Fannie Mae, or the Federal National Mortgage Association, has been at the forefront of the American housing market for decades. When financial hardships arise, homeowners often find themselves unable to keep up with their mortgage payments. In such instances, Fannie Mae's short sale process becomes an invaluable option. It allows homeowners to sell their property for less than the outstanding mortgage balance, averting a possible foreclosure. The housing market is an ecosystem that thrives on stability. The short sale process, pioneered by institutions like Fannie Mae, ensures that a wave of foreclosures doesn’t destabilize this delicate balance. By providing homeowners with an exit strategy that minimizes financial and credit damages, Fannie Mae's short sale framework significantly contributes to the overall health of the housing market, benefiting lenders, buyers, and the economy at large. The real estate commission is a charge that sellers frequently encounter, acting as compensation for the agents. It represents the fee paid to real estate agents in recognition of their services in marketing, listing, and selling the property. The commission ensures agents are rewarded for their role in the complex world of property transactions, making the sale process smoother for both buyers and sellers. When dealing with short sales, negotiation is paramount. The negotiation fee covers the intricate process of bridging the gap between buyer's offers and the lender's expectations, ensuring a successful transaction. This fee is crucial, as short sales often involve multiple parties with conflicting interests, requiring expert negotiation skills to come to a mutual agreement. Sellers are responsible for any property taxes due up to the date of the sale. Prorated real estate taxes reflect this obligation, ensuring sellers don't carry over tax liabilities after selling their homes. This mechanism prevents the new homeowner from bearing the previous owner's tax burdens and ensures a clean financial slate post-sale. To formalize the transfer of property ownership, local and state governments often impose certain taxes and stamps. These charges, which sellers typically bear, ensure all legal requisites for ownership transfer are met. They act as a government's acknowledgment of the transaction, adding a layer of legitimacy and protection to both the buyer and seller. To guarantee the buyer receives a clean title free from any encumbrances, sellers often tackle title and settlement charges. This process, which involves thorough legal checks, removes potential disputes over property ownership. By clearing these charges, sellers assure buyers that they are acquiring a property without hidden legal complications. Homeowners' associations (HOAs) impose certain dues for the upkeep of common areas and community amenities. If there are overdue HOA fees at the time of sale, sellers are obliged to clear them. Settling these fees ensures the community's continued maintenance and avoids passing on financial burdens to the new homeowner. On occasion, unique circumstances may arise that necessitate additional costs. Fannie Mae, exercising discretion, can approve these specific amounts on a case-by-case basis. Such flexibility ensures that unforeseen costs or unique situations don't stall the short sale process. Fannie Mae discourages costs that deviate from standard practices. As such, fees charged for outsourcing services or those presented by non-traditional third parties aren't permissible. These types of fees can inflate the overall cost of the transaction without adding direct value to the primary stakeholders. Commissions intended for borrowers or purchasers are strictly prohibited in the short sale realm. Such arrangements could distort the short sale process and aren't conducive to a transparent, unbiased transaction. These commissions can also confuse the financial dynamics of the deal, leading to potential misunderstandings. Any fees linked with initiating the buyer's loan or related to discount points aren't permissible in short sale costs. The rationale is that these expenses directly relate to the buyer's mortgage arrangements and shouldn't affect the short sale's net proceeds. They are typically settled directly between the buyer and their lender. Fees that aren't customary within the local property market are flagged as prohibited. Consistency with market norms ensures fairness in transactions. This guideline protects sellers from potential predatory practices and guarantees that both parties deal within established market norms. For properties on the market, it's vital to consolidate all pertinent details about the real estate agent. This includes their contact information, licensing details, and track record in handling similar sales. Equipped with this information, sellers can ensure they're partnering with competent professionals in the short sale journey. Real estate agents should be thoroughly familiar with the intricacies of short sales. Proper training or orientation allows them to guide homeowners and potential buyers more effectively. This clarity ensures a more streamlined