The Fannie Mae Senior Housing Loan is a specialized financing solution crafted for developers and investors in the senior housing sector. Operating under the Fannie Mae umbrella, this loan addresses the distinct needs of housing projects designed for seniors, ranging from independent living and assisted living facilities to memory care and continuing care retirement communities. Tailored to ensure the safety, accessibility, and overall well-being of elderly residents, it provides borrowers with competitive interest rates and flexible terms. For those venturing into the development or refurbishment of senior housing establishments, the Fannie Mae Senior Housing Loan emerges as a pivotal financial cornerstone, underpinning the sector's growth and ensuring senior citizens have quality living spaces. This housing type is designed for seniors who value their independence and require minimal assistance. The focus here is on creating an environment where seniors can live freely, engage in recreational activities, and have access to amenities like fitness centers, communal spaces, and more. Assisted living facilities combine housing, support services, and health care as required. They are tailored for seniors who may need help with daily activities such as bathing, dressing, and medication management. On-site medical care and professional staff ensure that residents are well taken care of. Memory care facilities offer specialized housing for seniors dealing with memory challenges, typically those with conditions like dementia or Alzheimer's. These facilities are equipped with advanced safety features, therapeutic activities, and trained staff to provide round-the-clock care and supervision. CCRCs are comprehensive senior care facilities that provide a full spectrum of care, from independent living to assisted living and even nursing home care, all on a single campus. This approach ensures that as residents age and their needs change, they can transition to the appropriate level of care without having to relocate. Before granting any loan, lenders prioritize evaluating the borrower's financial health. This includes examining liquidity, debt-to-income ratios, and overall financial stability. A strong financial position indicates not only the borrower's ability to repay the loan but also their capacity to handle unforeseen challenges that might arise during the project. Credit history acts as a report card of an individual's or organization's borrowing behavior. Fannie Mae reviews credit scores, past loan repayments, and any instances of defaults or bankruptcies. A positive credit history instills confidence in the lender about the borrower's commitment to repaying the loan. Given the specialized nature of senior housing, having prior experience in developing or managing similar projects is vital. Lenders look for borrowers with a demonstrated history of successfully completing projects, ensuring they have the expertise to meet the unique demands of senior housing. The journey begins with an in-depth application, where borrowers detail the specifics of the proposed project. This includes project plans, cost estimates, timelines, and the borrower's credentials. Clear, well-documented, and structured information helps set the tone for the subsequent stages. Once the application is received, the Fannie Mae team conducts a detailed review. This includes evaluating the feasibility of the project, the borrower's qualifications, and alignment with the senior housing vision. Every aspect of the application is scrutinized to ensure its viability and the borrower's capability. After the initial vetting, a meticulous due diligence process is initiated. This involves third-party property inspections, appraisals, and evaluations. Such comprehensive checks are paramount to ascertain the real-time value of the property and ensure that it aligns with the details provided in the application. Once all checks are cleared and the project meets the set standards, the loan is finally disbursed. This marks the green signal for borrowers to commence or continue with their project, armed with the financial support they need. When benchmarked against conventional loan options, the Fannie Mae Senior Housing Loan often emerges as a more economical choice, thanks to its competitive interest rates. The loan's allure can be attributed to the government's backing, allowing borrowers to avail of lower interest rates than many traditional financing avenues. Beyond interest rates, the loan's design addresses the unique challenges of senior housing developments. This includes aspects like phased disbursements aligned with construction timelines and flexible repayment structures. The loan prioritizes amenities crucial for seniors, such as ramps, elevators, emergency medical facilities, and recreational areas, ensuring that the senior communities built are not just houses, but homes. Given the government backing and the sector's specialized nature, the bar is set incredibly high, sometimes posing challenges for smaller or less-experienced investors. Smaller developers or first-time investors in the senior housing segment might find the criteria daunting, often necessitating partnerships or additional measures to qualify. While flexible, the loan might have penalties if borrowers decide to pay off their debts ahead of the scheduled timelines, impacting financial planning. Prepayment penalties can deter borrowers from capitalizing on favorable market conditions or adjusting to new financial realities. The requirement for comprehensive third-party reports, while ensuring thoroughness, can be time-consuming and expensive for borrowers. These due diligence steps, while ensuring the project's viability, might extend timelines and elevate costs. Unlike standard multifamily loans, there's a heightened focus on designs that prioritize senior safety, accessibility, and comfort. These loans recognize the varied requirements of seniors, from social engagement needs to healthcare, and ensure these are core to the financed projects. Given the specialized nature, projects financed might command higher rent or enjoy better occupancy rates due to the targeted amenities and features. While initial costs might be higher, the long-term ROI, when considering rent premiums and sustained occupancy, paints a favorable picture for borrowers. The Fannie Mae Senior Housing Loan stands out as a specialized financing beacon tailored for the senior housing sector, addressing the nuances of elderly residential needs. With its competitive interest rates and flexible terms, it underscores the importance of creating safe, accessible, and quality living spaces for seniors. The loan caters to diverse senior housing models, from independent living to more comprehensive care facilities. However, potential borrowers must navigate its stringent eligibility criteria, balancing the advantages against potential challenges like prepayment penalties and in-depth due diligence requirements. In essence, while the loan offers a pathway for the development of high-quality senior communities, it demands thorough preparation and understanding from its applicants. This meticulous approach, though demanding, ensures that senior housing financed under this framework truly epitomizes care, comfort, and dignity for its residents.What Is Fannie Mae Senior Housing Loan?

