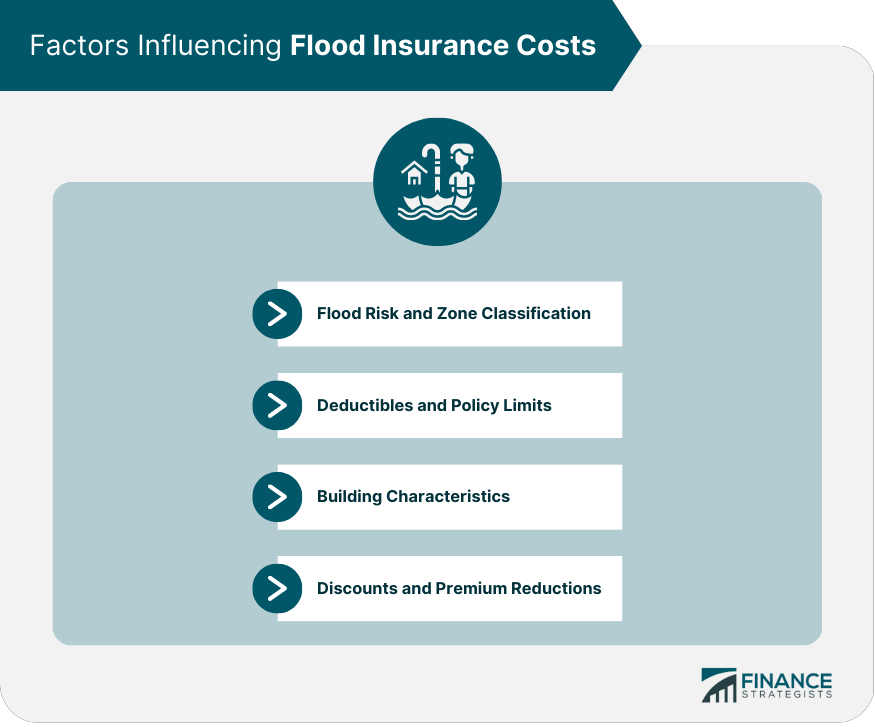

Factors Influencing Flood Insurance Costs

Flood Risk and Zone Classification

Deductibles and Policy Limits

Building Characteristics

Discounts and Premium Reductions

How to Purchase Flood Insurance

NFIP Policies

Finding an Agent

Application Process

Private and Excess Flood Insurance

Shopping Around

Application Process

Claims Process and Recovery

Filing a Flood Insurance Claim

Documentation and Assessment

Working With Adjusters

Receiving Compensation

Payout Options

Appealing Claim Decisions

Post-Disaster Recovery

Preventative Measures

Community Assistance Programs

Future of Flood Insurance

Impact of Climate Change on Flood Insurance

Technological Advancements

Regulatory Changes and Policy Updates

Conclusion

Flood Insurance FAQs

Flood insurance is a type of insurance policy that covers damage caused by flooding to your property and belongings. Floods can occur due to natural disasters like hurricanes, heavy rain, or snowmelt, and they can cause extensive damage to your home or business. While standard homeowners insurance policies typically do not cover flood damage, flood insurance can provide the protection you need to recover from a flood-related loss.

Anyone who owns property in an area that is at risk for flooding should consider purchasing flood insurance. This includes homeowners, renters, and business owners who live or operate in flood-prone areas. Even if you do not live in a high-risk flood zone, it is still a good idea to have flood insurance, as floods can happen anywhere and can cause significant damage.

The cost of flood insurance depends on a variety of factors, including the location and elevation of your property, the amount of coverage you need, and your flood risk. Premiums for NFIP policies typically range from a few hundred to several thousand dollars per year, depending on the level of coverage and your flood risk.

Flood insurance typically covers damage to your property and belongings caused by flooding, including structural damage, damage to appliances and fixtures, and damage to personal belongings like furniture, clothing, and electronics. Some policies may also provide coverage for additional expenses like temporary housing and living expenses if you are unable to live in your home due to flood damage.

Flood insurance is available through the National Flood Insurance Program (NFIP), which is administered by the Federal Emergency Management Agency (FEMA). You can purchase an NFIP policy through a licensed insurance agent, or you can contact the NFIP directly to find an agent in your area. Some private insurance companies also offer flood insurance policies, so it's worth shopping around to find the best coverage and rates for your needs.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.