process and fewer hiccups along the way. For homeowners new to the short sale process, locating a qualified real estate agent can be a daunting task. Providing assistance in this endeavor ensures that sellers have expert guidance throughout. Engaging a skilled agent can make the difference between a successful short sale and a drawn-out, unsuccessful one. Setting the right list price is pivotal to a successful short sale. Expert guidance ensures the property is priced competitively, attracting potential buyers while reflecting its true market value. A well-priced property tends to move faster in the market, reducing financial stress for the homeowner. Agents involved in short sales must hold valid licenses to operate in their respective states. This certification ensures they've met specific professional standards and are qualified to undertake such transactions. A licensed agent also offers homeowners the assurance of professionalism and accountability. For the sake of transparency, properties should maintain an active status on major listing platforms. This active status should persist for at least five consecutive days, offering potential buyers a reasonable window to discover and consider the property. It ensures a level playing field for all interested parties. Once a short sale is approved, it's crucial to move towards closing the deal within 60 calendar days. This swift progression ensures all stakeholders can transition to their next steps without unnecessary delays. It also offers the seller a sense of relief, knowing they've successfully navigated the challenging process. While the goal is a swift closure, unique circumstances might demand additional time. In such cases, Fannie Mae has the provision to grant extensions. This flexibility is designed to cater to unforeseen challenges or complications, ensuring all parties are given ample time to finalize details without feeling rushed. Engaging with mortgage insurers is pivotal when processing a Fannie Mae short sale. The servicer should be aware of the insurers with whom Fannie Mae has a delegation of authority. Such a setup would mean that the servicer can process the short sale in tandem with this guide, without the need for individual mortgage insurer approvals. In cases where no delegation from the mortgage insurer exists, the servicer's task increases manifold. They must liaise with the insurer, discuss the short sale's feasibility, and ensure that the insurer’s written agreement aligns with specific conditions. This agreement should emphasize waiving property acquisition rights pre-claim and settling the claim to satisfy both the master policy’s full percentage option and Fannie Mae's interests. Claims are an integral part of the mortgage ecosystem. For all conventional first lien mortgage loans where Fannie Mae bears the risk, the servicer must file a primary MI claim, with a few exceptions. It’s a procedure that demands attention to detail, ensuring that all the i's are dotted and t's crossed. While much is discussed about the lender's role, the borrower too has responsibilities. They must ensure that they're transparent about their financial situation, cooperate in listing the property, and engage proactively throughout the short sale process. Their cooperation is the backbone that ensures the procedure proceeds without hitches. Fannie Mae, on the other hand, operates with a clear goal: to ensure borrowers can navigate financial hardships with dignity. While facilitating short sales, they aim for transparency, timely communication, and a fair evaluation of each case. Their obligations extend towards a fair treatment, guiding borrowers towards an optimal resolution. A short sale does carry implications. One such repercussion revolves around the borrower's credit score. While it's a gentler hit compared to a foreclosure, there is an impact. It's a notch on the credit report, indicating that the borrower sold their property for less than what was due. Borrowers should be aware of this and potentially work with credit experts to map a recovery journey. Fannie Mae, central to the American housing market, offers a short sale process as an alternative to foreclosure, thereby maintaining housing market stability. This process allows homeowners facing financial adversities to sell their homes for a price less than their outstanding mortgage. This not only provides an escape route for distressed homeowners but also bolsters the health of the housing sector, benefitting the broader economy. Allowable and non-allowable transaction costs exist in short sales, emphasizing transparency and fairness in dealings. Furthermore, it underscores the importance of competent real estate agents, both for those experienced in short sales and novices. From the initial evaluation to the eventual closure, the short sale journey demands proactive engagement from both servicers and borrowers. While Fannie Mae plays a supportive and transparent role, borrowers must be prepared for the potential credit implications of a short sale. Awareness and guidance are crucial for a smooth, fair transaction.Overview of Fannie Mae Short Sale

