A Roth 401(k) is a type of employer-sponsored retirement savings account. Unlike its traditional counterpart, contributions to a Roth 401(k) are made with after-tax dollars. This means that while there are no immediate tax benefits for contributing, the distributions taken during retirement are typically tax-free, provided certain conditions are met. This design can be particularly advantageous for younger workers or those expecting to be in a higher tax bracket upon retirement. The key distinction between a traditional 401(k) and a Roth 401(k) is tax treatment. Traditional 401(k) contributions are pre-tax, lowering your current taxable income, but taxed upon retirement withdrawal. Conversely, Roth 401(k) contributions are taxed initially, enabling tax-free withdrawals in retirement. The choice between the two typically depends on your present and predicted future tax brackets, along with your retirement goals. Surprisingly to many, the Roth 401(k) doesn’t have income limits for eligibility in the same way Roth IRAs do. This means that regardless of how much you earn, you can contribute to a Roth 401(k) if your employer offers this type of plan. The real limitations are on the contribution amounts, which for 2024, for instance, were capped at $23,000 ($23,500 for 2025) for those under 50 and $30,500 ($31,000 for 2025) for those 50 and older due to catch-up contributions. This lack of income restriction broadens accessibility for high earners, who may otherwise be limited with Roth IRAs. The Roth 401(k) was introduced in 2006 as a result of the Economic Growth and Tax Relief Reconciliation Act of 2001. Since its inception, the focus has been more on the contribution limits rather than income limits. This design aimed to provide high earners an opportunity to partake in Roth-style retirement benefits, especially since they might be phased out of Roth IRA contributions due to its strict income limitations. It can be seen as an attempt to democratize the benefits of Roth accounts for a broader audience. Although there's no income limit to contribute to a Roth 401(k), it’s crucial to understand that other factors might affect your contribution amounts. For instance, Highly Compensated Employees (HCEs) might face certain restrictions due to non-discrimination testing requirements. Additionally, the presence of a Roth 401(k) doesn't negate the Roth IRA's income limits. Hence, while you may freely contribute to the former, the latter might still be off-limits based on your income. Balancing contributions across various accounts can be a nuanced process, requiring careful planning. Tax-Free Distributions: Once you reach retirement, and if you've held the account for at least five years, you can enjoy tax-free distributions. This can be a boon in scenarios where you anticipate being in a higher tax bracket during retirement. No RMDs if Rolled Over: Unlike traditional 401(k)s, Roth 401(k)s have Required Minimum Distributions (RMDs). However, if you roll over your Roth 401(k) into a Roth IRA, you can bypass these RMDs, allowing for greater flexibility in retirement planning. Beneficial for High Earners: As stated, high earners who are phased out of Roth IRA contributions can still partake in Roth 401(k) benefits. This opens the door for diversified tax strategies, even for those in the upper echelons of income. No Immediate Tax Benefit: Since contributions are after-tax, there's no immediate reduction in taxable income. For those looking for immediate tax relief, this could be a downside. It necessitates a more long-term view of tax benefits. Employer Match Is Pre-Tax: If your employer matches your Roth 401(k) contributions, their match will be pre-tax, necessitating tax payment upon withdrawal. This can create a dual-tax scenario that might complicate withdrawal strategies. Mandatory RMDs: Unlike Roth IRAs, Roth 401(k)s come with Required Minimum Distributions (RMDs). If not rolled over, this can be a limitation for those looking to grow their investments longer or pass them on. As previously mentioned, the Roth 401(k) and Roth IRA allow for after-tax contributions with tax-free distributions, whereas the Traditional 401(k) and Traditional IRA provide tax benefits upfront with taxes due upon withdrawal. This distinction primarily revolves around when you believe your taxes will be highest—now or in retirement. Roth IRAs have stringent income limits for contributions. Traditional IRAs have income limits related to deductibility if you're covered by a workplace retirement plan. Traditional 401(k)s and Roth 401(k)s, on the other hand, only focus on contribution limits, not income. This landscape means that high earners have to navigate these rules with precision to maximize benefits. Roth 401(k)s and Traditional 401(k)s have RMDs, whereas Roth IRAs do not. Traditional IRAs have RMDs starting at age 72. It's important to note these distinctions as they can significantly impact one's retirement withdrawal strategies and tax implications. Beyond Roth 401(k) contributions, if you're ineligible for Roth IRA contributions due to high income, consider putting money into a traditional IRA (though deductibility might be constrained). This multi-layered strategy provides avenues for various tax advantages, offering an expansive safety net for your retirement. For those aged 50 and above, the catch-up contribution is a golden opportunity. It allows you to deposit extra funds beyond the standard contribution limits. This is particularly useful if you start saving for retirement later than planned or if you're trying to maximize your nest egg in the final push before retirement. Even though there isn't an income limit for the Roth 401(k), understanding the specifics of this account is crucial. By juxtaposing this with the income constraints of other accounts like Roth IRAs, you can sculpt a comprehensive retirement strategy. It's always essential to assess your current financial status, projected future income, and anticipated retirement needs. The Roth 401(k) serves as a flexible tool in your retirement arsenal, ensuring that even high earners can diversify their retirement savings to enjoy tax-free withdrawals in their golden years. Implementing the Roth 401(k) into your broader financial plan requires foresight, understanding its unique features, and syncing them with your retirement vision. Forecasting future tax brackets can be a challenge, but it's a necessary step. If you anticipate being in a higher tax bracket during retirement, the Roth 401(k) shines. Remember, by paying taxes now, you shield yourself from potentially higher taxes later. Conversely, if you expect to be in a lower bracket post-retirement, a traditional 401(k) might be more fitting. It's a balance between current tax benefits and future tax savings. While the Roth 401(k) is a powerful retirement vehicle, it should not be the sole focus. Consider other investment opportunities such as stocks, bonds, mutual funds, and real estate. Diversifying your investments not only spreads risks but also provides multiple streams of income during retirement. Given the complexity of retirement planning and the multitude of available options, consulting with a financial planner, or advisor can be invaluable. They can offer personalized advice, taking into account your income, age, retirement goals, and risk tolerance. They can also assist in devising strategies to maximize the benefits of a Roth 401(k) and integrate it seamlessly into your broader financial blueprint. The Roth 401(k) is an attractive retirement savings tool that allows tax-free withdrawals in retirement. Its design caters to high earners who might otherwise face restrictions with Roth IRAs and for those anticipating a higher tax bracket upon retirement. The absence of income limits and the opportunity for catch-up contributions make it flexible, promoting diversified retirement planning. However, the Roth 401(k) does not operate in isolation and should be considered alongside other investment opportunities to form a comprehensive strategy. It's crucial to understand your current and future tax brackets, analyze other investment opportunities, and consider how the Roth 401(k) aligns with your overall retirement vision. The process can be complex and calls for nuanced understanding, reinforcing the value of professional advice. As your next step toward a secure retirement, consider seeking expert retirement planning services to optimize your Roth 401(k) and other retirement saving options.Understanding Roth 401(k)

