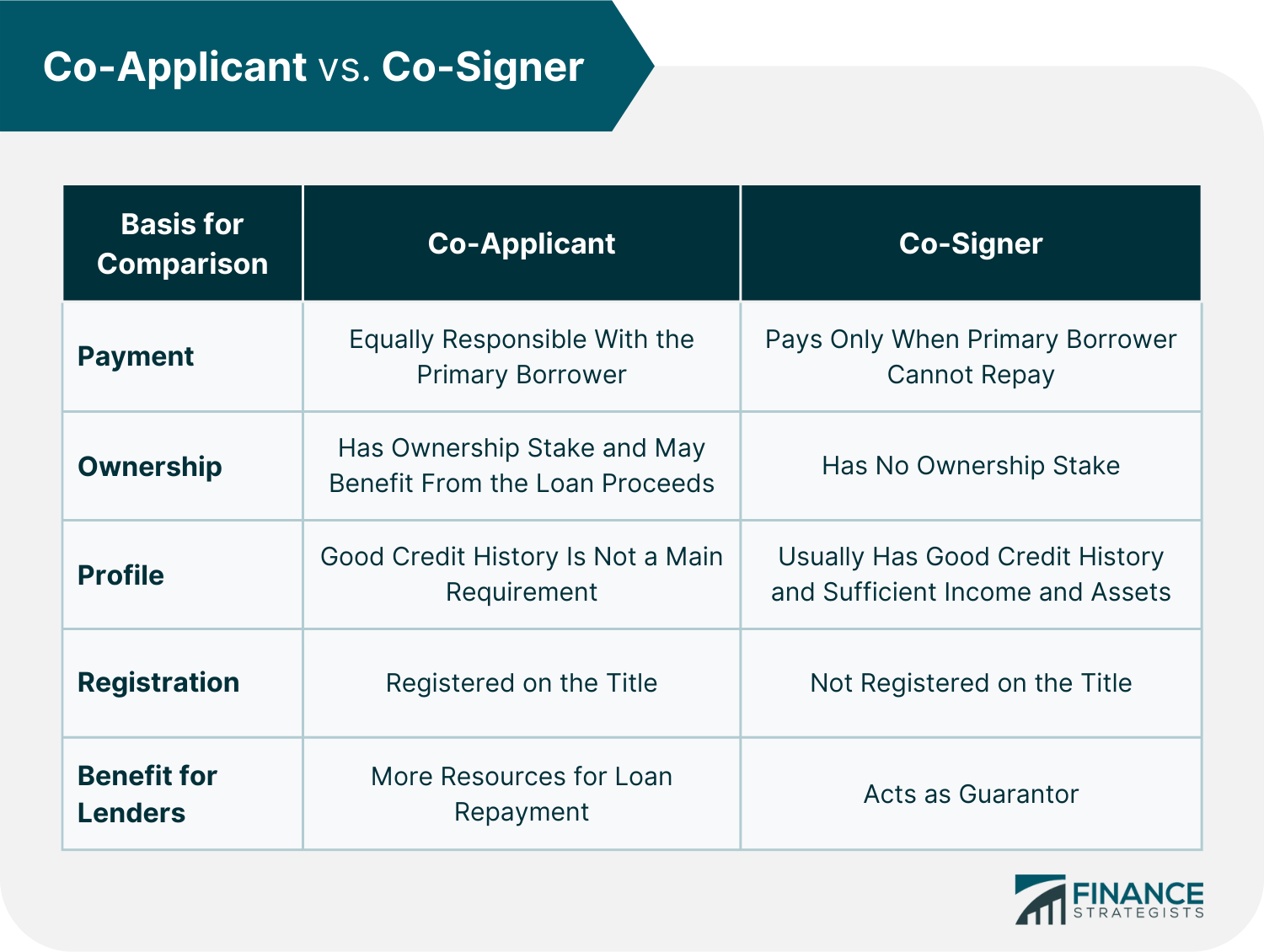

A co-applicant is an individual who applies for a loan with another person. The co-applicant's name will appear on the agreement, and they will be jointly liable for repaying the debt. A co-applicant's income and credit history will also be considered during the loan underwriting and approval process. Having a co-applicant might increase the likelihood of loan approval and improve loan terms. A mortgage application from a married couple is one example of this. Both partners' incomes and credit histories are considered since they applied jointly for the loan. If both applicants have strong credit profiles, the lender is more likely to approve the loan and offer better terms. Applying for a loan with a co-applicant involves the same process as applying for one individual. Both applicants must fill out their personal information and sign the application. When lenders consider loan applications, they prefer lending to those who present lesser risk. Since more resources are available for repayment with two applicants, lenders might look more favorably on these applications. The credit profiles of both applicants will be considered. If one person has a weaker credit history than the other, having a co-applicant can significantly increase the chances of the loan being approved. Upon loan approval, both applicants share in the benefits of the debt and the responsibility of repaying it. The following are some possible candidates to act as co-applicants in financial transactions: Some lenders may prefer co-applicants who are family members. For example, a parent might assist their college-aged child in obtaining a vehicle loan since the student presumably lacks the credit score necessary to qualify for personal loans. Spouses can be co-applicants because they generally live together, share many expenses, and may have financial stability. They are typically more familiar with the other person's finances and more likely to support each other in meeting loan repayments. A business partner is a good co-applicant because they likely know the ins and outs of the business's finances. This relationship can build trust with lenders, which may lead to a more favorable loan agreement. There are several advantages to applying for financial transactions with co-applicants. One of the primary considerations for including a co-applicant is that it may improve the chances of getting approved. Lenders typically want to see a strong credit history and income when considering a loan application. The borrower becomes more attractive if they have a co-applicant with a good credit score. The lender sees someone else responsible for repaying the debt, which lowers the risk for them. In some cases, having a co-applicant helps get better loan terms. For example, applicants can be granted an extended repayment period or a higher loan amount. Additionally, borrowers may get lower interest rates. If the application is robust, it can receive more favorable conditions. With a co-applicant, an individual can potentially borrow more money because the lender will consider both applicants' combined income when evaluating the loan. For instance, let us say someone is applying for a $100,000 loan alone. The lender may only approve $80,000 based on the individual's income. However, if the individual has a co-applicant who also earns an income, the lender may be more likely to approve the $100,000 loan amount in full. Several factors must be considered when selecting a co-applicant. Here are some of them: It is important to designate someone who has a strong credit score and who poses less risk to lenders. Most people think of a good credit score as 700 or higher, indicating that the individual has a history of making payments on time and has not accumulated too much debt. A co-applicant should have a robust financial background, which includes a long employment history, a low debt-to-income ratio, a good credit score, and a steady income. It is essential to look for a trustworthy co-applicant who can make payments on time because this person will be legally responsible for the debt. It is best to prepare all the required documents, such as loan forms, proof of identity, proof of income, employment contracts, bank statements, and others. The forms must be filled up and submitted with