Your 401(k) return can be influenced by various factors. Contribution amount and frequency significantly affect the growth potential of your account, while employer matching boosts your invested capital, increasing returns. Investment options chosen also play a critical role, as different assets carry varying risks and potential returns. Fees associated with your 401(k) can eat into your returns, making understanding and minimizing them essential. The power of compound interest magnifies over time, making a longer investment horizon beneficial. Economic factors such as inflation, interest rates, and market volatility can affect your return, as can your age and retirement date. The tax treatment of your contributions and changes in legislation can further influence your 401(k) return. The amount you regularly contribute to your 401(k) is the most direct influence on your return. Increasing your contributions allows for more potential growth. Many employers offer a matching program, essentially providing free money that can significantly increase your return. Contributing enough to earn the full employer match is critical. Your 401(k) plan's investment options significantly impact your return. These options usually include a range of mutual funds consisting of stocks, bonds, and cash equivalents. Higher-risk investments like stocks may yield higher returns but are also prone to larger losses. Diversifying your portfolio can help mitigate these risks. Various fees associated with your 401(k) plan can erode your return. These may include investment fees, administrative fees, and individual service fees. Understanding and minimizing these fees can help maximize your return. The longer your money is invested, the more potential it has to grow, thanks to compound interest. Starting early and having a longer investment horizon can significantly enhance your 401(k) return. Your 401(k) return is also susceptible to broader economic factors such as inflation, interest rates, and market volatility. While these factors are beyond your control, understanding their potential impact can help inform your investment strategy. Your age and the timing of your retirement can affect your 401(k) return. IRS rules allow older workers to make additional "catch-up" contributions. Moreover, if you retire during a market downturn, you may need to sell investments at low prices, impacting your return negatively. The tax advantages of a 401(k) contribute significantly to its potential return. Traditional 401(k) contributions provide a tax deduction now but will be taxed in retirement, while Roth 401(k) contributions are made with after-tax dollars but allow for tax-free withdrawals in retirement. The amount you contribute to your 401(k) directly affects the growth of your retirement savings. The more you put into your account, the more money is available to grow through investment. It's crucial to contribute as much as you can afford, up to the annual contribution limit set by the IRS. Frequency of contributions also plays a role in your 401(k) return. Making regular contributions not only increases the total amount you invest but also allows you to take advantage of dollar-cost averaging. This investment strategy involves regularly investing a fixed amount, regardless of market conditions. In many 401(k) plans, employers match a portion of your contributions. To maximize your return, it's recommended to contribute at least enough to get the full employer match. This is essentially free money that instantly increases your invested capital and, consequently, your potential result in a lower average cost per share, potentially leading to higher returns in the long run. An employer match instantly increases your 401(k) return, not by increasing the investment return percentage, but by amplifying your invested capital. The more money you have in your 401(k), the more you stand to gain from market returns. To optimize the benefits of employer matching, it's important to contribute at least enough to receive the full match. For instance, if your employer matches 100% of your contributions up to 3% of your salary, ensure you're contributing at least 3% of your salary to your 401(k). If you don't, you're essentially leaving free money on the table. Another major benefit of an employer match is its effect on compound interest. Compound interest is the interest you earn on your initial investment plus the interest that has already accrued. The more money you contribute - and the more your