The Federal National Mortgage Association, colloquially known as Fannie Mae, serves as the cornerstone of the U.S. secondary mortgage market. Established during the New Deal era, its mission was clear: improve liquidity in the mortgage market by purchasing loans from lenders. This process frees up funds, enabling lenders to underwrite more mortgages and facilitate homeownership for Americans. Over time, Fannie Mae evolved, but its core purpose remains: ensuring a stable and affordable housing market. Diving deeper, Fannie Mae doesn’t directly loan to borrowers. Instead, it operates by buying mortgages from banks and other loan originators. This model provides a safety net for these institutions, encouraging them to lend more confidently to prospective homeowners. Guidelines provided by Fannie Mae play an influential role in shaping the mortgage landscape. These standards, while precise, are designed to foster a sense of security for both lenders and borrowers. The front-end DTI ratio, often simply referred to as the housing ratio, provides a snapshot of a borrower's significant housing expenses relative to their gross monthly income. Typically, this ratio encompasses mortgage payments, property taxes, homeowner's insurance, and possibly homeowner's association fees. By assessing this ratio, lenders can gauge the portion of a borrower's income allocated to housing costs. While seemingly straightforward, the front-end DTI remains crucial in the lending world. It acts as an early indicator of a borrower's ability to handle the most pressing and consistent financial obligation they'll likely face: their home payments. Front-end DTI emerges as a pivotal factor during the mortgage approval process. Lenders employ this metric to assess if a borrower can comfortably manage their housing-related expenses. A lower front-end DTI often indicates that a borrower has ample financial wiggle room to address their housing costs, making them a more attractive candidate for a mortgage. Conversely, a high ratio suggests that a significant portion of a borrower's income is tied up in housing expenses. This scenario can raise red flags for lenders, prompting concerns about potential financial strain or default if unforeseen expenses arise. While specific benchmarks might fluctuate between lenders, the industry generally views a front-end DTI of 28% or lower as desirable. This percentage signals that less than a third of a borrower's income is devoted to housing costs. It's worth noting, though, that while 28% is a common benchmark, some lenders are flexible, especially if a borrower exhibits strong credentials in other areas. Such benchmarks aren't arbitrary. Decades of lending data and financial modeling have informed these standards, aiming to strike a balance between lender risk and borrower accessibility. Interestingly, Fannie Mae doesn't explicitly dictate a front-end DTI cap for conventional loans. Their focus tends to gravitate more towards the back-end DTI, which encompasses all of a borrower's monthly debt obligations, not just housing costs. This approach underscores Fannie Mae's holistic view of borrowers financial health, considering the entirety of their debt landscape. Yet, this absence doesn't translate to an oversight or indifference. Rather, it affords lenders the autonomy to set their boundaries, reflecting their risk appetite and specific clientele. Despite the lack of a front-end DTI mandate, Fannie Mae is stringent about the back-end DTI, setting a threshold of 50%. This figure encapsulates all monthly debts, including car loans, student loans, credit card payments, and housing costs. By imposing this limit, Fannie Mae ensures borrowers aren't over-leveraged, preserving the integrity of the loan and safeguarding the broader housing market. This 50% mark stands as a testament to Fannie Mae's commitment to responsible lending. By championing this metric, they push the industry towards practices that prioritize long-term financial stability over short-term