SEP IRAs and traditional IRAs are two pillars of retirement planning, each with unique features suited to different financial situations. SEP IRAs are favored by self-employed professionals and small business owners for their higher contribution limits and straightforward maintenance. This type of IRA allows these individuals to save significantly more for retirement compared to traditional IRAs. Traditional IRAs, accessible to most earners, are known for their tax-deferred growth, allowing investors to pay taxes on their savings only when they make withdrawals in retirement. This feature makes traditional IRAs a popular choice for long-term savings, providing tax relief in the present while securing funds for the future. Each account type has eligibility criteria, tax implications, and contribution limits that cater to different financial goals and life stages. For those with a SEP IRA, considering a rollover to a traditional IRA involves weighing these differences carefully to ensure the move aligns with their retirement strategy. Moving funds from a SEP IRA to a traditional IRA is not only possible, but can be a smart financial move under the right circumstances. This rollover allows individuals to streamline their retirement savings into one account, making it easier to manage and potentially opening up more diverse investment options. However, this decision should be made with a full understanding of both IRA types. For instance, while a traditional IRA may offer more flexibility in investment choices, it comes with lower annual contribution limits compared to a SEP IRA. When considering a rollover, it's important to factor in your current financial situation, future income expectations, and retirement goals. A rollover can be a strategic move for simplifying your retirement portfolio, but it's crucial to understand what you might be giving up in terms of SEP IRA benefits, such as the ability to save more money annually. Consulting with a financial advisor can provide clarity and personalized guidance for this decision. Before embarking on a rollover, confirming that you are eligible to move funds from your SEP IRA to a traditional IRA is a key first step. This involves understanding any rules or restrictions specific to your SEP IRA. For example, some plans may have stipulations regarding the timing of rollovers or may require certain conditions to be met before funds can be moved. Ensuring that these criteria are met is essential to avoid complications during the rollover process. It's also important to consider the timing of your rollover in relation to other financial events in your life. For example, if you have recently made another IRA rollover, IRS rules might limit your ability to roll over your SEP IRA immediately. Understanding these eligibility nuances is crucial for a smooth and compliant rollover process. Selecting the right traditional IRA provider is a decision that should be made with careful consideration of several factors. Investment options, account fees, and the quality of customer service are all important elements to evaluate. Some providers may offer a wider range of investment choices, which can be crucial for tailoring your portfolio to your specific financial goals. Others might provide more competitive fee structures, which can have a significant impact on your savings over time. When choosing a provider, it’s also wise to consider the ease of account management. Some providers offer robust online platforms and tools that can help you track your investments and make changes to your portfolio as needed. Researching and comparing providers or seeking advice from a financial advisor can help ensure that you select a provider that best meets your retirement planning needs. Informing your SEP IRA custodian of your decision to rollover funds is an essential step in the process. This notification is not just a courtesy; it is a necessary part of initiating the rollover. Your custodian can provide valuable information about the specific requirements and procedures for moving your funds. They can also assist with any paperwork or documentation needed for the rollover. This step is also an opportunity to ask questions and clarify any uncertainties you may have about the rollover process. Your custodian can offer guidance on topics such as potential fees, the timeline for the rollover, and how to handle any tax implications. Clear communication with your custodian can help ensure that the rollover goes smoothly. Filling out the rollover request form is a critical step in the rollover process. This form, which is typically straightforward, must be completed with accuracy to ensure that your funds are properly transferred. It will include essential details like the amount you are rolling over and the specifics of the receiving traditional IRA account. Attention to detail is key when completing this form. Even small errors, such as a mistyped account number or incorrect rollover amount, can lead to delays or complications. Taking the time to review the form carefully before submitting it can help prevent these issues. You have two options for transferring your funds: a direct rollover or an indirect rollover. A direct rollover is typically the safer and simpler choice, as it involves moving your funds directly from your SEP IRA to your traditional IRA without them passing through your hands. This method minimizes the risk of incurring any taxes or penalties, as the funds are never considered to be in your possession. An indirect rollover, on the other hand, involves the funds being paid to you first before you deposit them into your traditional IRA. This method requires strict adherence to IRS guidelines, including depositing the funds into your new IRA within 60 days. Failure to comply with these rules can result in