Even as you age, a 401(k) plan continues to offer significant benefits. For workers aged 70 and older, contributing to a 401(k) remains a viable strategy. If you're still working, you can continue making contributions, maximizing your retirement savings. The IRS allows catch-up contributions for those over 50, providing an opportunity to save more. Additionally, once you reach 72, you're required to take minimum distributions (RMDs) from your 401(k) account, ensuring you have funds during retirement. However, if you're still working and don't own more than 5% of the business you work for, you can delay these RMDs until you retire. Overall, a 401(k) provides a tax-advantaged way to accumulate wealth, regardless of age. Always consult a financial advisor to understand your personal situation better and make the most of your retirement savings. Starting at age 72, 401(k) account holders must start taking RMDs each year. The specific amount depends on the account balance and the account holder's life expectancy. If the worker is still employed and doesn't own more than 5% of the company they work for, they can delay RMDs until they retire. This is known as the "still working" exception. Continued employment after the age of 70 allows workers to keep contributing to their 401(k) accounts, subject to the annual limits. This can be especially beneficial for those who wish to grow their retirement savings further. However, they must still start taking RMDs at 72 unless they qualify for the "still working" exception. The interaction between a 401(k) and Social Security benefits can be complex. Increased income from a 401(k), either through continued contributions or RMDs, could potentially increase the portion of Social Security benefits subject to income tax. However, these effects vary widely depending on individual circumstances. By continuing to contribute to a 401(k), workers 70 and older can benefit from continued tax-deferred growth. This means they don't pay taxes on the money in the account until they withdraw it, allowing their investments to grow more efficiently. Continued contributions can help increase retirement savings, providing a larger nest egg for the retirement years. This is particularly helpful for those who started saving later in life or experienced significant financial setbacks. A larger 401(k) balance gives retirees more flexibility in their retirement spending. They can potentially afford a higher standard of living, cover unexpected expenses, or leave a larger inheritance. RMDs can be a drawback as they might push an individual into a higher tax bracket. Additionally, these forced withdrawals may not align with a retiree's spending needs or desires, creating a potential cash flow dilemma. As mentioned, the increased income from a 401(k), either through continued contributions or RMDs, could result in more of a retiree's Social Security benefits being subject to income tax. Continued employment to contribute to a 401(k) might delay the transition to a retirement lifestyle. This can be a significant drawback for those looking forward to leaving the workforce and fully enjoying their retirement years. Workers need to balance the benefits of continued contributions with the potentially increased income taxes from RMDs. Depending on their tax situation, it might be beneficial to withdraw from the 401(k) at a steady rate instead of making further contributions. It's crucial to understand the potential effects of a 401(k) on the taxation of Social Security benefits and overall tax liability. This requires careful planning and might necessitate professional financial advice. A key part of managing a 401(k) at this age involves planning for retirement lifestyle and potential legacy. The choices made about continued employment, contributions, and withdrawals will significantly impact both. Given the complexity of these issues, seeking advice from a financial planner can be very beneficial. They can help navigate tax rules, RMDs, and planning for retirement lifestyle and legacy. Circumstances can change rapidly, and so can tax laws and retirement strategies. Regular reviews can help ensure that a worker's approach to their 401(k) remains appropriate and beneficial. Understanding the role and impact of RMDs is crucial. This includes knowing when to start taking them, how much to withdraw, and how these withdrawals will affect income and taxes. A 401(k) remains a potent financial tool for workers aged 70 and older. It allows ongoing contributions, thus further growing retirement savings and enabling tax-deferred growth. Workers can also utilize catch-up contributions, adding more to their accounts. The obligation of taking RMDs at 72 guarantees a flow of funds during retirement, with exceptions for certain still-employed individuals. However, potential drawbacks exist, including potential tax implications and cash flow challenges due to RMDs, possible delay in retirement lifestyle, and potential increased taxation of Social Security benefits. Balancing continued contributions with RMDs, assessing the impact on Social Security and overall tax situation, and planning for a comfortable retirement lifestyle are key considerations. Engaging a financial advisor for navigating complexities and regularly reviewing retirement strategies can optimize the benefits of a 401(k) plan for workers 70 and older.What Is a 401(k) For Workers 70 and Older?

How a 401(k) For Workers 70 and Older Works

Understanding Required Minimum Distributions (RMDs)

