A personal line of credit allows individuals to borrow money up to a pre-approved credit limit as needed. This type of credit is commonly used for personal expenses, including home renovations, medical bills, and other unexpected expenses. There are two types of personal lines of credit: secured and unsecured. A secured personal line of credit is a credit line that is secured by collateral, such as a home or a vehicle. If the borrower cannot repay the credit, the collateral is forfeited to the lender. It often has lower interest rates than an unsecured personal line of credit, as it poses less risk to the lender. A secured personal line of credit offers several advantages to borrowers: Lower interest rates compared to Unsecured Personal Lines of Credit Higher credit limits Longer repayment terms While a secured personal line of credit can offer lower interest rates and higher credit limits, there are also several disadvantages to consider: Risk of losing the collateral if the borrower is unable to repay the credit Longer approval process due to the need for collateral evaluation Requires good credit history An unsecured personal line of credit is a credit line that is not backed by collateral. The lender assesses the borrower's creditworthiness and income to determine their eligibility for an unsecured personal line of credit. This type of credit often has higher interest rates than a secured personal line of credit, as it poses more risk to the lender. For individuals who do not want to use collateral to secure their credit line, an unsecured personal line of credit offers several advantages: Collateral is not required Faster approval process compared to a secured personal line of credit More flexibility in credit usage While an unsecured personal line of credit can offer greater flexibility in borrowing, there are also several disadvantages to consider, such as: Higher interest rates compared to secured personal line of credit Lower credit limits compared to secured personal line of credit Shorter repayment terms To get a personal line of credit, the borrower has to meet the lender's requirements and undergo the application process. One of the most important factors that lenders consider when assessing a borrower's eligibility for a personal line of credit is their credit score. A credit score numerically represents a borrower's creditworthiness based on their credit history. The higher the credit score, the more creditworthy the borrower is considered. The minimum credit score requirement varies by lender. Generally, lenders require a credit score of at least 680 to be eligible for a personal line of credit. However, some lenders may have more stringent credit score requirements. Lenders also consider a borrower's income and employment status when assessing their personal line of credit eligibility. The lender will want to see that the borrower has a steady income source, enabling them to make the minimum monthly payments on the credit. The minimum income requirement varies by lender. For example, lenders require a minimum annual income of $25,000 to be eligible for a personal line of credit. Lenders also consider the borrower's employment status when assessing their personal line of credit eligibility. Lenders prefer borrowers with a stable employment history with the same employer for at least two years. Lenders also consider a borrower's debt-to-income (DTI) ratio when assessing their personal line of credit eligibility. The DTI ratio is the percentage of the borrower's income that is used to pay off debt. A high DTI ratio may indicate that the borrower is over-extended and may have difficulty repaying a new credit line. The acceptable DTI ratio varies by lender. For instance, lenders may prefer borrowers with a DTI ratio of less than 40%. Personal line of credit applications usually follow these steps: The borrower must give the following information when applying for a personal line of credit: Personal information, such as name, address, and Social Security number Employment information, such as employer name, job title, and salary Financial information, such as bank account information and monthly expenses Credit information, such as credit score and credit history Once the borrower has gathered all the necessary information, they can begin the application process. The borrower will need to provide the lender with all the required information and documents, and the lender will assess the borrower's eligibility for a personal line of credit. The borrower will receive a credit limit and can begin using the credit line if approved. Once a borrower has been approved for a personal line of credit, they must manage it effectively to avoid overextending themselves and to maintain a good credit score. Personal lines of credit typically have variable interest rates, which means that the interest rate can change over time. Some lenders offer fixed interest rates, which means that the interest rate will not change throughout the credit term. They also have interest rate caps, which limit how high the interest rate can go. The borrower must make the minimum monthly payment on their personal line of credit, which is typically 1-2% of the outstanding balance. The repayment period varies by lender but is usually between 3-5 years. Late payment penalties may apply if the borrower fails to make the minimum monthly payment on time. The credit limit is the maximum amount of credit that the borrower can use on their personal line of credit. It is based on the borrower's credit score, income, and other factors. The credit limit may be increased or decreased over time, depending on the borrower's creditworthiness and credit line usage. A personal line of credit is a useful tool for individuals who need a flexible and affordable source of credit. Understanding the different personal lines of credit types, the application process, and how to manage it effectively can help borrowers make the most of this credit option. However, using this credit option responsibly is important to avoid overextending oneself and maintain a good credit score. If you are considering a personal line of credit or have questions about managing your finances, it may be beneficial to consult a financial advisor. They can assist you in making well-informed decisions and developing a financial strategy that meets your requirements and goals. You can also consult a mortgage broker if you plan on utilizing your home as collateral for a line of credit.Overview of a Personal Line of Credit

