A Valued Marine Policy is a unique type of marine insurance that assigns a pre-determined value to the insured subject, usually a vessel or cargo. Distinct from most insurance policies that base compensation on actual cash value or replacement cost at loss time, this policy compensates based on the value set when the policy begins. This established value serves as a critical financial safety net for maritime businesses, particularly in total loss scenarios. Valued Marine Policies hold substantial relevance in the insurance sector, particularly for those involved in maritime transport, such as shipowners, freight companies, and businesses in maritime trade. They provide a predictable compensation level in case of loss, mitigating the inherent risk and uncertainty of maritime activities. With the continual growth of global trade and increasing dependence on maritime transportation, the significance of Valued Marine Policies in the insurance industry will undoubtedly escalate. The concept of a Valued Marine Policy has its roots in the marine insurance practices of the 17th century. As global sea trade began to boom, shipowners and merchants needed a way to protect themselves from significant financial losses resulting from maritime perils. Originally, this insurance was based on the actual value of the ship or cargo, creating uncertainties and disputes when losses occurred. This led to the creation of the Valued Marine Policy, which defined an agreed value for the insured items upfront, simplifying claims and ensuring fair compensation for losses. As maritime trade has evolved and expanded, so has the Valued Marine Policy. The complexity and diversity of modern maritime operations have necessitated adaptations to meet the varying needs of policyholders. Today's Valued Marine Policies may include coverage for a variety of risks, from physical loss or damage to the ship and cargo to other associated costs such as salvage and general average contributions. Additionally, modern policies often incorporate flexibility to accommodate the changing value of ships and cargo over the policy term. One of the most distinctive features of a Valued Marine Policy is its agreed value coverage. The insured and insurer agree upon a specified value of the ship or cargo at the onset of the policy. This value is the maximum amount that the insurer will pay in the event of a total loss. The agreed value provides a clear understanding of potential financial recovery, making it easier for businesses to plan their risk management and financial strategies. A standard Valued Marine Policy covers loss or damage to the insured vessel or cargo arising from a range of marine risks. These may include perils of the sea, such as storms and waves, as well as human-related perils, like piracy, jettison, and collisions. Some policies may also cover war risks and other specified perils. Depending upon the terms and conditions, partial losses might also be covered under the policy. The uniqueness of a Valued Marine Policy also extends to other aspects. For instance, it generally covers expenses related to averting or minimizing a loss (sue and labor costs) and general average losses, where the loss is voluntarily incurred for the benefit of all interests in a maritime venture. Another unique feature is the concept of "constructive total loss," where recovery or repair of the ship or cargo is either legally or physically impossible, or the cost of recovery or repair exceeds the insured value. In such cases, the policyholder can claim a total loss. The declaration section of a Valued Marine Policy sets out the essential details of the insurance agreement. It includes information such as the name of the insured, the insurer, the policy period, the insured vessel or cargo, the voyage or location covered, and the agreed value of the subject matter insured. The insuring agreement defines the scope of coverage under the policy. It outlines the perils insured against and the circumstances under which the insurer will pay a claim. It usually includes physical loss or damage caused by marine perils, along with any other risks specifically agreed upon. Like all insurance policies, Valued Marine Policies have exclusions and exceptions which outline what is not covered by the policy. These can include losses resulting from illegal activities, losses due to the inherent vice of the goods, and losses occurring outside the geographical area defined in the policy. The conditions section includes the obligations of the insured and insurer and how the policy operates. It may contain provisions about payment of premiums, obligations in the event of a loss, and requirements for maintaining the insurable interest. Endorsements or riders can be added to a Valued Marine Policy to broaden, restrict, or otherwise alter the coverage provided. These may be used to add additional perils, extend the policy's geographical area, or include other interests, such as freight earnings or disbursements. Hull insurance is a type of valued marine policy that covers physical loss or damage to the vessel itself, including its machinery and equipment. The policy is typically taken out by the shipowner, and the agreed value is often the cost of completely rebuilding the ship. It may also cover additional expenses, such as salvage costs or expenses to prevent further loss. Cargo insurance provides coverage for physical loss or damage to goods while in transit. The policy is usually taken out by the owner of the goods (which could be the shipowner, the charterer, or a third party), and the agreed value is typically the