Reinsurance is a fundamental practice in the insurance industry, wherein insurance companies transfer a portion of their risks to other entities called reinsurers. It involves an agreement between the insurer and the reinsurer, where the reinsurer agrees to indemnify the insurer for a share of the losses incurred on the policies they underwrite. Reinsurance enables insurers to manage their exposure to risks, maintain financial stability, and protect their capital. It helps spread risks across a broader pool of participants, mitigating the impact of large losses and providing insurers with the confidence to underwrite policies with higher limits. Reinsurance is a vital tool for risk management in the insurance ecosystem. There are several types of reinsurance, each with its unique characteristics and benefits. Insurers choose the most appropriate type of reinsurance based on their risk profile, financial objectives, and market conditions. Proportional reinsurance is a type of reinsurance where the insurer and reinsurer share the premiums and losses proportionally. There are two main forms of proportional reinsurance: In a quota share arrangement, the insurer, and reinsurer agree to share a fixed percentage of all premiums and losses. This type of reinsurance is popular among small and medium-sized insurers, as it provides a stable source of income and a predictable distribution of risk. Surplus share reinsurance allows the insurer to cede a portion of the risk exceeding a specified retention limit. This type of reinsurance is particularly beneficial for insurers looking to protect against large, infrequent losses, as it provides coverage for risks that may exceed the insurer's capacity. Non-proportional reinsurance is a type of reinsurance where the reinsurer only covers losses exceeding a specified threshold. There are two primary forms of non-proportional reinsurance: In an excess of loss arrangement, the reinsurer covers losses above a predetermined limit, up to a specified maximum. This type of reinsurance is commonly used to protect against catastrophic events, such as natural disasters or large-scale accidents. Stop loss reinsurance provides coverage when the insurer's total losses exceed a specified percentage of its earned premiums. This type of reinsurance helps insurers protect against adverse loss ratios and maintain financial stability. Facultative reinsurance is a type of reinsurance where the insurer and reinsurer negotiate coverage for individual risks on a case-by-case basis. This type of reinsurance is often used for high-risk or unusual exposures that may not be covered under a treaty reinsurance agreement. Treaty reinsurance is a type of reinsurance where the insurer and reinsurer enter into a long-term agreement to cover a specific portfolio of risks. Treaty reinsurance can be structured as proportional or non-proportional, depending on the needs of the insurer and reinsurer. Reinsurance plays a crucial role in managing risk for property and casualty insurers. These insurers often face significant financial exposure due to natural disasters, accidents, and other unforeseen events, making reinsurance an essential tool for risk management. Property and casualty insurers use reinsurance to protect their balance sheets from large, unexpected losses. Reinsurance allows these insurers to spread their risk across a broader pool of participants, reducing the likelihood of insolvency following a catastrophic event. Insurers use various reinsurance strategies to manage their exposure to property and casualty risks. These strategies may include: Purchasing catastrophe reinsurance to protect against extreme events, such as hurricanes or earthquakes Utilizing excess of loss reinsurance to cover high-severity, low-frequency losses Employing quota share reinsurance to share risk and premiums with reinsurers, providing additional capacity and capital relief Catastrophe reinsurance is a critical component of property and casualty insurance, providing coverage for losses resulting from large-scale natural disasters or other catastrophic events. This type of reinsurance helps insurers maintain financial stability and continue to operate in the aftermath of such events. Catastrophe reinsurance can be structured as a standalone policy or integrated into a broader reinsurance program. Climate change has become an increasingly important consideration for property and casualty insurers and reinsurers. As the frequency and severity of weather-related events continue to rise, insurers face mounting losses and increased demand for reinsurance coverage. To address this challenge, reinsurers are developing new products and leveraging advanced analytics to better understand and price climate-related risks. The global reinsurance market is a dynamic and competitive landscape, with a diverse array of participants ranging from traditional reinsurers to alternative capital providers. The reinsurance market is characterized by a mix of large, multinational companies and smaller, regional players. Market conditions can fluctuate significantly based on factors such as natural disasters, economic trends, and regulatory changes. Insurers and reinsurers must continuously adapt to remain competitive and meet the evolving needs of their clients. Some of the leading reinsurance companies in the global market include Swiss Re, Munich Re, Hannover