Roth 401(k) Income Limit

Direct Explanation of Roth 401(k) Income Limits

Historical Context of Roth 401(k) Income Limits

How the Income Limit Might Impact Your Ability to Contribute

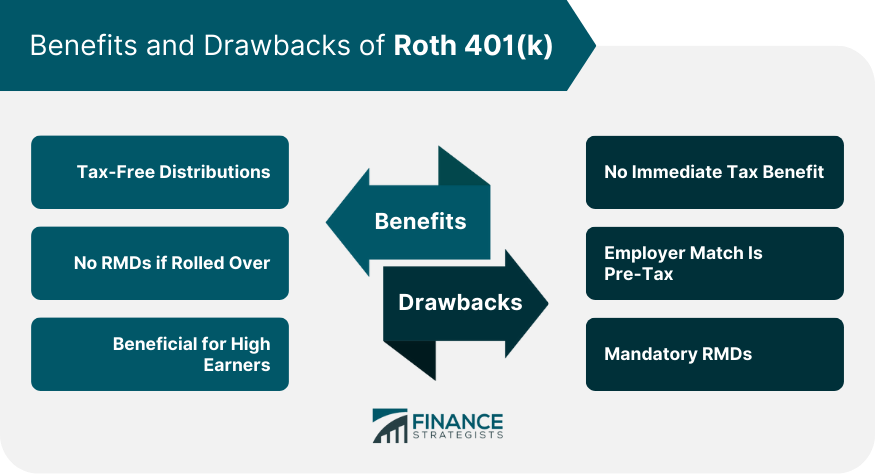

Benefits and Drawbacks of Roth 401(k)

Benefits of Investing in Roth 401(k)

Drawbacks and Limitations of Roth 401(k)