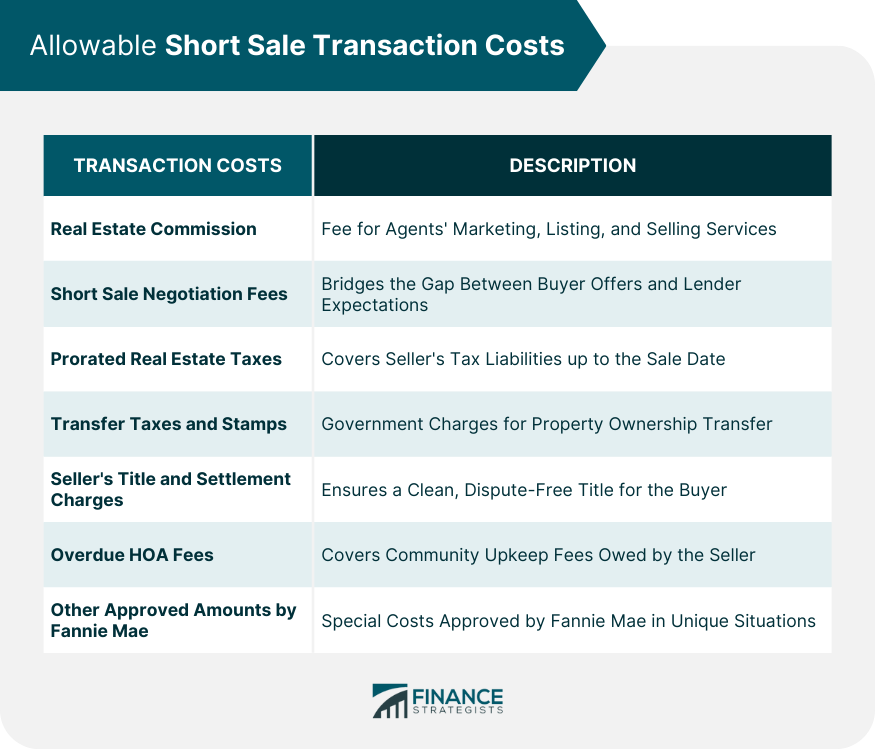

Allowable Short Sale Transaction Costs

Costs Deductible From the Sales Price

Real Estate Commission

Short Sale Negotiation Fees

Prorated Real Estate Taxes

Local and State Transfer Taxes and Stamps

Seller's Title and Settlement Charges

Overdue HOA Fees

Other Approved Amounts by Fannie Mae

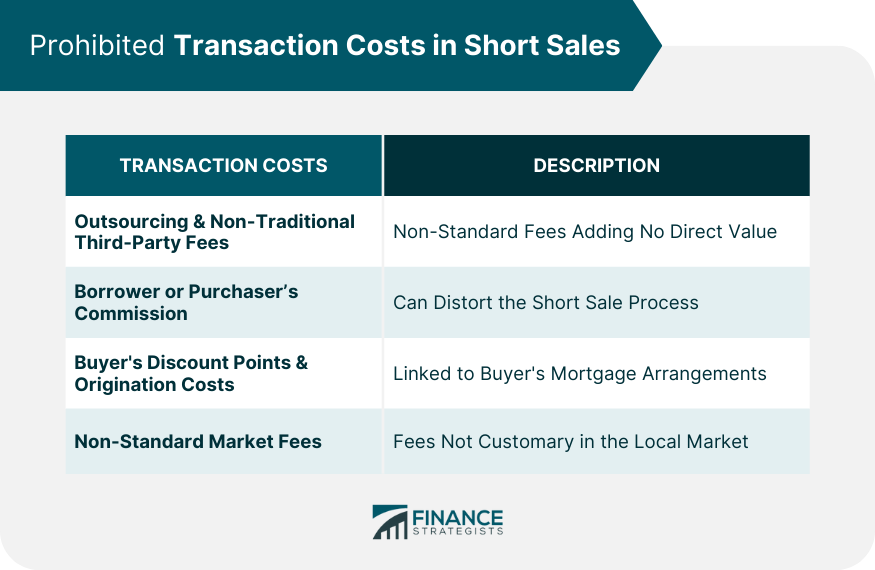

Prohibited Transaction Costs in Short Sales

Non-Allowable Fees and Deductions

Outsourcing Fees and Non-Traditional Third-Party Fees

Borrower or Purchaser’s Commission

Buyer's Discount Points and Origination Costs

Non-Standard Fees for the Market

Listing Procedures and Requirements of Short Sales

Protocols for Properties Already Listed

Gathering Real Estate Agent Details

Introducing the Short Sale Process to Agents

Guidelines for Properties Not Yet Listed

Assisting in Finding Real Estate Agents

Offering List Price Guidance

Essential Notes for Property Listings

Licensing Requirements for Agents

Active Listing Status and Duration

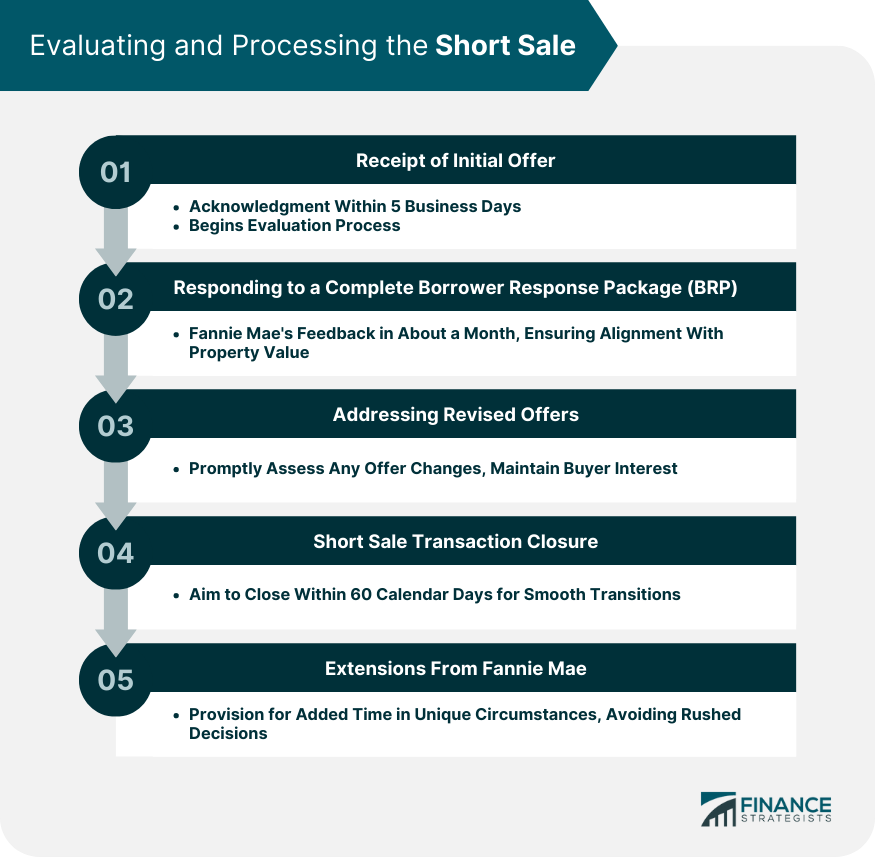

Closure Procedures and Timelines

Short Sale Transaction Closure

Extensions From Fannie Mae

Short Sale Involving Mortgage Insurance

Handling Delegations From Mortgage Insurers

When No Delegation Exists

Filing a Primary MI Claim

Rights and Responsibilities of the Borrower

Borrower's Duties in the Short Sale Process

Fannie Mae's Obligations Towards the Borrower

Possible Impacts on the Borrower’s Credit Score

Bottom Line

Fannie Mae Short Sale FAQs

A Fannie Mae short sale allows homeowners to sell their property for less than the outstanding mortgage balance to avoid foreclosure.

It ensures housing market stability by providing homeowners an option that prevents a surge of foreclosures and supports the overall economic health.

Allowable costs include real estate commission, short sale negotiation fees, prorated real estate taxes, and specific approved amounts by Fannie Mae.

Yes, costs like outsourcing fees, borrower or purchaser’s commission, and non-standard market fees are not allowed.

Yes, while less damaging than a foreclosure, a short sale still impacts the borrower's credit, indicating a sale for less than the owed amount.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.