Re, and SCOR. These companies offer a broad range of reinsurance products and services, including property and casualty reinsurance, life and health reinsurance, and specialty line coverage. Insurance brokers plays a vital role in the reinsurance market, connecting insurers with reinsurers and facilitating transactions. Brokers help insurers identify suitable reinsurance partners, negotiate contract terms, and manage claims and settlements. They also provide valuable market intelligence and insights to help insurers make informed decisions about their reinsurance strategies. The reinsurance market faces several trends and challenges, including: Increased competition from alternative capital providers, such as pension funds and hedge funds Regulatory changes, such as the implementation of Solvency II in Europe The growing impact of climate change on property and casualty reinsurance Technological advancements, including the rise of insurtech and the use of big data analytics The reinsurance industry operates within a complex regulatory framework, with oversight from national and international bodies. Regulatory bodies, such as the National Association of Insurance Commissioners (NAIC) in the United States or the European Insurance and Occupational Pensions Authority (EIOPA) in Europe, are responsible for overseeing the reinsurance industry and ensuring compliance with relevant laws. These bodies establish standards for capital adequacy, risk management, and corporate governance, among other areas. Reinsurance regulations vary by jurisdiction, but some of the key regulations that impact the industry include: Solvency requirements, which dictate the minimum level of capital that insurers and reinsurers must maintain to remain solvent Risk management and governance requirements, which set expectations for how insurers and reinsurers should manage their operations and mitigate risks Disclosure and transparency requirements, which mandate that insurers and reinsurers provide detailed information about their financial condition, risk exposures, and business strategies Solvency II is a regulatory framework implemented by the European Union, which sets out capital requirements and risk management standards for insurers and reinsurers. The introduction of Solvency II has had a significant impact on the reinsurance industry, driving changes in capital management practices, risk modeling, and reporting. Regulations can have far-reaching implications for insurance brokers and property and casualty insurers. Regulatory changes may affect the way brokers operate, requiring them to adapt their business models or invest in new technologies to remain compliant. For property and casualty insurers, regulations may influence their risk management strategies, capital requirements, and reinsurance purchasing decisions. Insurance brokers play a crucial role in the reinsurance process, acting as intermediaries between insurers and reinsurers to facilitate transactions and ensure that both parties needs are met. Insurance brokers are responsible for a variety of tasks in the reinsurance process, including: Identifying suitable reinsurance partners based on the insurer's risk profile and coverage needs Negotiating contract terms, including coverage limits, premiums, and deductibles Managing the placement of reinsurance contracts and ensuring compliance with all regulatory requirements Assisting with claims management and settlement processes Insurance brokers play a critical role in the placement of reinsurance contracts. They work closely with insurers to understand their risk profiles and coverage needs and then use their market knowledge and relationships to identify potential reinsurance partners. Brokers are often heavily involved in reinsurance contract negotiations, working on behalf of insurers to secure favorable terms and conditions. Insurance brokers play a vital role in the claims management and settlement process, acting as intermediaries between insurers and reinsurers. They help insurers navigate the complexities of the reinsurance claims process, including the submission of claims, the provision of supporting documentation, and the negotiation of settlements. Reinsurance is a critical component of the insurance industry, enabling insurers to transfer risk and maintain financial stability. There are various types of reinsurance, including proportional (quota share, surplus share), non-proportional (excess of loss, stop loss), facultative, and treaty reinsurance. Reinsurance plays a crucial role in managing risk for property and casualty insurers, offering protection against catastrophic losses. Catastrophe reinsurance is particularly important in covering large-scale natural disasters. Leading reinsurance companies include Swiss Re, Munich Re, Hannover Re, and SCOR. Insurance brokers play a vital role in the reinsurance market, connecting insurers with reinsurers, negotiating contracts, and managing claims. The reinsurance market faces challenges from alternative capital providers, regulatory changes, climate change impacts, and technological advancements. Regulations, such as Solvency II, impact reinsurance practices, risk management, and capital requirements. Insurance brokers assist in facilitating reinsurance transactions, from identifying suitable partners to negotiating contracts and managing claims.Definition of Reinsurance

