A Church Retirement Plan, also known as a 403(b)(9) plan, is a specialized retirement savings vehicle designed to meet the distinct needs of religious organizations and their employees. It offers a unique blend of flexibility and security. The plan considers the unique tax implications and lifestyle needs often associated with clergy and church staff, providing a customized solution that aligns with spiritual service values. The Church Retirement Plan is a financial tool and a testament to different churches’ commitment to the well-being of their dedicated service members. Eligibility for these plans typically includes clergy members, such as ministers, priests, and pastors, as well as lay employees in administrative, educational, or operational roles. Employees of affiliated organizations like church-run schools or hospitals may also qualify. Full-time employees are usually eligible, while part-time employees might need to meet minimum service requirements. Plans can vary, with some offering immediate eligibility and others imposing waiting periods. Automatic enrollment increases participation rates, but some plans require voluntary enrollment. Clergy members often have unique provisions, such as dual-status considerations and the inclusion of housing allowances for contribution calculations. Each plan's specific design can tailor eligibility criteria to fit the organization's needs. The IRS sets annual contribution limits for Church Retirement Plans, similar to other 403(b) plans. For 2024, the combined limit for employee and employer contributions is $69,000 ($70,000 in 2025) or 100% of the employee's includible compensation, whichever is less. The elective employee deferral limit is up to $23,000 ($23,500 in 2025). Employees aged 50 and older can make additional catch-up contributions of up to $7,500 for both 2024 and 2025. Special catch-up contributions are available for employees with 15 or more years of service with the same employer, potentially allowing for higher contributions. Contributions can be pre-tax, reducing current taxable income, or post-tax with Roth options, offering tax-free growth and withdrawals. These limits help ensure substantial retirement savings while providing tax advantages. Church retirement plans offer various investment options to accommodate risk tolerances and retirement goals. Common choices include mutual funds, which provide diversification across stocks, bonds, or a mix of both; annuities, which offer a steady income stream in retirement; and other financial instruments like index funds and target-date funds. Participants can tailor their investment strategy based on their financial situations, selecting more aggressive or conservative income-focused growth options. Plan administrators often provide educational resources and tools to help employees make informed investment decisions to ensure the retirement portfolios align with employees’ long-term objectives. Withdrawals from church retirement plans are generally governed by rules similar to those for other retirement plans. Participants can typically begin taking distributions at age 59½, with withdrawals taxed as ordinary income unless they are Roth contributions, which can be tax-free. Required Minimum Distributions (RMDs) must start by April 1 of the year after the participant turns 73. Some plans offer provisions for hardship withdrawals, allowing access to funds in cases of severe financial need, though these may incur taxes and penalties. Loan options may also permit employees to borrow against their retirement savings depending on a particular plan’s provisions. Contributions to these plans are typically tax-deferred, which means that employees do not have to pay taxes on the money they contribute or the earnings on those contributions until they withdraw the funds in retirement. Additionally, clergy members have the unique benefit of designating a portion of their retirement distributions as a housing allowance, which can be excluded from taxable income. This provision is especially beneficial for clergy who often have housing provided by their religious organization during their working years. These retirement plans offer substantial flexibility, allowing churches to design plans tailored to the specific needs of their employees. Church Retirement Plans can include employer matching contributions, discretionary contributions, and various vesting schedules, all of which can be customized to meet the organization's and its employees' goals. The contribution limits are also generous, enabling employees to save substantial amounts for retirement. For example, ministers treated as self-employed for tax purposes can contribute to the plan, maximizing both employer and employee contribution limits. This can significantly enhance their retirement savings potential. Furthermore, many 403(b)(9) plans are exempt from the Employee Retirement Income Security Act (ERISA), reducing administrative costs and regulatory burdens. This exemption allows smaller churches to offer competitive retirement benefits without the complexity and expense associated with ERISA compliance. It also makes the plans easier to administer and potentially lowers participants' fees. While the exemption from ERISA can reduce costs and administrative burdens, it also means that Church Retirement Plans are not subject to the same fiduciary and protection standards as ERISA-covered plans. This lack of oversight can result in fewer protections for plan participants, such as less stringent requirements for plan governance, funding, and disclosure. Participants in these plans may have fewer legal resources in case of mismanagement or fiduciary breaches. If an employee leaves the religious organization, transferring