Fannie Mae, a government-sponsored entity, plays a pivotal role in the U.S. mortgage industry. One area of rigorous scrutiny by Fannie Mae concerns "large deposits" in a borrower's bank account. Typically, these are substantial sums of money, inconsistent with the borrower's regular income, that appear within 60 days of a loan application. The emphasis on examining such deposits stems from the need to ensure that borrowers aren't acquiring undisclosed debts or obligations that could compromise their ability to repay a mortgage. To address this, borrowers are often required to provide a paper trail, including bank statements, pay stubs, or letters of explanation. By understanding and adhering to Fannie Mae's guidelines on large deposits, borrowers can streamline their mortgage application process, ensuring transparency and building trust with lenders. Like detectives searching for clues, lenders scour through financial documents to trace the origins of every significant sum. A clear paper trail not only establishes the legitimacy of the funds but also helps in speeding up the loan approval process. Meticulous documentation is the cornerstone of simplifying the loan approval process. Acceptable documents include Bank Statements: A clear record of inflows and outflows over a specific period is essential. Highlighting the sources of large deposits can be instrumental. Letters of Explanation: Sometimes, a simple letter can elucidate the origin of funds, especially if they're gifts or inheritances. This letter typically needs to be from the person providing the funds. Pay Stubs, Inheritance Letters, Etc: Proof of additional income, be it from bonuses, inheritances, or any other legitimate source, can simplify the process of loan approval. Typically, the verification of large deposits should be done within the 60 days preceding the loan application. However, delays can occur if the documentation is incomplete or unclear. Delays in Loan Approval: As the adage goes, time is money. In the mortgage world, delays in verifying large deposits can push back loan approvals, affecting the borrower's home-buying plans. Ineligibility for Loan Approval: Unexplained large deposits can result in an outright loan denial. Lenders might perceive them as undisclosed debts, making the borrower a risky proposition. Additional Scrutiny and the Need for More Extensive Documentation: Large deposits often invite additional layers of scrutiny. Borrowers might have to furnish more extensive documentation or details to pacify wary lenders. Deposits that appear as regular inflows, such as monthly salary credits or annual tax refunds, are typically considered routine and are unlikely to undergo stringent scrutiny. This is because these funds are often consistent with a borrower's documented income, thus raising fewer questions about their origin. Lenders usually recognize these transactions as genuine and not as an attempt to artificially inflate one's account balance. Hence, while approaching a loan application, borrowers can feel more at ease with these kinds of deposits in their statements. When it comes to shifting funds between personal accounts, like moving money from checking to savings or vice versa, such transfers are generally deemed innocuous. However, it's essential for borrowers to ensure that the entire sequence of these transfers remains transparent. This means that when viewing account statements, a lender should be able to effortlessly trace funds as they move from one account to another. While receiving monetary gifts from close family members or associates is not uncommon, it's pivotal that such transactions are thoroughly documented. Proper paperwork, which distinctly states the nature of the transaction as a gift, can offer lenders the required assurance. Equally important is the acknowledgment that these funds are indeed gifts and not loans. The lender must be certain that there's no obligation, implied or explicit, for the borrower to repay these funds. Having clear documentation not only simplifies the loan approval journey but also fortifies the borrower's credibility. Informed borrowers are easier to deal with. Lenders, and brokers should take the initiative to educate potential clients about the nuances of large deposit rules. Lenders plays a pivotal role in verifying the legitimacy of large deposits. Ensuring thorough checks can prevent potential defaults in the future. While scrutinizing large deposits safeguards lenders, it also adds to their workload. Balancing between due diligence and efficient customer service can be challenging. Similar to Fannie Mae, Freddie Mac also has stringent checks in place. However, the exact protocols and thresholds might differ. While the core principle remains the same across agencies, each has its own set of rules. FHA loans, for instance, might have different documentation requirements or thresholds for what constitutes a large deposit. Navigating the nuances of Fannie Mae's guidelines on large deposits is crucial for both borrowers and lenders in the U.S. mortgage industry. Such deposits, inconsistent with a borrower's regular income within the span of 60 days from a loan application, require meticulous documentation to establish their legitimacy. This is paramount in ensuring borrowers aren't burdened with undisclosed debts that might hinder their repayment abilities. Whether it's regular inflows like salaries, transfers between personal accounts, or documented monetary gifts, transparency and thorough paperwork are indispensable. Moreover, while Fannie Mae sets specific standards, other agencies such as Freddie Mac or FHA maintain their own unique guidelines, emphasizing the importance of understanding each one. As the mortgage landscape evolves, being well-informed about these guidelines not only streamlines the loan application process but also fosters a transparent and trustworthy relationship between borrowers and lenders.Fannie Mae's Large Deposit Overview