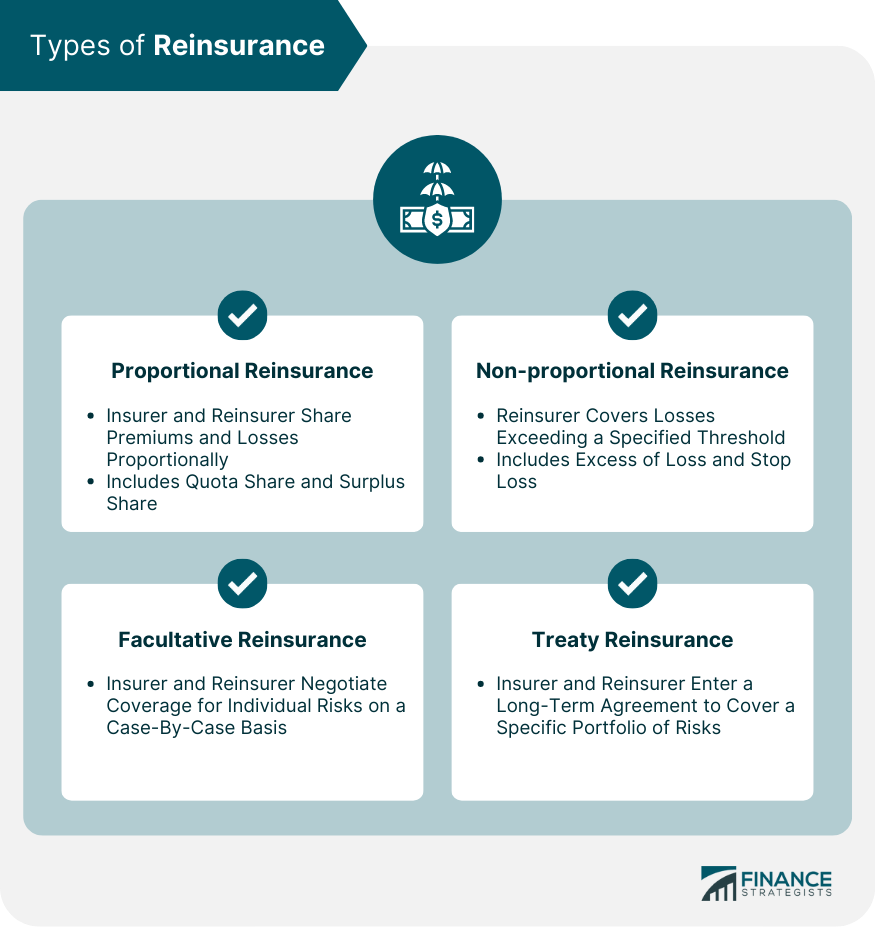

Types of Reinsurance

Proportional Reinsurance

Quota Share

Surplus Share

Non-Proportional Reinsurance

Excess of Loss

Stop Loss

Facultative Reinsurance

Treaty Reinsurance

Reinsurance in Property and Casualty Insurance

Risk Management for Property and Casualty Insurers

Reinsurance Strategies for Property and Casualty Insurance

Catastrophe Reinsurance

Impact of Climate Change on Property and Casualty Reinsurance

Reinsurance Market and Key Players

Global Reinsurance and Market Conditions

Leading Reinsurance Companies

Insurance Broker's Role in Reinsurance Market

Market Trends and Challenges

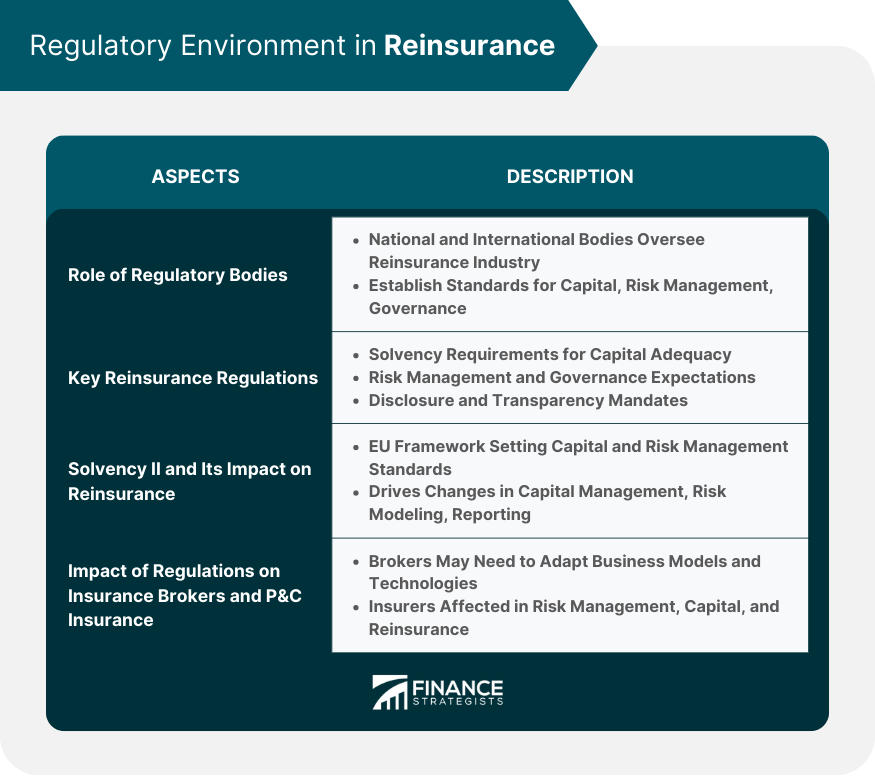

Regulatory Environment in Reinsurance

Role of Regulatory Bodies

Key Reinsurance Regulations

Solvency II and Its Impact on Reinsurance

Impact of Regulations on Insurance Brokers and Property and Casualty Insurance

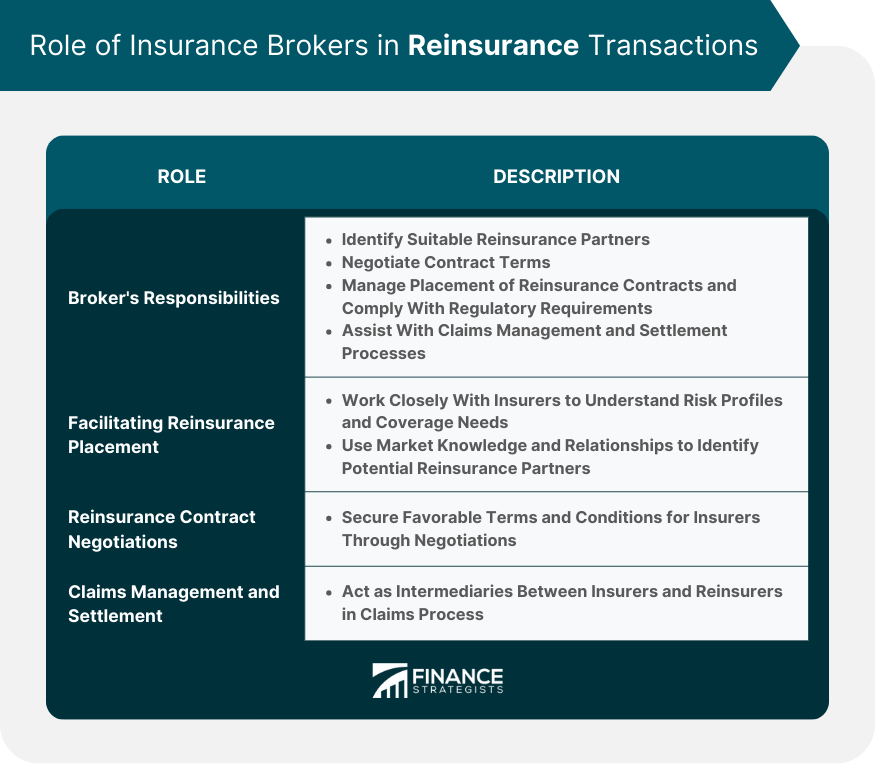

Role of Insurance Brokers in Reinsurance Transactions

Broker's Responsibilities

Facilitating Reinsurance Placement

Brokers also help insurers navigate the complexities of the reinsurance market, ensuring that they secure the best possible terms for their coverage.Reinsurance Contract Negotiations

This may involve negotiating coverage limits, premiums, deductibles, and other contractual provisions. Brokers also help insurers understand the implications of different reinsurance structures and make informed decisions about their risk management strategies.Claims Management and Settlement

Bottom Line

Reinsurance FAQs

Reinsurance is the practice of transferring a portion of an insurer's risk to another party, allowing insurers to manage their capital more effectively, protect against catastrophic losses, and maintain financial stability. It is particularly important for property and casualty insurers, as they often face significant financial exposure due to natural disasters, accidents, and other unforeseen events.

Insurance brokers play a crucial role in the reinsurance process by connecting insurers with reinsurers and facilitating transactions. They help insurers identify suitable reinsurance partners, negotiate contract terms, manage claims and settlements, and provide valuable market intelligence and insights to help insurers make informed decisions about their reinsurance strategies.

There are several types of reinsurance available for property and casualty insurers, including proportional reinsurance (quota share and surplus share), non-proportional reinsurance (excess of loss and stop loss), facultative reinsurance, and treaty reinsurance. Insurers choose the most appropriate type of reinsurance based on their risk profile, financial objectives, and market conditions.

Climate change has increased the frequency and severity of weather-related events, leading to mounting losses for property and casualty insurers and increased demand for reinsurance coverage. Emerging technologies, such as insurtech, blockchain, and big data analytics, are transforming the reinsurance industry by streamlining processes, improving risk assessment, and enhancing customer experiences.

Regulatory bodies, such as the National Association of Insurance Commissioners (NAIC) or the European Insurance and Occupational Pensions Authority (EIOPA), oversee the reinsurance industry and ensure compliance with relevant laws and regulations. They establish standards for capital adequacy, risk management, corporate governance, and other areas, helping to maintain the stability and integrity of the reinsurance market.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.