Impact of Continued Employment on 401(k) Contributions

Effect on Social Security Benefits

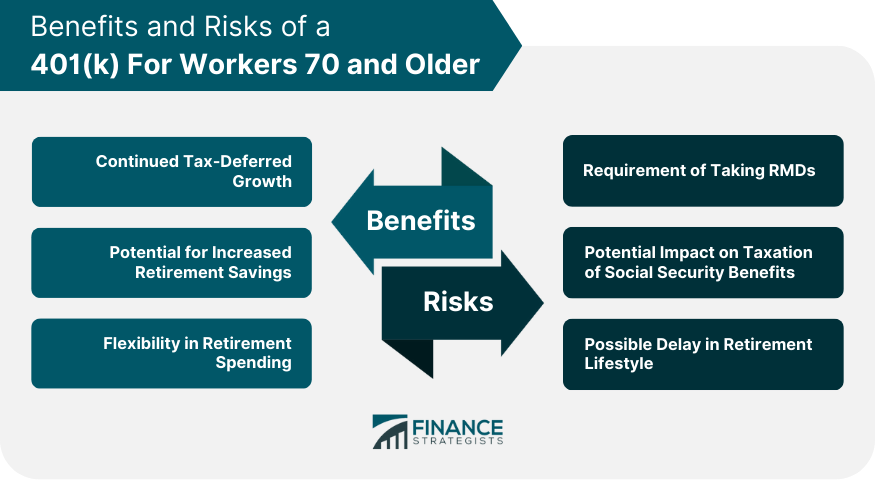

Benefits of a 401(k) For Workers 70 and Older

Continued Tax-Deferred Growth

Potential for Increased Retirement Savings

Flexibility in Retirement Spending

Risks of a 401(k) For Workers 70 and Older

Requirement of Taking RMDs

Potential Impact on Taxation of Social Security Benefits

Possible Delay in Retirement Lifestyle

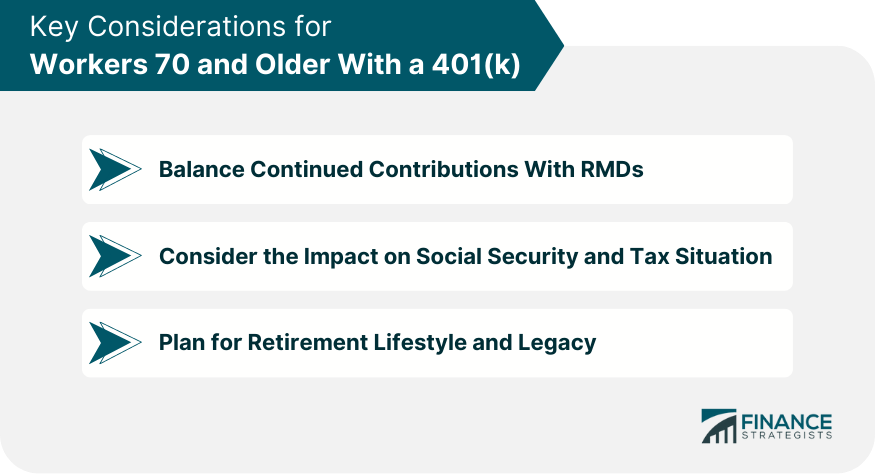

Key Considerations for Workers 70 and Older With a 401(k)

Balance Continued Contributions With RMDs

Consider the Impact on Social Security and Tax Situation

Plan for Retirement Lifestyle and Legacy

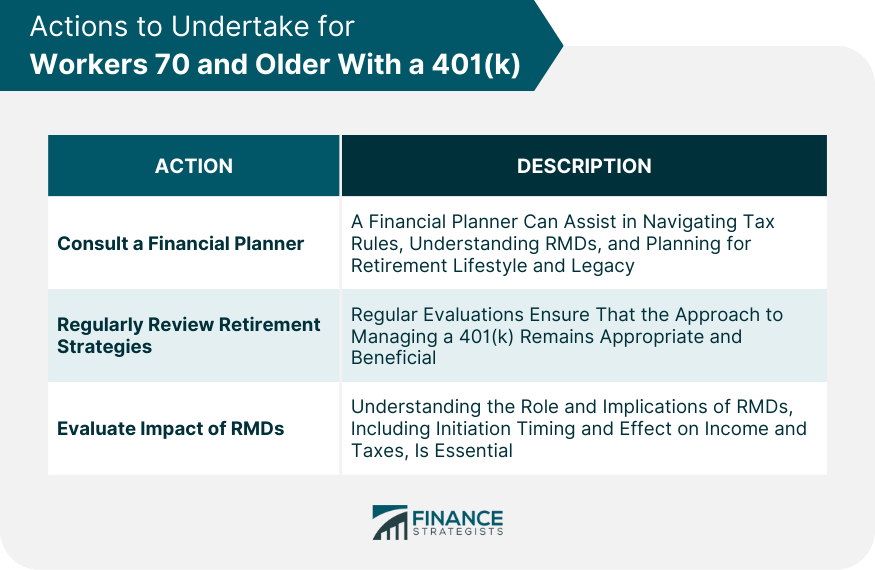

Actions to Undertake for Workers 70 and Older With a 401(k)

Seek Advice From a Financial Planner

Regularly Review Retirement Strategies

Assess the Need for and Impact of RMDs

Conclusion

401(k) For Workers 70 and Older FAQs

Required Minimum Distributions (RMDs) are the minimum amounts that a 401(k) account holder must withdraw annually starting at age 72. If you're still working and don't own more than 5% of the company you work for, you may delay RMDs until you retire.

Yes, workers 70 and older can still contribute to their 401(k) as long as they are still employed. The "still working" exception also allows these individuals to delay Required Minimum Distributions (RMDs) until retirement.

Increased income from a 401(k), either through continued contributions or RMDs, could potentially make more of your Social Security benefits subject to income tax. The effects vary greatly depending on individual circumstances.

Drawbacks include the mandatory RMDs which can potentially push individuals into a higher tax bracket, possible increase in taxation of Social Security benefits due to increased income, and the potential delay in transitioning to a full retirement lifestyle.

Key actions include seeking advice from a financial planner, regularly reviewing retirement strategies, and carefully assessing the need for and impact of RMDs, especially considering their tax implications and effect on retirement lifestyle and legacy.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.