Types of Personal Lines of Credit

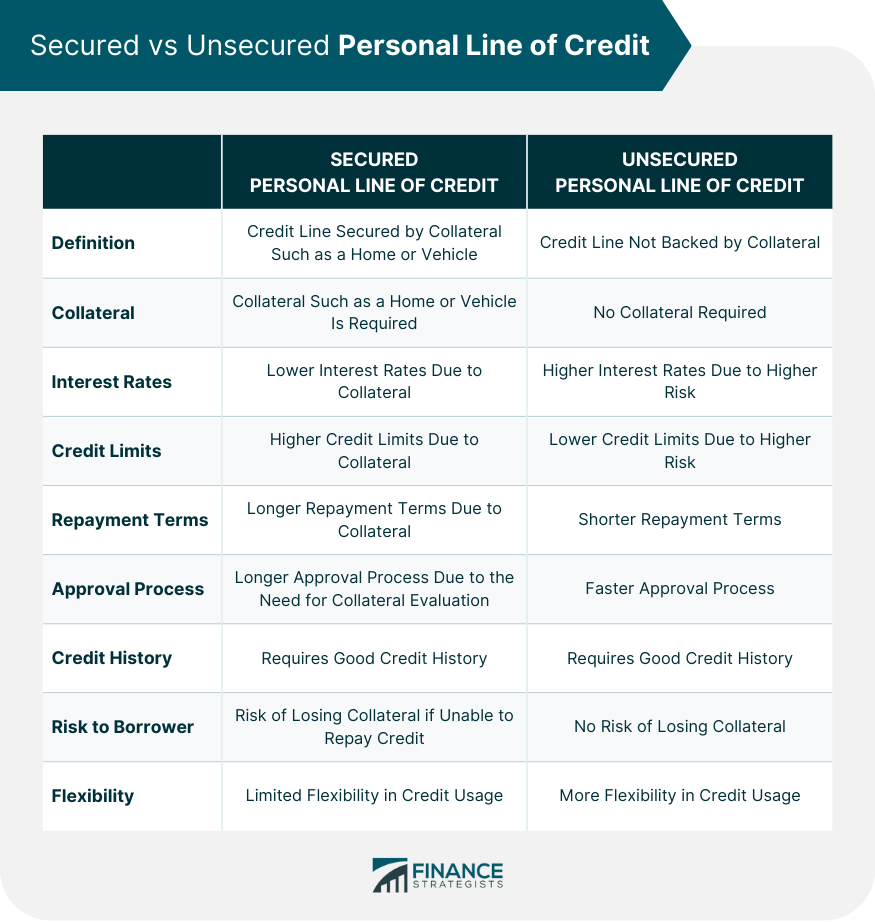

Secured Personal Line of Credit

Advantages of a Secured Personal Line of Credit

Disadvantages of a Secured Personal Line of Credit

Unsecured Personal Line of Credit

Advantages of an Unsecured Personal Line of Credit

Disadvantages of an Unsecured Personal Line of Credit:

Applying for a Personal Line of Credit

Credit Score

Income and Employment

Employment Status

Debt-to-Income Ratio

Application Process

Application Requirements

Application Procedure

Managing a Personal Line of Credit

Interest Rates

Repayment Terms

Credit Limit

Conclusion

Personal Line of Credit FAQs

A personal line of credit is a type of revolving credit that allows individuals to borrow money as needed, up to a pre-approved credit limit.

There are two types of personal lines of credit: secured and unsecured. A secured personal line of credit is backed by collateral, while an unsecured personal line of credit is not.

Most lenders need a credit score of at least 680, a steady source of income, and a debt-to-income ratio of less than 40%.

Managing a personal line of credit involves making the minimum monthly payments on time, keeping credit utilization low, and monitoring the credit limit and interest rates.

A personal line of credit offers borrowers flexibility in their borrowing, lower interest rates compared to credit cards, and convenient access to funds as needed.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.