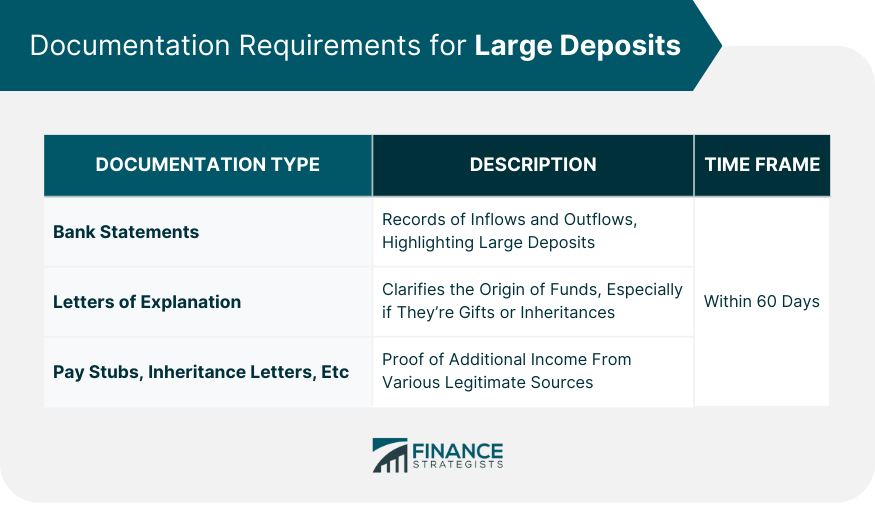

Documentation Requirements for Large Deposits

Need for Paper Trails

Types of Acceptable Documentation

Time Frame for Document Verification

Potential Challenges With Large Deposits

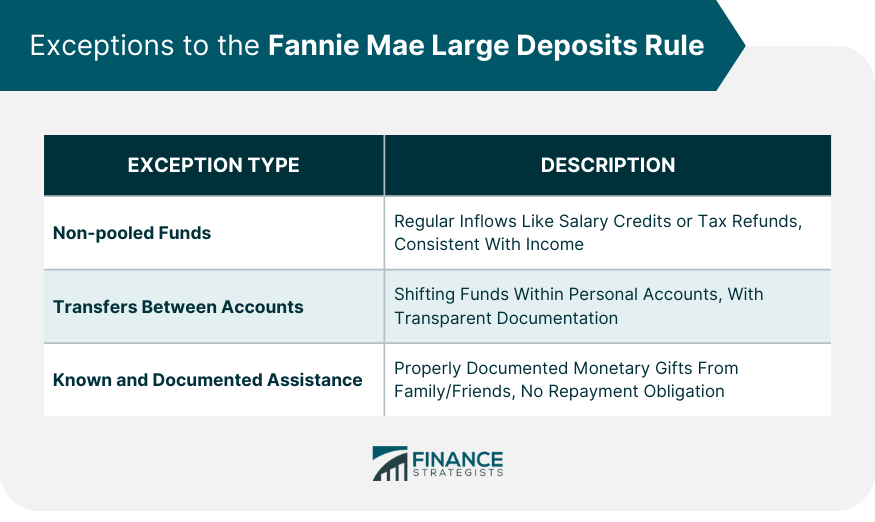

Exceptions to the Fannie Mae Large Deposit Rule

Non-pooled Funds

Transfers Between the Borrower's Own Accounts

Known and Documented Assistance

Fannie Mae Large Deposits Impact on Mortgage Lenders and Brokers

Importance of Educating Borrowers

Role of Lenders in Document Verification

Challenges Faced by Lenders

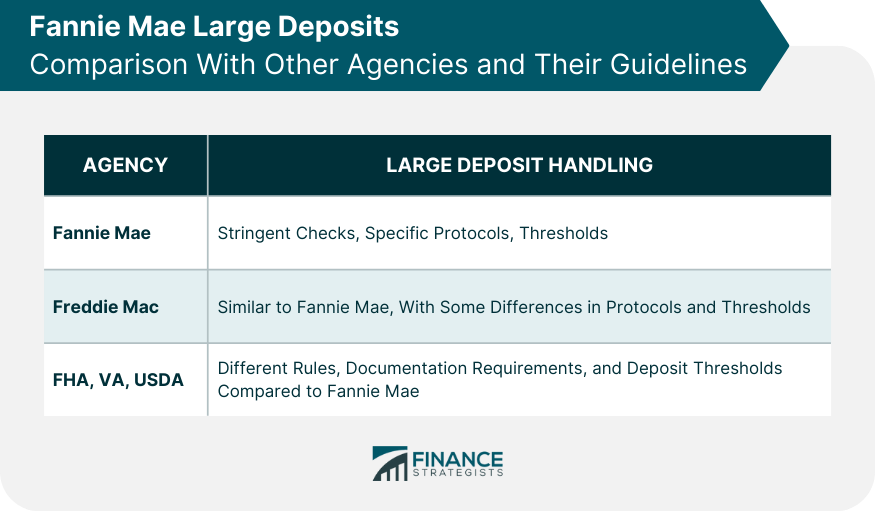

Fannie Mae Large Deposits Comparison With Other Agencies and Their Guidelines

How Freddie Mac Handles Large Deposits

Differences With FHA, VA, and USDA Loan Requirements

Final Thoughts

Fannie Mae Large Deposits FAQs

A "large deposit" refers to any substantial sum of money added to a borrower's bank account within a specific period, typically 60 days of the loan application. The exact amount can vary, but it's typically an amount that's inconsistent with the borrower's regular income patterns.

Explaining the source ensures that the borrower isn't taking on undisclosed debts that might affect their ability to repay the mortgage. Clear explanations help establish creditworthiness and genuine capability to handle the loan.

No, transfers between a borrower's own accounts, such as between checking and savings, are generally exempt from the scrutiny of large deposit rules. However, it's essential that the complete transfer trail be visible to the lender.

Borrowers can ensure that their bank statements are free of unexplained large deposits for at least 60 days before applying. They should also keep documentation handy, like pay stubs, inheritance letters, or letters of explanation, to quickly address any lender concerns.

Yes, similar agencies also have guidelines concerning large deposits. While the core principle of verifying significant inflows remains consistent, each agency might have its own specific protocols, thresholds, and documentation requirements.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.