What is the Fannie Mae Late Mortgage Payment?

A Fannie Mae late mortgage payment arises when a homeowner misses or delays their mortgage payment due to Fannie Mae beyond the established due date.

Typically, borrowers have a brief grace period to make this payment without penalties. However, if payments aren't made within this window, it can lead to late fees, increased interest accumulation, and potential reporting to credit bureaus.

Over time, consistent late payments can risk loan default, affecting the homeowner's credit health and, in extreme cases, leading to foreclosure.

It's essential for borrowers to be aware of these implications and communicate proactively with their lenders if they anticipate payment difficulties.

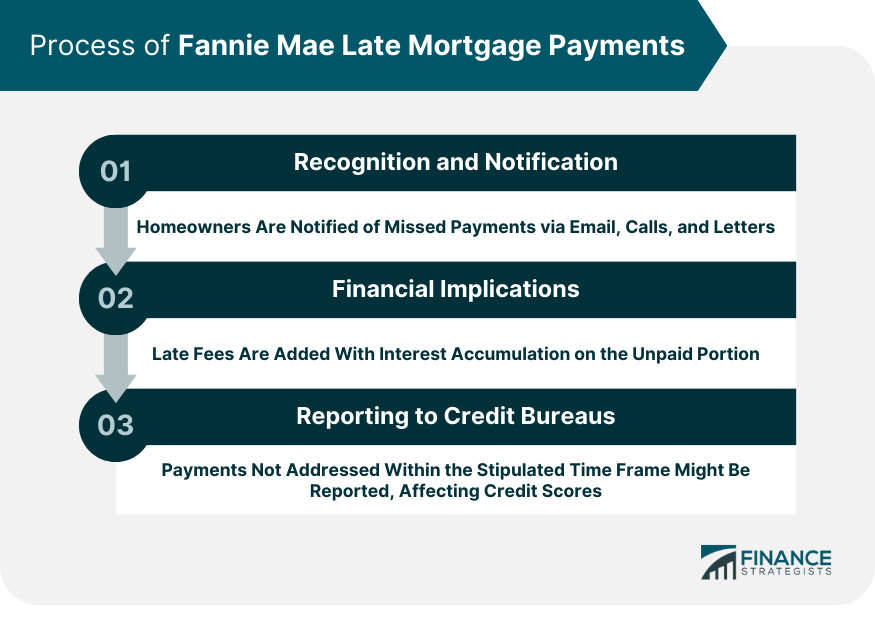

Process of Fannie Mae Late Mortgage Payments

When a mortgage payment is not received by the expected due date, certain actions are set into motion:

Recognition and Notification

Once Fannie Mae realizes a payment is late, the organization initiates a communication process. Homeowners are usually notified via email, phone calls, or mailed letters about the missed payment.

These reminders serve as a nudge to the borrower and also clarify any potential next steps or consequences.

Financial Implications

Missed payments aren't just about a sum going unpaid. Late fees are typically added to the owed amount. Additionally, interest may accumulate on the unpaid portion, adding to the borrower's financial burden.

Reporting to Credit Bureaus

If the payment isn't made within a stipulated time frame, Fannie Mae might report the missed payment to credit bureaus. This can have severe implications for the borrower's credit score, making future financial transactions more challenging.

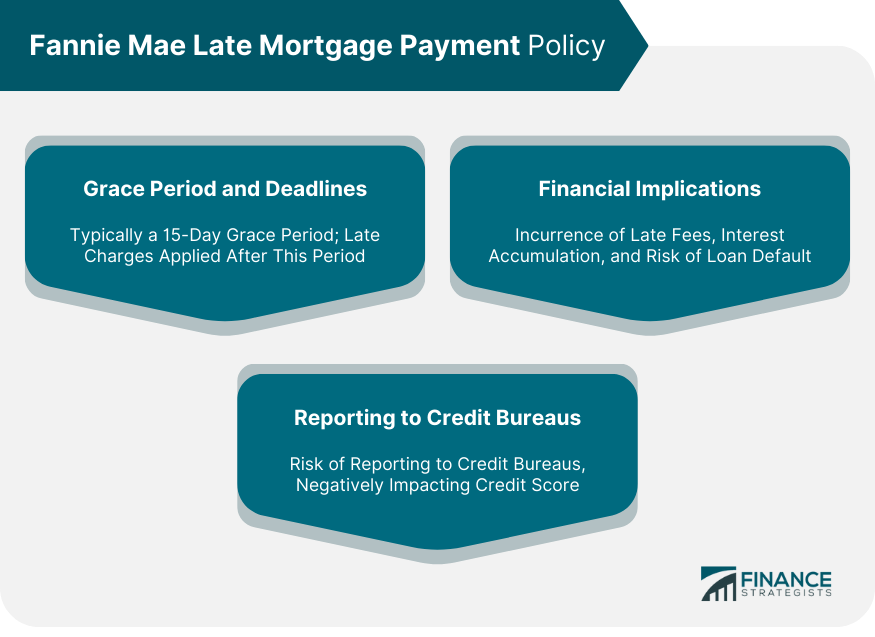

Fannie Mae Late Mortgage Payment Policy

Grace Period and Deadlines

Like many financial institutions, Fannie Mae typically offers a grace period for mortgage payments.