funds from a 403(b)(9) plan to other types of retirement plans, such as an IRA or a 401(k), may be more challenging. The rules and limitations on rollovers can vary depending on the plan and the denomination's regulations. This can create complications for employees who change jobs or retire and wish to consolidate their retirement savings. Understanding the portability options and any potential tax implications or restrictions is crucial for employees considering leaving their current organization. The special tax treatment and provisions for clergy within 403(b)(9) plans can add complexity to tax planning and compliance. For instance, the tax rules regarding the housing allowance designation can be intricate, requiring careful documentation and adherence to IRS guidelines. Additionally, the benefits and rules can vary significantly between different denominations and church organizations, making it essential for employees to understand their specific plan’s details thoroughly. Clergy members may need specialized tax advice to navigate these complexities effectively and ensure they maximize their tax advantages while complying with all regulatory requirements. This involves considering the needs and goals of the church and its employees, including decisions on the types of benefits to offer, such as employer matching contributions and vesting schedules. Choosing a qualified plan administrator or financial institution is crucial in handling the day-to-day operations, including record-keeping, compliance, and investment management. Developing a comprehensive plan document is essential, outlining the plan’s terms and conditions, eligibility requirements, contribution limits, and distribution rules. This document should comply with IRS regulations and other laws to ensure the plan is legally sound. Providing education resources is vital to help employees understand the benefits and features of the retirement plan. This can include workshops, webinars, and informational materials on investment options and retirement planning. Regular communication with plan participants is also important, providing updates on plan performance, changes to the plan, and essential deadlines. Clear and consistent communication helps employees stay informed and engaged with their retirement savings, fostering a sense of ownership and involvement in their financial futures. Offering a diverse range of investment options is crucial to meet plan participants' varying risk tolerances and retirement goals. This includes options such as mutual funds, target-date funds, and annuities. Regularly reviewing and monitoring the performance of these investment options ensures they continue to meet the needs of participants. Providing access to financial advisors or investment professionals can also help employees make informed investment decisions and develop personalized retirement strategies. Advisors play a key role in guiding participants through the complexities of investment choices and retirement planning. This process involves staying informed about changes in regulations that affect 403(b)(9) plans and ensuring that the plan complies with IRS rules and other applicable laws. This may require periodic reviews and updates to the plan document. Annual reporting obligations include completing required filings and disclosures, providing participants with regular account balances and performance statements, and issuing any mandated notices or disclosures. This evaluation should consider whether the plan is meeting the church's and its employees' objectives and needs. Gathering feedback from plan participants can help identify areas for improvement. This feedback should be used to make necessary adjustments to the plan design, investment options, or educational resources, ensuring the plan remains relevant and beneficial to its participants. Working with the plan administrator and investment providers to negotiate competitive fees can enhance the overall returns for plan participants. Ensuring that all fees associated with the plan are clearly disclosed to participants is also crucial. Transparency in fee structures builds trust and allows employees to make informed decisions about their retirement savings, knowing exactly what costs are involved. Clergy should be made aware of how to properly designate a portion of their retirement distributions as a housing allowance and the documentation required to comply with IRS rules. Additionally, it is important to assist clergy who are treated as self-employed with understanding their ability to make contributions to the plan. Providing clear information on maximizing their contributions within the limits set by the IRS can help clergy optimize their retirement savings. Church retirement plans, specifically 403(b)(9) plans, provide a robust framework for ensuring the financial security of clergy and church employees. These plans offer significant advantages, including substantial tax benefits, flexible design options tailored to the unique needs of religious organizations, and special provisions for ministers that enhance their retirement savings potential. However, the lack of ERISA protections, reduced portability, and complexities in tax treatment for clergy present challenges that require careful consideration. Effective management of a church retirement plan involves strategic planning, comprehensive employee education, diligent investment management, and ongoing compliance monitoring. By addressing these elements, churches can create a supportive retirement environment that aligns with their mission and values, ensuring that their dedicated service members are well-prepared for a secure and comfortable retirement.What Is a Church Retirement Plan?