employer matches - the greater the power of compounding, leading to a higher 401(k) return in the long term. Typically the most significant fees associated with a 401(k) plan. They're usually charged as a percentage of the amount invested and cover services such as investment management and fund operating expenses. Plan administration fees cover the day-to-day operation of the 401(k) plan. These may include record-keeping, legal services, customer service, and other administrative services. Some plans charge these fees as a flat rate, while others charge them as a percentage of your investment. Individual service fees are charges for optional features offered by a 401(k) plan. These could include fees for taking a loan from your 401(k), fees for brokerage window services, or fees for financial planning services. Not all participants will pay these fees, as they only apply if you choose to use these services. Compounding is the process where earnings on your investments are reinvested to generate their own earnings. Over time, the effect of compounding can result in exponential growth of your 401(k). The more time you have, the more opportunities your money has to compound, leading to potentially larger gains. Starting your 401(k) contributions early can significantly boost your retirement savings due to the effect of compounding. Even smaller contributions made in the early years of your career can grow substantially over several decades. On the other hand, delaying your contributions can mean you have to invest significantly more money to achieve the same retirement goal. Your time horizon, or the period until you need to start withdrawing your funds, can also impact your 401(k) return. With a longer time horizon, you can afford to take on more risk for potentially higher returns, knowing you have time to recover from market downturns. As you near retirement, you may want to shift towards more conservative investments to protect your savings. Attempting to time the market can be risky. Most people aren't able to consistently predict market highs and lows. Instead, a steady, long-term investment approach can help smooth out short-term market fluctuations and lead to reliable growth over time. In conclusion, time is a powerful ally in growing your 401(k) return. Leveraging the power of compounding, starting early, adjusting your investment strategy according to your time horizon, and avoiding market timing can significantly enhance your retirement savings. Inflation represents the general increase in prices over time, which erodes the purchasing power of your money. If the return on your 401(k) investments is lower than the rate of inflation, you're losing purchasing power as the value of your accumulated wealth decreases in real terms. Therefore, to maintain or increase your purchasing power, your 401(k) return needs to outpace inflation. Interest rates can impact your 401(k) return in several ways. Lower interest rates can stimulate economic growth and lead to increased corporate profits, potentially boosting stock prices. Conversely, when interest rates rise, borrowing costs increase for companies, potentially reducing profits and causing stock prices to fall. Also, changes in interest rates can directly impact bond prices, affecting the fixed-income portion of your 401(k) portfolio. Market volatility refers to the degree of variation in the price of a financial instrument over time. During periods of high market volatility, your 401(k) investments can fluctuate greatly in value. This volatility can impact your 401(k) return, especially if you need to sell investments during a downturn. However, it's important to remember that 401(k) plans are typically long-term investments, and short-term market fluctuations should not dictate your overall investment strategy. Broad economic indicators like GDP growth and unemployment rates can also affect your 401(k) return. A strong economy usually translates into better corporate earnings, which can support stock prices. On the other hand, high unemployment rates can signal economic trouble, potentially impacting the financial markets negatively. The timing of your retirement can have a substantial effect on your 401(k) returns. If you retire when the market is up, your investments are likely worth more, and you can potentially sell them at a profit. However, retiring during a market downturn can lead to a reduction in the value of your portfolio and force you to sell your investments at a loss to cover