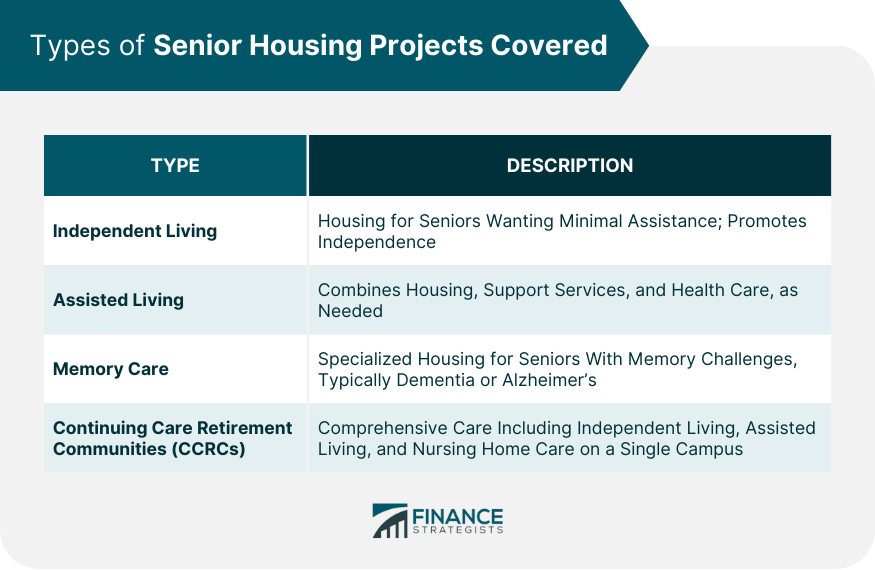

Types of Senior Housing Projects Covered

Independent Living

Assisted Living

Memory Care

Continuing Care Retirement Communities (CCRCs)