significant tax liabilities and penalties. Regardless of the method you choose for your rollover, it’s important to accurately report the transaction on your tax returns. A direct rollover typically doesn’t trigger immediate tax consequences, but it still needs to be reported to the IRS. This ensures that the IRS is aware that the funds were moved in a compliant manner and are not subject to early withdrawal penalties. For an indirect rollover, careful reporting is even more crucial. If you receive the funds directly, the IRS considers this a distribution, and you must report it as such on your taxes. To avoid taxes and penalties, you must also provide proof that you deposited the funds into your new IRA within the 60-day window. Proper documentation and accurate reporting are key to avoiding problems with the IRS. Consolidating your retirement savings by rolling over a SEP IRA into a Traditional IRA can make managing your retirement funds simpler and more efficient. With all your funds in one account, it’s easier to track your investment performance and make informed decisions about your retirement strategy. This consolidation can also make it easier to adjust your investment allocations as your financial goals and needs evolve over time. In addition to simplifying management, consolidation can also provide a clearer picture of your overall retirement readiness. It’s easier to assess whether you are on track to meet your retirement goals when all your savings are in one place. This clarity can be invaluable in making strategic decisions about contributions, investments, and withdrawals as you approach retirement. One of the key benefits of a traditional IRA is the potential access to a wider range of investment options. While SEP IRAs typically offer a decent selection of investment choices, traditional IRAs often provide an even broader array of options, including individual stocks, bonds, mutual funds, and exchange-traded funds (ETFs). This diversity can be crucial for building a retirement portfolio that is tailored to your specific risk tolerance and investment goals. Having access to a wider variety of investment options also allows for greater flexibility in adapting your investment strategy over time. As market conditions change and as you get closer to retirement, the ability to adjust your portfolio can be a significant advantage. This flexibility can help you maximize your investment returns while managing risk in a way that aligns with your overall retirement plan. Rolling over your SEP IRA into a traditional IRA can simplify both your tax situation and your overall retirement planning. Managing a single IRA simplifies the process of calculating and making annual contributions, tracking investment growth, and planning for future withdrawals. This simplicity can be a significant benefit, particularly as you approach retirement and begin to focus more on income planning and tax efficiency. From a tax planning perspective, consolidating your accounts can make it easier to understand your future tax liabilities. Since withdrawals from a traditional IRA are taxed as ordinary income, having a single account can simplify the process of estimating your tax burden in retirement. This clarity can be extremely helpful in planning for a financially secure retirement. Another advantage of consolidating your SEP IRA into a traditional IRA is the potential to reduce the fees and expenses associated with maintaining multiple retirement accounts. Some IRA providers offer lower fees for accounts with higher balances, so consolidating your funds into a single account could qualify you for these reduced rates. Over time, lower fees can result in significant savings, allowing more of your money to stay invested and grow. In addition to potentially lowering account fees, having a single IRA can also reduce transaction and management fees. Fewer accounts mean fewer transactions and adjustments, which can translate into lower costs. These savings can compound over time, potentially adding a significant amount to your retirement savings. While rolling over a SEP IRA to a traditional IRA has its advantages, it’s important to consider what you might be giving up. SEP IRAs offer unique features that are particularly beneficial for self-employed individuals and small business owners. For example, SEP IRAs allow for significantly higher annual contributions compared to traditional IRAs. This can be a major advantage for those who wish to save aggressively for retirement. Additionally, SEP IRAs often have more lenient rules regarding contributions, providing flexibility for business owners who may have variable incomes. By moving funds to a traditional IRA, you may lose these benefits, which could impact your ability to maximize your retirement savings. Furthermore, SEP IRAs are often praised for their simplicity, especially in terms of setup and maintenance, which is particularly appealing to small business owners who may not have extensive financial resources. By rolling over to a traditional IRA, you might encounter a more complex set of rules and requirements, which could potentially add to the administrative burden of managing your retirement savings. Engaging in a rollover from a SEP IRA to a traditional IRA without fully understanding the tax implications can lead to unexpected financial consequences. It's essential to be aware that while direct rollovers are usually non-taxable events, indirect rollovers, if not handled correctly, can incur taxes. If the funds from an indirect rollover are not deposited into the new IRA within the 60-day window, the amount is treated as a taxable distribution. This can significantly increase your tax liability for the year. Moreover, if you are under the age of 59½, not only could the amount be subject to regular