cost of the cargo plus freight and a certain percentage of profit. Freight insurance provides coverage for the freight at risk. If the ship or cargo is lost, the shipowner may also lose the freight they would have earned. This type of valued marine policy allows the shipowner to insure the freight, providing an additional layer of financial protection. While not a valued policy in the traditional sense, Protection and Indemnity (P&I) insurance is an essential part of a shipowner’s risk management strategy. P&I Clubs provide coverage for third-party liabilities such as damage to other ships, pollution, and injury or illness of crew members. Valued Marine Policies play a significant role in loss prevention and mitigation. The financial protection provided by these policies encourages businesses to invest in safety measures to prevent losses and maintain the condition of their vessels and cargo. In the event of a partial loss, the policy might cover the costs of necessary repairs, thus preventing further damage. By providing coverage for the agreed value of the vessel or cargo, Valued Marine Policies offer financial protection for businesses against unexpected losses. This can ensure business continuity, even in the case of significant loss events. The assurance of financial recovery allows businesses to rebound quickly and effectively from setbacks. Valued Marine Policies form an integral part of the overall risk management strategy for businesses in the maritime industry. Alongside safety protocols, maintenance programs, and loss prevention initiatives, these insurance policies provide a financial safety net, enhancing business resilience and long-term sustainability. In the event of a loss covered under a Valued Marine Policy, the insured must notify the insurer as soon as possible. The claim typically includes details of the loss event, evidence supporting the loss, and proof of the insured's interest. Depending on the nature of the loss, a surveyor may be appointed to assess the damage and estimate the cost of repair or replacement. Disputes may arise from disagreements over the cause of loss, the value of the loss, or the interpretation of policy terms. In these cases, resolution can be sought through negotiation, mediation, arbitration, or legal action. For instance, a dispute over whether a loss was caused by a peril covered by the policy might be resolved by interpreting the policy wording or examining the circumstances of the loss. While the agreed value under a Valued Marine Policy provides a clear maximum limit for a total loss claim, various factors can affect the settlement amount. These include the terms and conditions of the policy, any deductibles that apply, the extent of the loss or damage, and the cost of repairs or salvage operations. Various international conventions regulate marine insurance, including Valued Marine Policies. These conventions set standards for the terms and conditions of policies, the rights and obligations of the insured and insurer, and dispute resolution procedures. National legislation also governs marine insurance. This can vary significantly between countries and regions, affecting the operation of Valued Marine Policies. In many jurisdictions, the legislation specifies the obligations of the insurer and insured, the construction of policy terms, and the handling of claims and disputes. Case law plays a crucial role in interpreting the terms and conditions of Valued Marine Policies and resolving disputes. Legal precedents established in court decisions can significantly impact the operation of these policies and the outcomes of claims. Some critics argue that the valuation clause in a Valued Marine Policy can lead to moral hazard, as it may encourage the insured to act recklessly, knowing that they will receive the agreed value regardless of the actual value of the loss. However, defenders of the policy argue that the clause provides certainty and simplifies the claims process. Valued Marine Policies can be susceptible to fraud, with dishonest insureds inflating the value of their ship or cargo to receive higher compensation in the event of a loss. Insurers must be vigilant and conduct proper due diligence when agreeing on the value of the insured items. Both underinsurance and over-insurance can pose problems in a Valued Marine Policy. If the agreed value is less than the actual value of the ship or cargo (underinsurance), the insured may not receive adequate compensation in the event of a loss. Conversely, if the agreed value is more than the actual value (over-insurance), the insured might be paying unnecessarily high premiums. A Valued Marine Policy is a specialized marine insurance that provides crucial financial protection to maritime businesses by assigning a predetermined value to a vessel or cargo. With unique features like agreed value and loss or damage coverage, it is an integral part of risk management in the maritime sector. The policy offers comprehensive coverage through its structured sections, including declarations, insuring agreements, exclusions, conditions, and endorsements. Different policy types like hull, cargo, freight, and liability insurance cater to varied needs in the sector. These policies play a key role in risk management, from loss prevention to ensuring financial protection and business continuity. As the maritime trade landscape evolves, understanding the nuances of Valued Marine Policies becomes increasingly important. Therefore, businesses are advised to consult a qualified insurance broker to secure tailored coverage.Overview of Valued Marine Policy