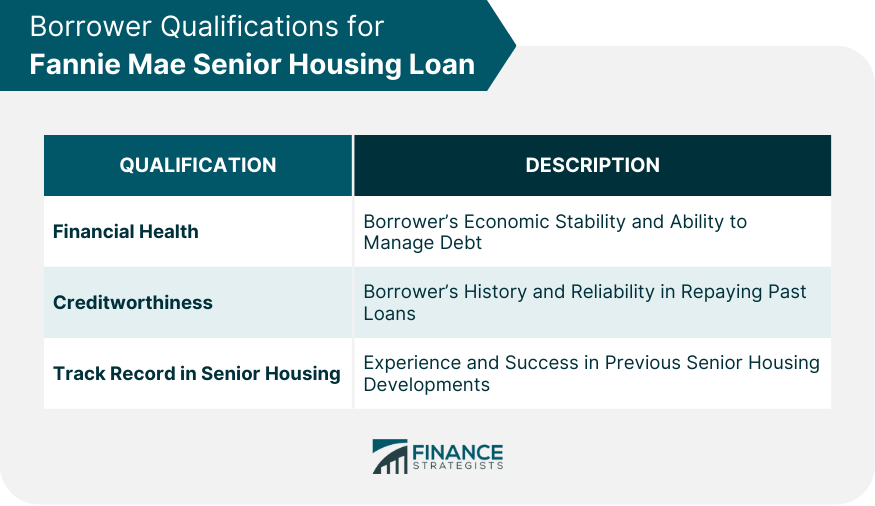

Borrower Qualifications for Fannie Mae Senior Housing Loan

Financial Health

Creditworthiness

Proven Track Record in Senior Housing

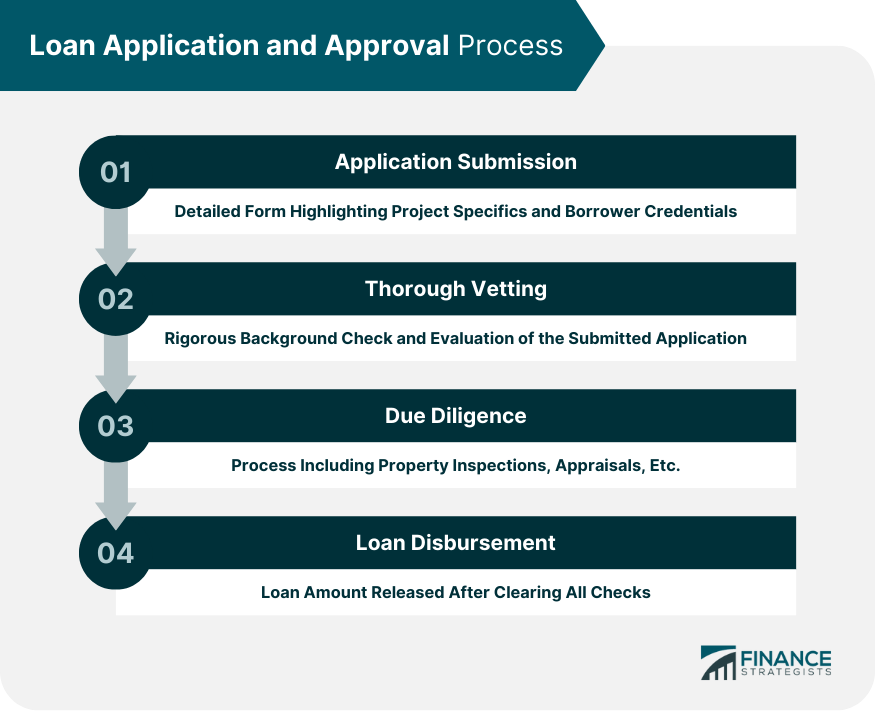

Loan Application and Approval Process

Comprehensive Application

Thorough Vetting Phase

Due Diligence Process

Loan Disbursement

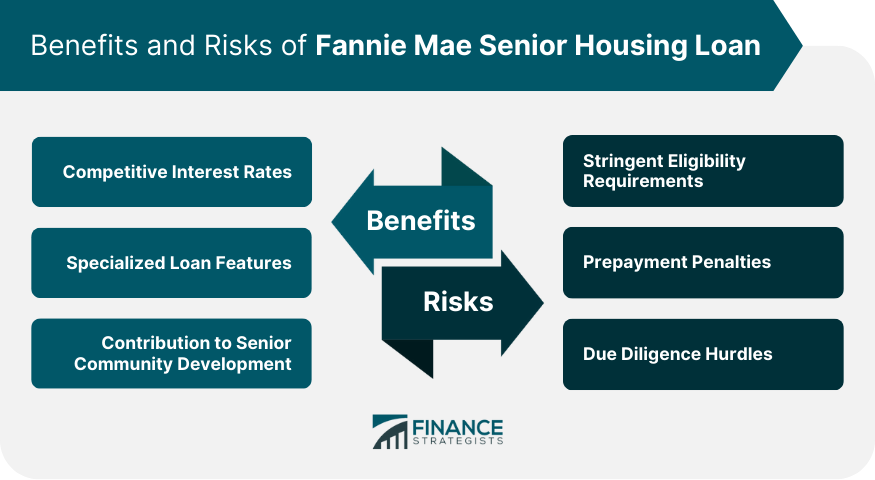

Benefits of Fannie Mae Senior Housing Loan

Competitive Interest Rates

Specialized Loan Features

Contribution to Senior Community Development

Risks of Fannie Mae Senior Housing Loan

Stringent Eligibility Requirements

Prepayment Penalties

Due Diligence Hurdles

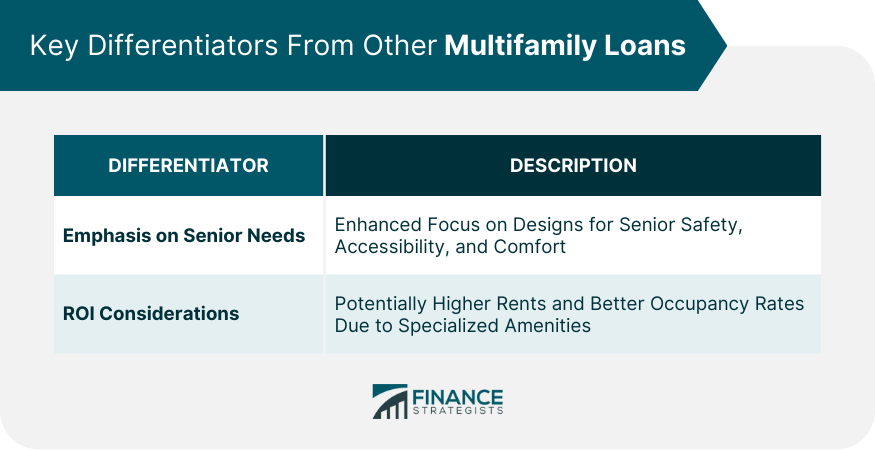

Key Differentiators From Other Multifamily Loans

Special Emphasis on Senior Needs

Return on Investment (ROI) Considerations

Conclusion

Fannie Mae Senior Housing Loan FAQs

The Fannie Mae Senior Housing Loan is specifically designed to finance senior housing projects, which cater to the unique needs and requirements of elderly residents.

The Fannie Mae Senior Housing Loan places a special emphasis on senior needs, with heightened focus on safety, accessibility, and amenities tailored for the elderly, distinguishing it from standard multifamily loans.

Yes, borrowers must meet stringent criteria including financial health, creditworthiness, and a proven track record in senior housing developments to qualify for the Fannie Mae Senior Housing Loan.

The loan covers a variety of senior housing types, including independent living, assisted living, memory care, and continuing care retirement communities, ensuring a comprehensive range of senior needs are addressed.

While the loan offers many benefits, it comes with stringent eligibility requirements, potential prepayment penalties, and extensive due diligence processes that can be challenging for some borrowers.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.