income tax, but it might also be hit with a 10% early withdrawal penalty. These potential tax consequences underscore the importance of understanding the rollover rules and considering the timing of your rollover, especially if you are considering an indirect rollover. The IRS imposes certain limitations on IRA rollovers that are crucial to understand. One key limitation is the one-rollover-per-year rule, which states that you can only perform one IRA-to-IRA rollover in a 12-month period. This rule applies across all your IRAs, not just per account, so if you have already completed a rollover within the past year, you may need to wait before you can rollover your SEP IRA. Additionally, while most SEP IRA funds are eligible for rollover, there may be specific restrictions or conditions based on your plan's rules. Overlooking these limitations can result in unintended consequences, such as taxes and penalties, or the rollover being disallowed. Understanding these limitations is crucial to ensure that your rollover is compliant with IRS regulations and achieves your intended financial goals. Incorrectly executing a rollover from a SEP IRA to a traditional IRA can inadvertently trigger early withdrawal penalties, particularly in the case of indirect rollovers. If the rollover is not completed within the IRS's strict 60-day window, the funds could be considered an early distribution, subject to taxes and potentially a 10% penalty if you are under 59 ½. These penalties can significantly reduce the value of your retirement savings. Therefore, it's crucial to plan the rollover carefully and understand the rules fully. Opting for a direct rollover, where the funds are transferred directly between the financial institutions, can help avoid these risks, as it eliminates the possibility of missing the 60-day deadline. When considering a rollover from a SEP IRA to a traditional IRA, it's vital to assess any immediate tax implications. Typically, a direct rollover is a non-taxable event, as the funds are transferred directly from one account to another without being paid to you first. However, with an indirect rollover, where you receive the funds and then deposit them into the new IRA, there are potential tax consequences if not completed correctly. If the funds from an indirect rollover are not deposited into the new IRA within the required 60-day period, the distribution becomes taxable. Additionally, if you withhold any taxes from the distribution, you must deposit the full amount of the original distribution into the new IRA to avoid taxes and penalties. Understanding these nuances is essential for a tax-efficient rollover process. The rollover of a SEP IRA into a traditional IRA also has implications for your future tax situation. It’s important to remember that while funds in a traditional IRA grow tax-deferred, withdrawals in retirement are taxed as ordinary income. This means that the tax rate applicable to your withdrawals could be different from your current tax rate, depending on your income level at the time of retirement. Considering the future tax implications is crucial when deciding whether a rollover is in your best financial interest. It’s important to think about your anticipated income in retirement and how it will affect your tax bracket. This foresight can help in planning effective retirement income strategies that maximize your savings and minimize your tax liabilities. Accurately reporting a rollover from a SEP IRA to a traditional IRA on your tax return is essential. For direct rollovers, this typically involves indicating on your tax forms that the rollover occurred but was not a taxable event. For indirect rollovers, it's necessary to report the distribution and then show that it was rolled over into another IRA within the allowable 60-day period. Proper reporting ensures that the IRS recognizes the rollover as a legitimate, non-taxable event. Failing to report the rollover correctly can lead to misunderstandings with the IRS, potentially resulting in unnecessary taxes and penalties. Keeping accurate records of the rollover and seeking guidance from a tax professional can help ensure that your tax filings are correct and compliant. In addition to federal taxes, state tax considerations may also play a role in your rollover decision. Each state has its own tax laws regarding IRA distributions and rollovers, which can vary significantly. Some states may offer tax deductions or exemptions for IRA contributions or rollovers, while others may impose additional taxes or have different reporting requirements. Understanding the state tax implications of a rollover is important, especially if you live in a state with unique tax laws regarding retirement accounts. Consulting with a tax advisor who is knowledgeable about your state’s specific tax regulations can provide valuable insights and help you make a more informed decision about your rollover. One of the most critical rules to adhere to when conducting an indirect rollover is the 60-day rollover rule. Failing to deposit the funds into a new IRA within this timeframe can result in the entire amount being treated as a taxable distribution. This can lead to a significant and unexpected tax bill, especially if the amount is substantial. To avoid this costly mistake, it’s advisable to plan the rollover carefully and begin the process well before the 60-day deadline. If possible, consider a direct rollover instead, as it eliminates the risk of missing the deadline and ensures a smoother and safer transfer of funds. A common pitfall in the rollover process is not fully understanding the tax implications. This lack of understanding can lead to unexpected tax liabilities and penalties. It’s crucial to be aware of both the immediate and future tax consequences of a rollover, including