Usually, borrowers have a 15-day grace period from the due date to make their payment without incurring any late fees. However, any payments made beyond this grace period can result in late charges and potential impacts on one's credit report.

Financial Implications

A missed payment isn't merely about a delay. If not addressed in time:

Late fees will be added to the outstanding amount.

Interest continues to accumulate on the unpaid sum.

Potential risk for loan default increases, leading to more severe consequences.

Reporting to Credit Bureaus

Continued failure to address a late mortgage payment can lead Fannie Mae to report the delinquency to credit bureaus. This action can significantly affect a borrower's credit score, making it difficult to secure loans in the future or face higher interest rates.

Assistance for Borrowers

Understanding the challenges homeowners can face, Fannie Mae has instituted policies to assist struggling borrowers. Before resorting to foreclosure, Fannie Mae's policy typically involves:

Offering forbearance options, allowing borrowers to reduce or suspend payments for a specified period.

Presenting loan modification opportunities to make mortgage payments more manageable.

Encouraging borrowers to seek housing counseling to better navigate their financial challenges.

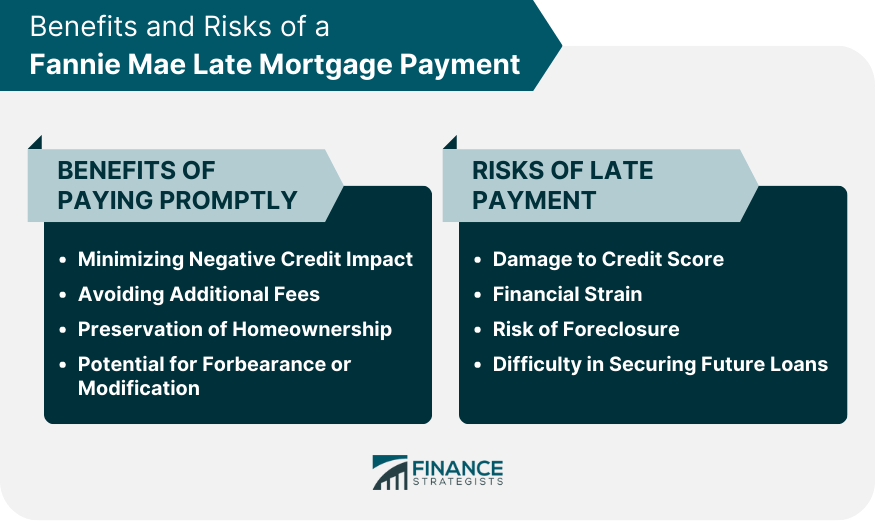

Benefits of Addressing a Late Mortgage Payment Promptly

Addressing a late payment isn't merely about avoiding penalties. There are tangible benefits to resolving such issues promptly:

Minimize Negative Credit Impact

A timely resolution ensures that the credit score remains relatively unaffected. Immediate action can sometimes prevent the late payment from being reported to credit bureaus.

Avoid Additional Fees

The sooner the payment is made, the fewer fees accumulate. This can mean significant savings, especially in scenarios where multiple payments have been missed.

Preservation of Homeownership

Rights Making the payment quickly can halt any potential acceleration toward more severe actions, such as foreclosure.

Potential for Forbearance or Modification

Lenders, including Fannie Mae, can sometimes offer forbearance or loan modification options to borrowers facing genuine financial hardships. Acting promptly can open the door to these options.

Risks of a Fannie Mae Late Mortgage Payment

Late mortgage payments can lead to several challenges:

Damage to Credit Score

A marked decrease in credit score can have long-term implications. It affects not just mortgage transactions, but any future loans, credit cards, or financial agreements.

Financial Strain

With accumulating late fees and compounded interest, the financial burden can grow exponentially over time.

Risk of Foreclosure

Perhaps the most severe consequence of continued missed payments is the risk of foreclosure. This not only means losing the home but also further damaging the credit score.

Difficulty in Securing Future Loans

Lenders view late payments unfavorably. Borrowers with such marks on their record might find it challenging to secure loans in the future or might face higher interest rates.

Impact of Fannie Mae Late Mortgage Payment Policy

Personal Financial Health

When homeowners miss a payment:

Credit Score Deterioration: Fannie Mae can report delinquencies to credit bureaus. This negative mark can significantly lower a borrower's credit score, affecting their ability to obtain future credit at favorable terms.

Accumulating Costs: Late payments bring late fees. Over time, these additional costs, combined with accruing interest, can significantly increase the financial burden on homeowners.

Housing Market Stability

The ripple effects of many homeowners defaulting on their mortgages can be vast:

Increased Foreclosures: Without the policy's guidelines and protective measures, there would likely be a surge in foreclosures. This not only displaces families but can also depress local real estate values.

