A 401(k) plan is an employee benefit offered by some employers. Employees may contribute a portion of their income to the plan and in some cases, employers also match contributions. The money is invested and can be accessed when they retire. Have questions about 401(k) Plans? Click here. A 401(k) plan usually consists of three components: employee deferrals, employer contributions, and investment options. Under a traditional 401(k), employees choose how much to contribute from their paychecks each month. Their choices might be limited to a certain percentage of their income. How much employees contribute is not subject to federal taxes; the employees' paychecks are adjusted accordingly and all contributions go into the 401(k) account. Employers also make contributions, usually as a percentage of the employees' salaries, but can offer other options such as matching a certain percentage of an employee's contributions up to a certain amount or contributing a flat dollar amount for each pay period in which the employee contributes. Contributions may consist entirely of pre-tax dollars or part may be made with after-tax dollars. To invest their money, employees typically choose specific funds within the 401(k) plan, like a target-date fund or a balanced fund. This way the employee doesn't have to manage this part of their retirement savings and can leave it to a professional financial manager who has access to a wide range of investment choices. Anyone who has a 401(k) plan at their job can contribute. If an employer offers a match, that contribution is free money, and it's in the worker's best interest to take advantage of that extra savings. The following conditions apply: If you're married, your spouse can also contribute to a 401(k) even if he/she has another job where there is no employer match. Similar to taxes on traditional IRA accounts, contributions made to a traditional 401(k) plan are not deductible on a person's federal income tax return. 401(k) plans have been around since 1978. They have become popular as an alternative to the IRA because they offer several benefits:What Is a 401(k) Plan?

How Does the 401(k) Work?

Who Can Contribute to a 401(k)?

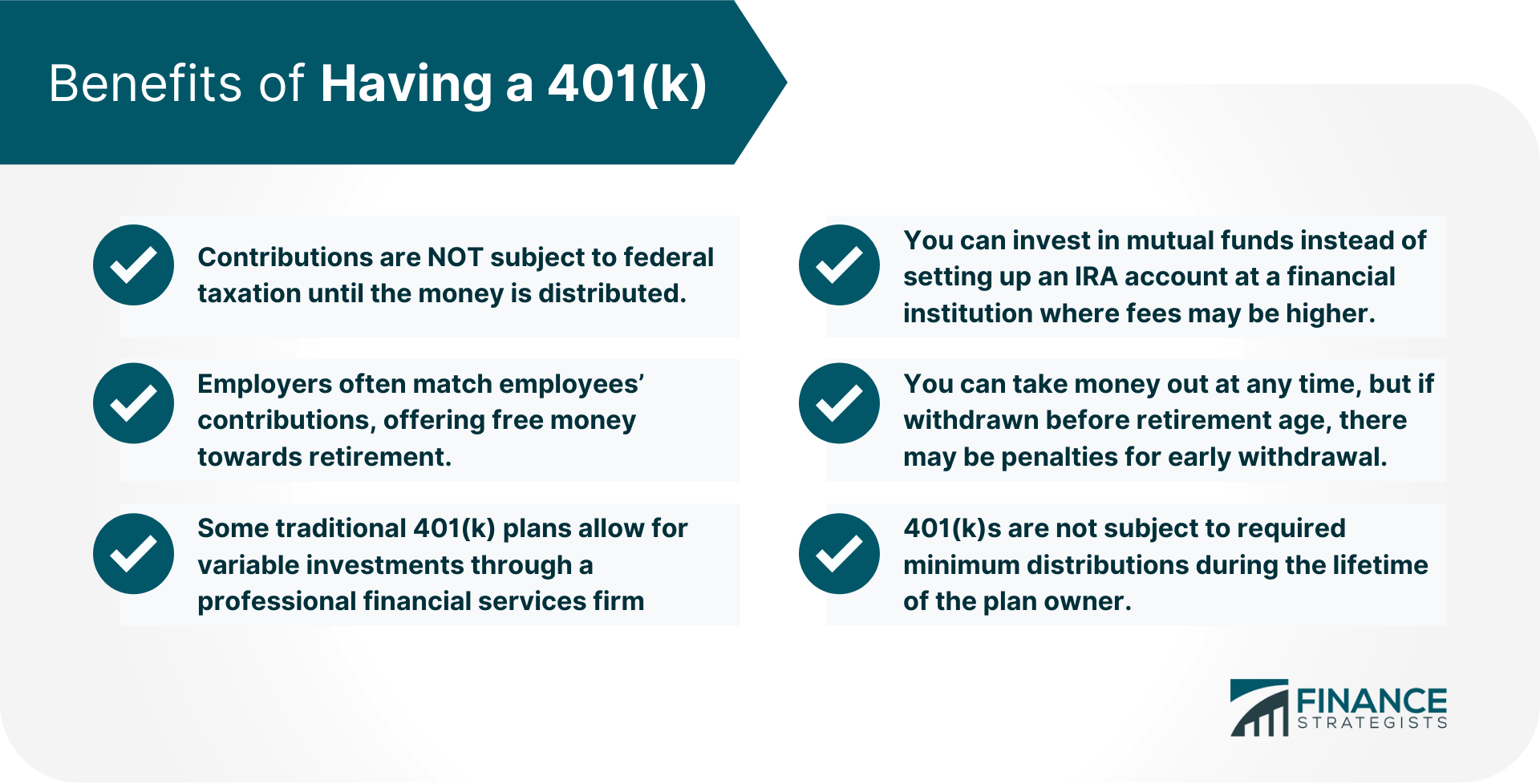

What Are the Benefits of Having a 401(k)?

What Are Some Drawbacks of Having a 401(k)?

How a 401(k) Works FAQs

A 401(k) is a type of retirement savings account. How much money you contribute to your 401(k) is deducted from your paycheck before taxes are taken out, which can lower your taxable income.

Your employer or plan provider sets aside a portion of your income before you get paid. You choose how to invest the money from a list of options, and once you invest, it's up to you to monitor your portfolio balance and make changes if necessary.

The IRS caps the maximum annual contribution that you can make to any 401(k) plan at $19,500 for 2020. You can contribute to an IRA in addition to your 401(k). How long you can contribute depends on how old you are when you start making contributions. You can begin contributing to your traditional 401(k) account when you start working, typically at age 18 or older, but the maximum contribution limit for any year is $19,500 if you are under 50 years old in 2020.

Your employer may go out of business or choose to stop offering the plan. However, you will still have to pay taxes on any withdrawals that you take while it's still in operation. If your account fails, your assets are insured by the Pension Benefit Guaranty Corporation (PBGC).

Your plan provider (usually your employer) offers a list of investment options such as stocks, bonds, and mutual funds. You choose where to invest your money. It's up to you to monitor your investments and make changes if necessary.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.