How Church Retirement Plans Work

Eligibility and Participation

Contribution Limits

Investment Options

Distribution Rules

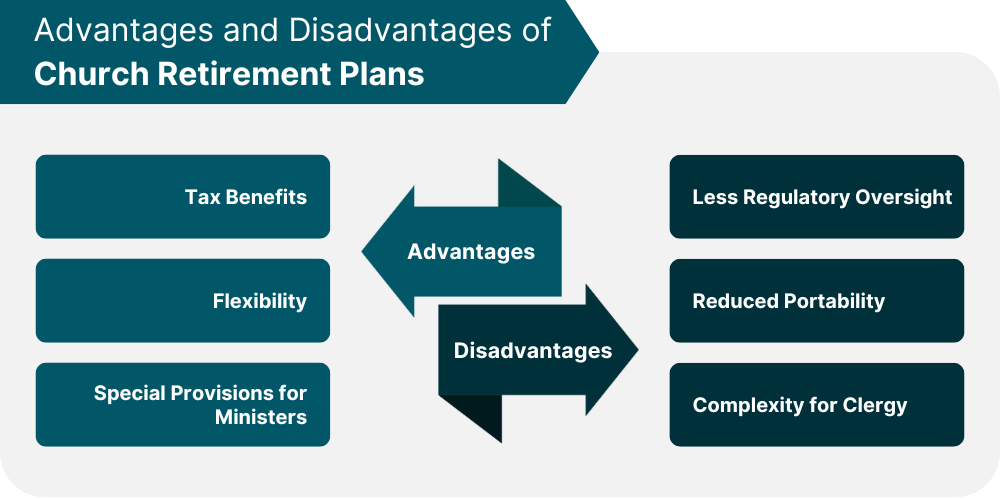

Advantages of Church Retirement Plans

Tax Benefits

Flexibility

Special Provisions for Ministers

Disadvantages of Church Retirement Plans

Less Regulatory Oversight

Reduced Portability

Complexity for Clergy

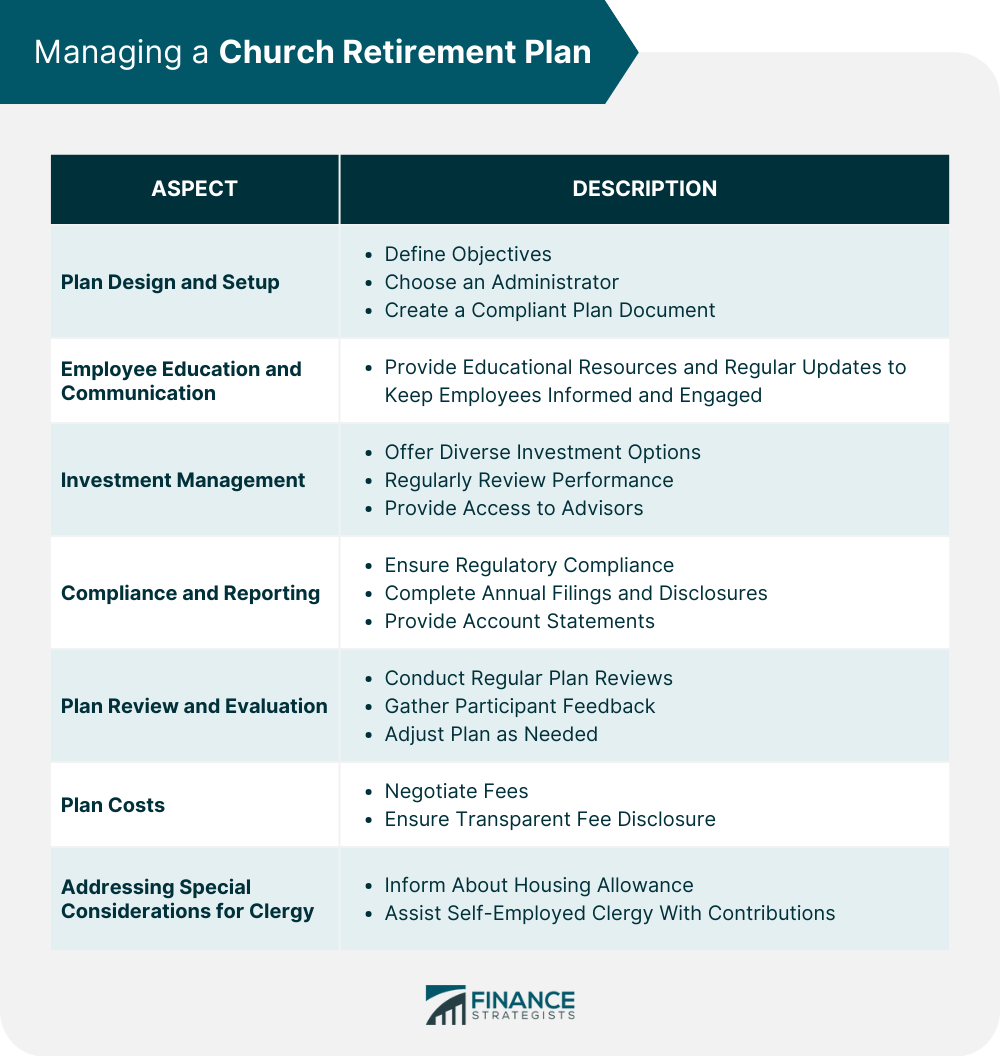

Managing a Church Retirement Plan

Plan Design and Setup

Employee Education and Communication

Investment Management

Compliance and Reporting

Plan Review and Evaluation

Managing Plan Costs

Addressing Special Considerations for Clergy

Final Thoughts

Church Retirement Plan FAQs

Also known as a 403(b)(9) plan, it is a retirement savings plan for church employees, offering tax-deferred contributions and special provisions for clergy.

Clergy and lay employees of religious organizations, including affiliated schools and hospitals, may participate in these plans.

Contributions are tax-deferred, and clergy can designate part of their distributions as a tax-free housing allowance.

Options typically include mutual funds, annuities, index funds, and target-date funds.

It lowers administrative costs but offers fewer participant protections, requiring careful plan management.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.