Lender Reluctance: If lenders believe they won't be repaid, they may become more reluctant to issue new mortgages. This can lead to reduced housing market liquidity, making it harder for potential homeowners to secure loans.

Economic Implications

The broader economy can also feel the effects:

Consumer Spending: With a dip in credit health and increased financial burdens, consumers might cut back on spending. This reduction can, in turn, affect various sectors of the economy.

Financial Institutions: Banks and other lenders could face financial strains if significant numbers of borrowers default on their loans. This can result in reduced lending activity or even potential bank failures in extreme cases.

Protective Measures and Support

Fortunately, Fannie Mae's policy isn't just about penalization. They also offer:

Forbearance and Modification: These tools can help borrowers navigate temporary hardships, ensuring they don't spiral into insurmountable debt.

Housing Counseling: By guiding homeowners through their challenges, Fannie Mae aids in making informed decisions to protect their homes and financial futures.

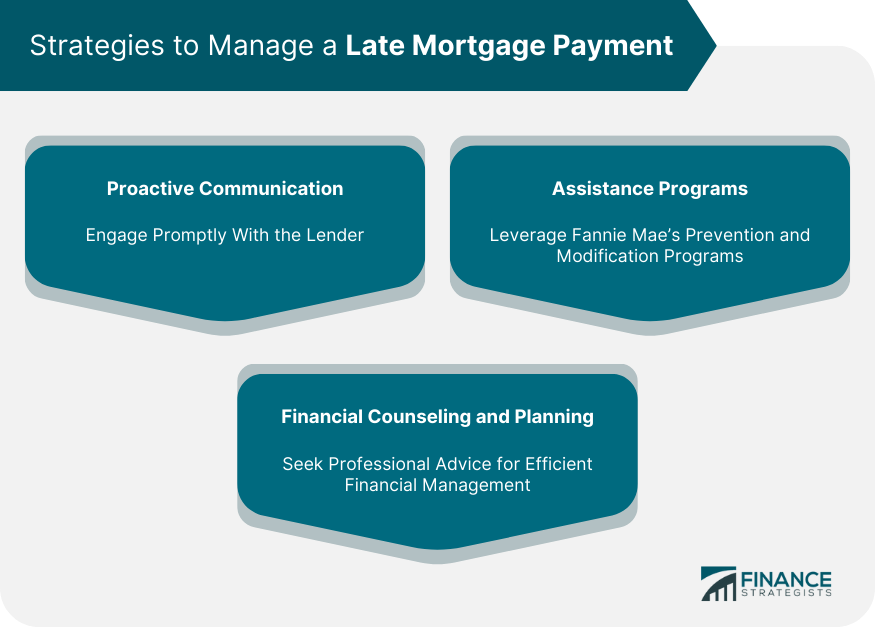

Strategies to Manage a Late Mortgage Payment

If you find yourself in a situation with a late mortgage payment, here are some strategies:

Proactive Communication

Engage with the lender as soon as you realize a payment has been missed. This shows responsibility and can sometimes lead to leniency or alternative payment options.

Assistance Programs

Fannie Mae offers programs like foreclosure prevention and loan modification to assist borrowers. Explore these options if you're facing genuine financial hardships.

Financial Counseling and Planning

Consider seeking professional financial advice. Experts can provide insights into managing debts, creating a sustainable budget, and navigating complex mortgage scenarios.

Conclusion

The Fannie Mae Late Mortgage Payment Policy safeguards the intricate balance between lenders and borrowers within the U.S. housing finance system.

With its structured approach, Fannie Mae not only ensures timely mortgage repayments but also offers support mechanisms like forbearance and loan modification.

The impact of late payments spans personal financial health, housing market stability, and broader economic implications. Such delinquencies can tarnish credit scores, result in additional financial burdens, and even pose risks to homeownership.

However, Fannie Mae's commitment to assisting borrowers shines through its varied assistance programs and proactive communication channels.

As borrowers navigate the complex realm of mortgages, understanding these policies and the importance of timely repayments becomes paramount.

Fannie Mae Late Mortgage Payment FAQs

A Fannie Mae Late Mortgage Payment occurs when a homeowner misses or delays their mortgage payment to Fannie Mae beyond the due date. This can result in late fees, increased interest, and potential reporting to credit bureaus if not addressed promptly.

The process initiates with recognition and notification. When Fannie Mae identifies a missed payment, homeowners are alerted through email, phone calls, or letters. If unresolved, financial implications like late fees and interest accumulate. Extended delays may lead to reporting to credit bureaus, affecting credit scores.

Yes, Fannie Mae offers assistance for struggling borrowers. This includes forbearance options to reduce or suspend payments temporarily, loan modification to make payments more manageable, and housing counseling to help navigate financial challenges.

Multiple late payments amplify the risks, including significant damage to credit scores, accumulating late fees and interest, increased risk of loan default, and ultimately the threat of foreclosure. It also makes securing future loans more challenging or could result in higher interest rates.

Proactive communication is key. Engage with your lender as soon as you recognize an issue. Explore Fannie Mae's assistance programs, and consider seeking professional financial counseling and planning for better management of your mortgage.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.