how it might affect your taxable income and retirement withdrawals. To avoid unpleasant surprises, thoroughly research the tax rules surrounding rollovers or consult with a tax professional. This step can provide clarity on how a rollover will impact your tax situation and help you make an informed decision that aligns with your financial goals. Overlooking the eligibility criteria for a rollover can lead to complications and potential penalties. It's important to be aware of restrictions that may apply to your SEP IRA, as well as IRS rules, such as the one-rollover-per-year limit. Failing to meet these criteria can result in the rollover being disallowed or treated as a taxable distribution. Before initiating a rollover, review your SEP IRA’s terms and conditions and familiarize yourself with relevant IRS regulations. Understanding these rules and ensuring that you are eligible for the rollover is key to avoiding mistakes that could hinder your retirement savings. Incorrectly filling out rollover forms is a common error that can delay or even derail the rollover process. Mistakes such as entering the wrong account numbers, misspelling names, or providing incorrect rollover amounts can lead to significant delays and complications. To prevent these issues, take the time to carefully review and double-check all information on the rollover forms. Ensuring accuracy in every detail is crucial for a smooth transfer of funds. If you’re uncertain about any part of the form, don’t hesitate to reach out to your financial institution or custodian for assistance. For those who value the unique features of a SEP IRA, such as higher contribution limits, maintaining separate IRA accounts might be a preferable option. Keeping your SEP IRA intact while also contributing to a traditional IRA can provide a diversified approach to retirement savings. This strategy allows you to leverage the benefits of both account types, although it does require careful management of multiple accounts. Maintaining separate accounts can be particularly beneficial if your income varies from year to year, as it allows you to maximize contributions to your SEP IRA in high-income years while still building savings in a traditional IRA. However, managing multiple accounts does require a higher level of organization and attention to ensure that contribution limits and tax implications are properly handled. Converting your SEP IRA to a Roth IRA is another alternative to consider. Unlike a traditional IRA, Roth IRAs are funded with after-tax dollars, which means that contributions are not tax-deductible. However, the advantage of a Roth IRA is that your investments grow tax-free, and qualified withdrawals in retirement are not subject to income tax. A Roth IRA conversion can be particularly advantageous if you expect to be in a higher tax bracket in retirement, as it allows you to pay taxes at your current lower rate. However, it's important to consider the tax implications of the conversion, as the amount converted will be treated as taxable income in the year of the conversion. This strategy requires careful planning to determine if the potential long-term tax benefits outweigh the immediate tax costs. Additionally, Roth IRAs offer more flexibility with withdrawals and are not subject to Required Minimum Distributions (RMDs), making them an attractive option for many retirees. Another alternative to consider is contributing to or rolling over funds into an employer-sponsored retirement plan, such as a 401(k), if available. These plans often come with the benefit of employer matching contributions, which can significantly enhance your retirement savings. Employer-sponsored plans also typically offer a range of investment options and can be a convenient way to save for retirement directly from your paycheck. Additionally, if you have a high income, participating in an employer-sponsored plan might allow you to save more for retirement than you could with an IRA alone due to higher contribution limits. However, it's important to compare the investment options and fees in your employer's plan with those in IRAs to ensure you're making the best choice for your financial situation. Exploring non-retirement investment options, such as taxable brokerage accounts or real estate, is another strategy to complement your retirement savings. While these options don't offer the same tax advantages as IRAs, they provide greater flexibility in terms of access to funds and a wider range of investment choices. Taxable accounts allow for more diverse investment strategies, such as capital gains harvesting or tax-loss selling, which can be advantageous in certain financial situations. Real estate investments can provide a source of passive income and potential appreciation in value. Diversifying your investment portfolio with these options can be a valuable part of a comprehensive retirement strategy, offering flexibility and potential growth outside of traditional retirement accounts. Rolling over a SEP IRA into a traditional IRA can be a strategic move for streamlining retirement savings, offering potential benefits like a broader range of investment options and simplified tax planning. However, it's crucial to consider the drawbacks, such as the loss of SEP IRA's higher contribution limits and possible tax consequences. The rollover process demands careful attention to eligibility, correct execution of forms, and adherence to IRS rules, especially the 60-day rule for indirect rollovers. Alternatives like maintaining separate IRA accounts, converting to a Roth IRA, or exploring non-retirement investment options should also be weighed. Ultimately, a rollover decision should align with your long-term retirement goals and financial situation, possibly necessitating advice from a financial advisor.