the complete documents to the appropriate office. The lender will then look at credit scores, profile, financial history, income, assets, and anything else that is important. People often mix up a co-applicant and a co-signer, but they are different. A co-applicant shares equal responsibility and benefits from getting the loan. On the other hand, a co-signer applies for a loan with the borrower only to help them get approved but does not personally benefit from the loan. A co-signer is only accountable for the loan if the borrower cannot pay, while a co-applicant has equal responsibility for repaying the loan as the borrower. Another difference is that a co-applicant typically has an ownership stake in what is being purchased with the loan, while a co-signer does not. Most companies talk about a co-borrower arrangement when they work with co-applicants. If a title is involved, both of their names are declared. Lenders benefit from either a co-applicant or a co-signer but in slightly different ways. With a co-applicant, two people are responsible for repaying a loan which means more resources are available for repayment. Meanwhile, a co-signer assures the lender of getting their money back if the borrower defaults on the loan. The co-signer acts as a guarantor who will be legally responsible for repaying the debt in case the borrower cannot do so. Below is a table summarizing the key differences between a co-applicant and a co-signer: A co-applicant joins the borrower in applying for a loan, sharing equal responsibility and benefits. Co-applicants strengthen the loan application, especially if they have good financial credentials. Co-applicants are usually family members, spouses, business partners, or anyone else who meets the criteria set by the lender. It is vital to choose a trustworthy co-applicant with a good credit score, a steady income, and an excellent financial history. The benefits of applying for a loan with a co-applicant include easier approval, better loan terms, and possibly increased loan principal. Lenders see lower risk in loans with co-applicants and a higher chance of repayment. It is essential to distinguish between a co-applicant and a co-signer. A co-signer helps the borrower get approved for the loan but is only legally responsible in case of a default on payments. On the other hand, co-applicants are just as accountable for repaying the loan. Borrowers must consider many things before deciding whether or not to apply for a loan with a co-applicant. Generally, it is better to have a co-applicant or a co-signer since it helps lenders look more favorably on the loan application. What Is a Co-Applicant?

How Having a Co-Applicant Works

Who Can Be a Co-Applicant?

Family Members

Spouses

Business Partners

Benefits of Having a Co-Applicant

Increased Chance of Approval

Better Loan Terms

Higher Loanable Amount

What to Look For in a Co-Applicant

Good Credit

Strong Financial Credentials

Trustworthy

How to Apply for a Loan With a Co-Applicant

Co-applicant vs Co-Signer

The Bottom Line

Co-Applicant FAQs

Every lender has different requirements for whom they will accept as a co-applicant. Generally, they prefer eligible co-applicants who have good credit scores, a steady income, and an excellent financial history.

There are many benefits of having a co-applicant when applying for a loan. The most obvious benefit is that it increases the chances of getting approved for the loan because lenders see the presence of a co-applicant as lowering the risk involved.

A co-applicant needs good credit, a steady income, and an excellent financial history.

Having a co-applicant can increase your likelihood of getting approved for a loan if your co-applicant has good credit. However, it can also hurt your chances if they have bad credit. You might have to pay a higher interest rate or be denied the loan altogether.

Co-applicants are not necessarily the same as co-owners. A co-applicant joins the borrower in applying for a loan, sharing equal responsibility and benefits. Meanwhile, a co-owner shares legal rights to a piece of property with another person or group. Depending on the purpose of the loan, co-owners may also be required to be co-applicants. A typical example is when a couple applies for a home loan.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.