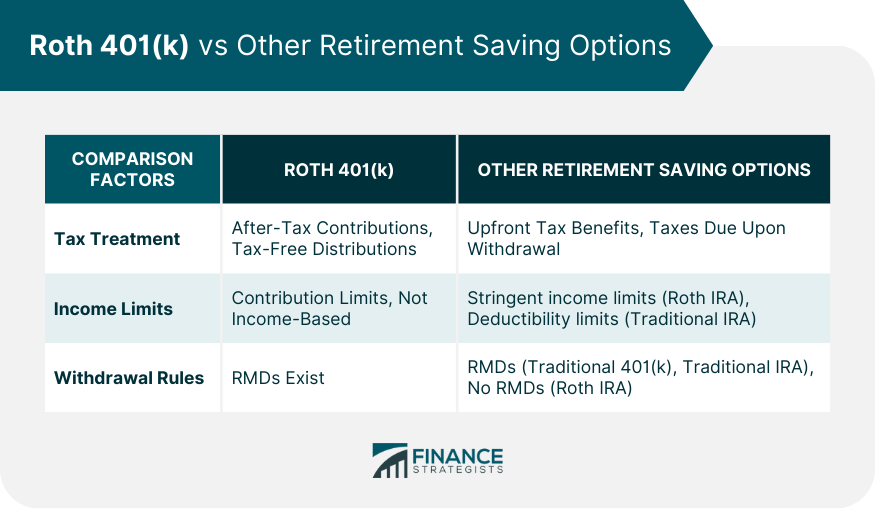

Roth 401(k) vs Other Retirement Saving Options

Tax Treatment

Income Limits

Withdrawal Rules

How to Optimize Contributions in Roth 401(k)

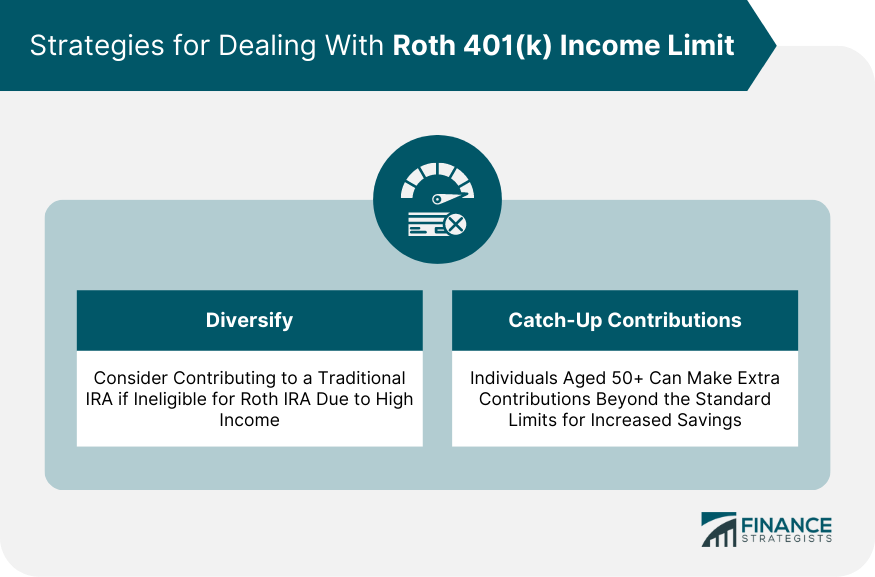

Strategies for Dealing With Roth 401(k) Income Limit

Diversify

Catch-Up Contributions

Impact of Roth 401(k) Income Limit on Retirement Saving Strategy

Implementing Roth 401(k) in Your Financial Plan

Consider Current and Future Tax Brackets

Analyze Other Investment Opportunities

Consult With a Financial Planner

Bottom Line

Roth 401(k) Income Limit FAQs

Roth 401(k) income limits refer to the maximum annual income that an individual can earn and still be eligible to contribute to a Roth 401(k) retirement account. These limits are set by the Internal Revenue Service (IRS) and are subject to change each year. Contributions to a Roth 401(k) are made with after-tax dollars, allowing for tax-free withdrawals in retirement.

No, the Roth 401(k) income limits do not change based on your age. The IRS sets the income limits uniformly for all eligible individuals, regardless of age. The income limits are typically adjusted each year based on inflation and other factors, but age is not a criterion for determining eligibility or contribution limits for a Roth 401(k). However, it's essential to be aware that as you age, your retirement planning needs may change, and it's always a good idea to review and adjust your retirement savings strategy periodically, considering factors like risk tolerance, investment goals, and time horizon.

If your income exceeds the Roth 401(k) income limits set by the IRS, you may not be eligible to make direct contributions to a Roth 401(k). However, you might still have the option to contribute to a Traditional 401(k) or other retirement accounts, depending on your situation. Additionally, you may consider a backdoor Roth IRA conversion if you are interested in a Roth-like account.

If you inadvertently contribute to a Roth 401(k) when your income exceeds the IRS limits, you will need to correct the situation to avoid potential tax penalties. The excess contributions should be withdrawn from the account by the tax-filing deadline for the given year (including extensions) to avoid a 6% excise tax on excess contributions. Consult with your plan administrator or financial advisor to facilitate the correction process.

No, Roth IRA income limits are different from Roth 401(k) income limits. While both are retirement savings options, they have separate contribution rules and income limits. Roth IRAs have their own set of income limits, which may be subject to change by the IRS each year. It's important to distinguish between the two and ensure you meet the eligibility criteria for each specific account type when considering retirement savings options.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.