gains. In the absence of a direct mandate from Fannie Mae regarding front-end DTI, individual lenders often craft their guidelines. These policies reflect a blend of risk tolerance, market positioning, and past experiences. For instance, a lender with a more conservative stance might set stricter DTI benchmarks to curtail risk, while another might opt for more lenient limits to appeal to a broader client base. The freedom to set front-end DTI standards allows lenders to tailor their offerings, differentiating themselves in a competitive market. It also empowers them to pivot quickly in response to economic shifts or emerging trends. Borrowers with a low front-end DTI are often in an advantageous position. They might secure better interest rates, have smoother approval processes, and access a wider array of loan products. This scenario is largely because they present a reduced risk profile, appearing more likely to manage their housing expenses adeptly. On the flip side, those with a higher DTI might encounter hurdles. They could face higher interest rates, stricter scrutiny, or even outright denial. Yet, it's essential to remember that DTI is just one piece of the puzzle. Other factors, like credit history or savings, can sway a lender's decision. For those looking to bolster their mortgage application, tweaking their front-end DTI can be transformative. Strategies might include paying down existing debts, seeking additional income sources, or choosing a more affordable housing option. By adjusting these levers, borrowers can position themselves more favorably in the eyes of lenders. Additionally, shopping around can be beneficial. Different lenders might have varied DTI requirements, so casting a wide net can unearth more accommodating loan options. While the front-end DTI focuses exclusively on housing expenses, the back-end DTI offers a panoramic view of a borrower's debt landscape. This broader perspective is why entities like Fannie Mae place immense emphasis on it. Capturing all monthly obligations, it provides a more comprehensive snapshot of a borrower's financial health and resilience. From student loans to car payments, the back-end DTI encapsulates these commitments, painting a clearer picture for lenders. It's a testament to the notion that while housing expenses are paramount, they aren't the sole financial responsibilities individuals bear. Mortgage qualification isn't a one-dimensional process hinged solely on DTI. Lenders dive deep, considering aspects like credit scores, which reflect a borrower's creditworthiness, and loan-to-value (LTV) ratios that measure the loan amount against the property's value. These elements, in tandem with DTI, craft a multi-faceted profile of a borrower. For instance, a stellar credit score might offset a slightly higher DTI. Conversely, a low LTV, indicating a substantial down payment, can be a positive signal, even if other metrics are less than perfect. The interplay of these factors underscores the complexity of mortgage qualification, nudging borrowers to optimize across multiple fronts. Navigating the world of mortgage qualification can be intricate, with the front-end Debt-To-Income (DTI) ratio serving as a pivotal marker. As a linchpin of the U.S. secondary mortgage market, Fannie Mae’s influence reverberates throughout the lending landscape. Their holistic view prioritizes back-end DTI, illuminating a borrower's full financial spectrum. This perspective balances housing costs with other financial commitments, echoing the importance of a comprehensive financial profile. Meanwhile, individual lenders tailor their DTI benchmarks based on unique strategies and market insights. As borrowers tread these waters, it's imperative to recognize the mosaic of factors, from credit scores to loan-to-value ratios, shaping their mortgage prospects. Ultimately, understanding these nuances not only empowers borrowers but also sustains a robust and resilient housing market.Fannie Mae's Role in Mortgage Lending