living expenses. Your age not only influences the amount you can contribute but also the investment strategy you should follow. Younger individuals typically have a longer time horizon until retirement, and this allows them to take on more risk in hopes of achieving higher returns. As you near retirement, a more conservative approach is usually recommended to protect your savings from sudden market downturns. It's also important to note that your age can influence your 401(k) return if you decide to withdraw funds early. The IRS imposes a 10% penalty on early withdrawals (before age 59 ½) in addition to the ordinary income tax, which can significantly reduce your return. There are exceptions to the early withdrawal penalty, but generally, it's best to leave your 401(k) funds untouched until retirement. Once you reach age 73, the IRS requires you to start taking required minimum distributions (RMDs) from your 401(k). The amount of the RMD is based on your life expectancy and the balance in your account. If you don't need these distributions for living expenses, they could push you into a higher tax bracket, reducing your return. The primary benefit of a traditional 401(k) lies in tax deferment. By contributing pre-tax dollars, you reduce your current taxable income, potentially moving you into a lower tax bracket. The money then grows tax-deferred until retirement, at which point withdrawals are taxed as ordinary income. If you expect to be in a lower tax bracket in retirement, this can result in significant tax savings and a higher net return. A Roth 401(k) provides no immediate tax benefit since contributions are made with after-tax dollars. However, the potential for tax-free withdrawals in retirement can be significant. The money you contribute and the returns it generates can be withdrawn tax-free, provided you're at least 59½ and the account has been open for at least five years. If you expect to be in a higher tax bracket in retirement, a Roth 401(k) can enhance your net return. Your choice between a traditional and Roth 401(k) significantly impacts your return. The right choice depends on your current and expected future tax rates, as well as your financial goals. Understanding how tax treatment affects your 401(k) return can help you make an informed decision and optimize your retirement savings. Legislation often changes the contribution limits for 401(k) plans. For example, the IRS often adjusts these limits annually to account for inflation. If the contribution limit increases, it allows you to invest more money into your 401(k), potentially increasing your future returns. Changes in tax laws can also significantly impact your 401(k) return. For instance, if tax rates were to increase in the future, it could reduce the after-tax value of your retirement savings. Alternatively, if the government decided to make 401(k) withdrawals tax-free, this would effectively increase your return. Sometimes, legislation can affect the types of investments available within a 401(k) plan. These changes could potentially affect your return, depending on whether they expand or limit your investment options. More options generally allow for better diversification, which could potentially enhance your return. The legislation determines the age at which you must start taking required minimum distributions (RMDs) from your 401(k). For example, the SECURE Act of 2019 raised this age from 70.5 to 73. This change gives your investments more time to grow if you don't need to withdraw them, potentially increasing your 401(k) return. Optimizing your 401(k) return relies on understanding and carefully managing key factors. Diligent contributions, maximizing employer match opportunities, and making wise investment choices can significantly enhance growth potential. Being aware of fees and actively working to minimize them also plays an integral role. Furthermore, leveraging time and compound interest by starting early can lead to substantial returns in the long run. Although uncontrollable, economic variables are essential to comprehend as they can sway your return. Adjusting your strategies based on age, retirement date, and catch-up contributions also makes a difference. Lastly, understanding the implications of tax treatments and staying informed about legislative changes is crucial, as these can have substantial effects on your return. Together, these strategies provide a robust approach to maximizing your 401(k) return.Factors Affecting Your 401(k) Return Overview