Brief Overview of SEP IRAs and Traditional IRAs

Can You Rollover a SEP IRA Into a Traditional IRA?

Rollover Process From a SEP IRA to a Traditional IRA

Step 1: Determine Eligibility for the Rollover

Step 2: Choose a Traditional IRA Provider

Step 3: Notify Your SEP IRA Custodian

Step 4: Complete the Rollover Request Form

Step 5: Transfer Funds Directly or Indirectly

Step 6: Report the Rollover on Taxes

Advantages of a SEP IRA to Traditional IRA Rollover

Consolidation of Retirement Funds

Potential for Better Investment Options

Simplification of Tax and Retirement Planning

Possible Lower Fees and Expenses

Disadvantages of a SEP IRA to Traditional IRA Rollover

Loss of the Unique Features of a SEP IRA

Potential Tax Consequences

Rollover Limitations

Possible Early Withdrawal Penalties

Tax Implications and Reporting in a SEP IRA to Traditional IRA Rollover

Assessing Immediate Tax Implications

Understanding Future Tax Impacts

IRS Reporting Requirements

State Tax Considerations

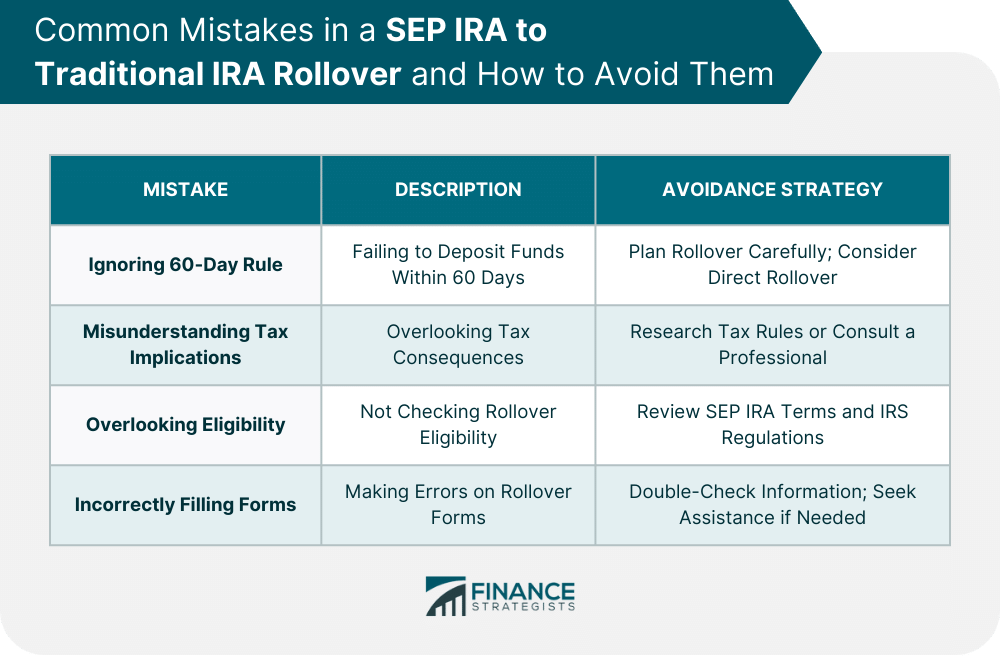

Common Mistakes in a SEP IRA to Traditional IRA Rollover and How to Avoid Them

Failing to Adhere to the 60-Day Rollover Rule

Not Understanding Tax Implications

Overlooking Rollover Eligibility Criteria

Incorrectly Filling Out Forms

Alternatives to a SEP IRA to Traditional IRA Rollover

Maintaining Separate IRA Accounts

Converting to a Roth IRA

Employer-Sponsored Retirement Plans

Non-retirement Investment Options

Final Thoughts

Can You Rollover a SEP IRA Into a Traditional IRA? FAQs

Yes, you can rollover a SEP IRA into a traditional IRA without incurring immediate taxes, especially if you opt for a direct rollover where funds are transferred between institutions.

To roll over a SEP IRA into a traditional IRA, determine your eligibility, choose a traditional IRA provider, notify your SEP IRA custodian, complete the rollover request form, and decide on a direct or indirect transfer of funds.

While you can rollover a SEP IRA into a traditional IRA more than once, remember that IRS rules limit you to one rollover per year across all your IRAs.

Generally, there are no penalties or fees for rolling over a SEP IRA into a traditional IRA if you follow the correct process, particularly for a direct rollover.

Before you rollover a SEP IRA into a traditional IRA, consider factors like the differences in investment options, the impact on your retirement strategy, and the potential loss of SEP IRA's unique features, such as higher contribution limits.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.