Understanding the Front-End Debt-to-Income Ratio (DTI)

Definition of the Front-End DTI Ratio

How Front-End DTI Affects Mortgage Qualification

Commonly Accepted Front-End DTI Benchmarks in the Industry

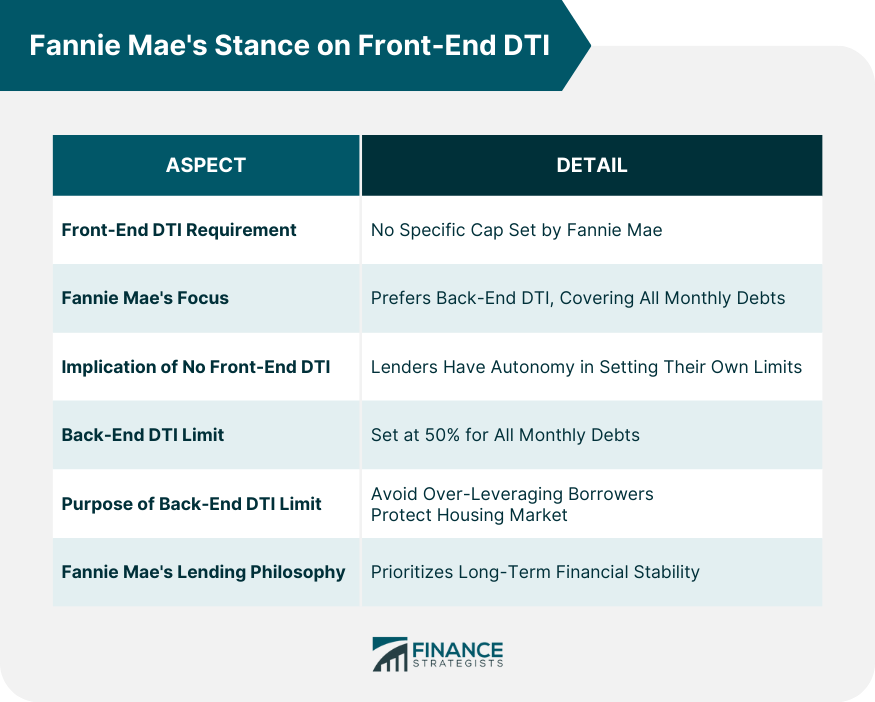

Fannie Mae's Stance on Front-End DTI

Absence of a Specific Front-End DTI Requirement

Emphasis on Back-End DTI: A Brief Look at the 50% Limit

Lender-Specific DTI Requirements

Why Lenders Might Set Their Own Front-End DTI Limits

Benefits and Challenges for Borrowers With Varying Front-End DTIs

Strategies for Borrowers to Improve Their Front-End DTI

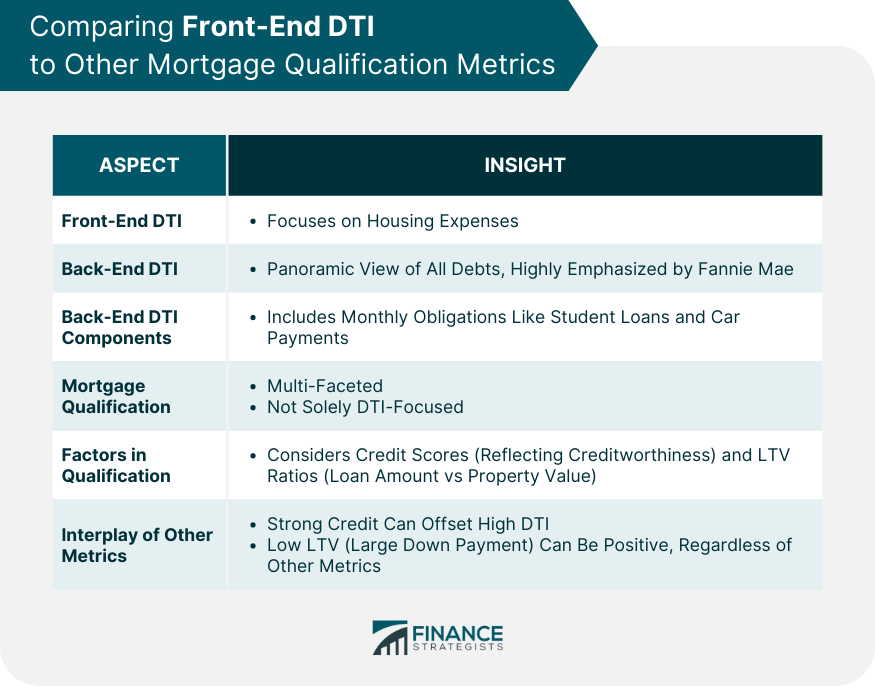

Comparing Front-End DTI to Other Mortgage Qualification Metrics

Importance of Back-End DTI in Fannie Mae's Guidelines

How Credit Scores, Loan-to-Value Ratios, and Other Factors Interplay With DTI

Bottom Line

Understanding Fannie Mae’s Stance on Front-End Ratio FAQs

It's a metric gauging major housing expense relative to a borrower's gross monthly income, often termed the housing ratio.

Lenders use this ratio to assess if borrowers can comfortably manage housing-related expenses; a lower DTI often signifies better financial flexibility.

No, Fannie Mae doesn't dictate a specific front-end DTI cap but places emphasis on the holistic back-end DTI.

Lenders tailor their guidelines based on risk tolerance, market positioning, and past experiences, especially in the absence of a direct mandate from Fannie Mae.

While the front-end focuses on housing expenses, the back-end DTI provides a broader view of a borrower's total monthly debt obligations, capturing a complete financial snapshot.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.