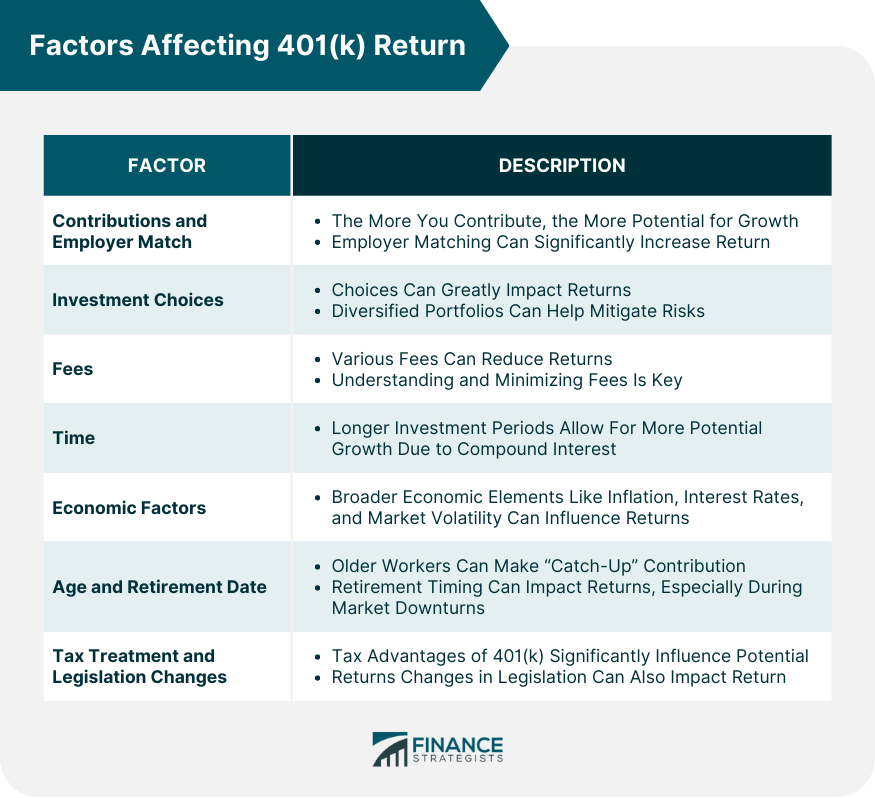

What Are the Factors Affecting Your 401(k) Return

Contributions and Employer Match

Investment Choices

Fees

Time

Economic Factors

Age and Retirement Date

Tax Treatment and Legislation Changes

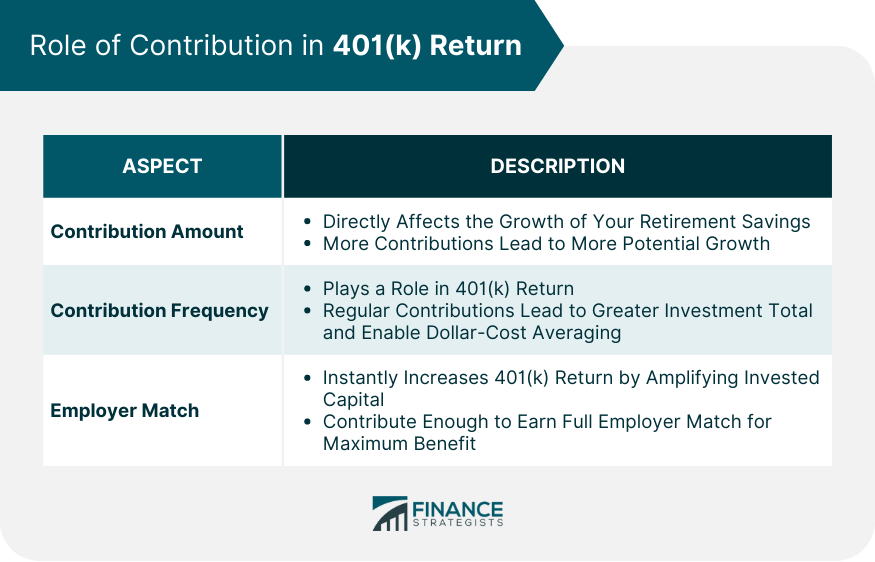

Role of Contribution in 401(k) Return

Impact of Contribution Amount

Effect of Contribution Frequency

Maximizing Contributions and Employer Match

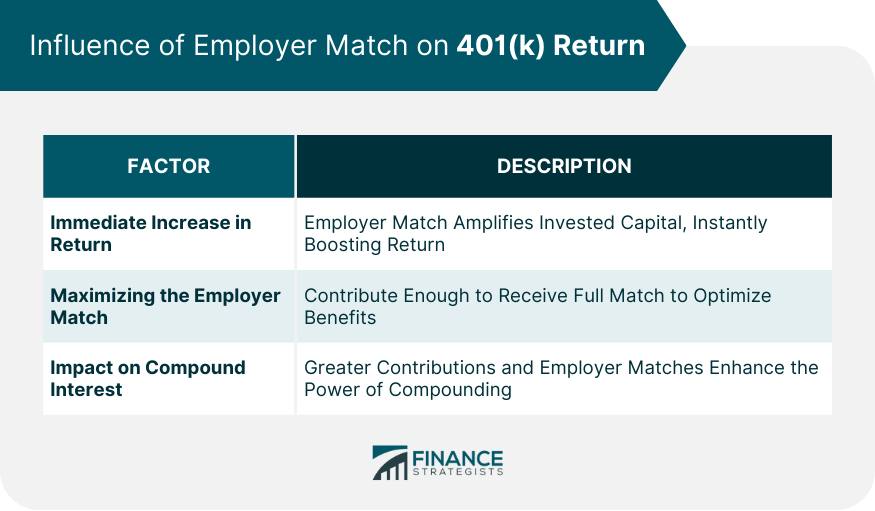

Influence of Employer Match on 401(k) Return

Immediate Increase in Return

Maximizing the Employer Match

Impact on Compound Interest

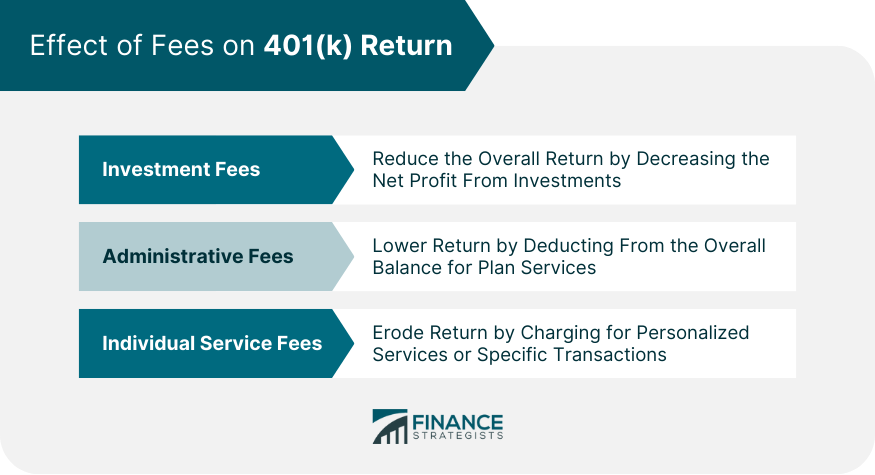

Effect of Fees on 401(k) Return

Investment Fees

Plan Administration Fees

Individual Service Fees

Role of Time in 401(k) Return

Time and the Magic of Compounding

Power of Starting Early

Time Horizon and Investment Strategy

Impact of Market Timing

Impact of Economic Factors on 401(k) Return

Influence of Inflation

Role of Interest Rates

Effect of Market Volatility

Economic Growth and Unemployment Rates

Influence of Age and Retirement Date on 401(k) Return

Timing of Retirement and Its Impact on Returns

Age and Investment Strategy

Consequences of Early Withdrawals

Role of Required Minimum Distributions

Effect of Tax Treatment on 401(k) Return

Traditional 401(k) and Deferred Taxes

Roth 401(k) and Tax-Free Withdrawals

Tax Treatment and Your 401(k) Return

How Changes in Legislation Can Impact 401(k) Return

Impact of Contribution Limit Changes

Changes in Tax Laws

Legislation Affecting Investment Choices

Mandatory Withdrawal Rules

Conclusion

Factors Affecting Your 401(k) Return FAQs

Your contributions form the basis of your 401(k) return. The more you contribute, the larger the initial sum that can grow through investment. Regular contributions also allow you to take advantage of dollar-cost averaging, potentially leading to higher returns in the long run.

An employer match instantly boosts your 401(k) return by increasing your invested capital without any additional investment from your pocket. Understanding your employer's matching policy and contributing at least enough to get the full match can significantly enhance your 401(k) return.

The investment options you select can significantly impact your 401(k) return. Diversification can help manage risk, while your risk tolerance and investment goals should guide your choices. The risk-return trade-off principle also plays a part, with higher-risk investments potentially offering higher returns.

Fees can reduce your 401(k) return by taking away from the power of compound interest. It's important to understand the various types of fees you may encounter, such as investment fees, plan administration fees, and individual service fees, and how they can impact your return.

The tax treatment of your 401(k) investments can significantly impact your return. Traditional 401(k) contributions lower your taxable income now but will be taxed upon withdrawal in retirement. Roth 401(k) contributions are made with after-tax money, and withdrawals in retirement are tax-free. The choice between these depends on your current and expected future tax rates.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.