Historical Development of the Valued Marine Policy

Origins and Early Use

Evolution and Modern Adaptations

Key Features of a Valued Marine Policy

Agreed Value Coverage

Loss or Damage Coverage

Other Unique Aspects

Structure of a Valued Marine Policy

Declaration Section

Insuring Agreement

Exclusions and Exceptions

Conditions

Endorsements and Riders

Types of Valued Marine Policies

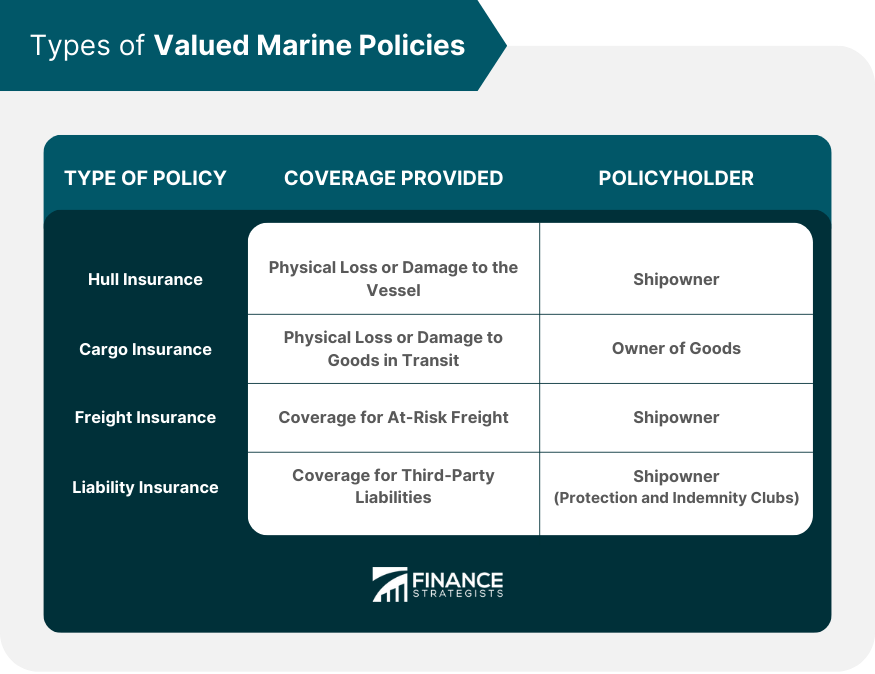

Hull Insurance

Cargo Insurance

Freight Insurance

Liability Insurance (Protection and Indemnity)

Role of Valued Marine Policy in Risk Management

Loss Prevention and Mitigation

Financial Protection and Business Continuity

Contribution to Overall Risk Management Strategy

Valued Marine Policy: Claims and Settlements

Process of Filing a Claim

Typical Dispute Scenarios and Resolutions

Factors Affecting the Settlement Amount

Legal and Regulatory Aspects of a Valued Marine Policy

International Regulations

National Legislation

Case Laws and Legal Precedents

Challenges and Criticisms of Valued Marine Policies

Arguments Against Valuation Clause

Problems Related to Fraud

Underinsurance and Over-Insurance Issues

Final Thoughts

Valued Marine Policy FAQs

A Valued Marine Policy is a type of insurance that provides coverage for an agreed value of a vessel or its cargo, which is determined at the beginning of the policy term.

Key features of a Valued Marine Policy include agreed value coverage, loss or damage coverage, and coverage for other unique aspects such as salvage costs and general average losses.

The different types of Valued Marine Policies include hull insurance, cargo insurance, freight insurance, and liability insurance (Protection and Indemnity).

A Valued Marine Policy contributes to risk management by offering loss prevention and mitigation, providing financial protection and business continuity, and forming an integral part of the overall risk management strategy.

You can get a Valued Marine Policy from insurance companies that offer marine insurance. It's recommended to seek advice from a qualified and experienced insurance broker to ensure you get a policy that suits your needs.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.