An IRA to 401(k) rollover refers to the process of transferring your retirement savings from an Individual Retirement Account (IRA) to a 401(k) plan, typically one offered by your employer. It's a strategic move aimed at consolidating your retirement savings into a single plan, which could offer more flexibility, potentially lower fees, or other advantages depending on your circumstances.

There are several reasons why someone might consider performing an IRA to 401(k) rollover. They might wish to consolidate their retirement accounts for easier management or to access specific investment options offered by their 401(k) plan. A rollover might also be beneficial for someone considering a backdoor Roth IRA contribution who wants to avoid the pro-rata rule. Both IRA and 401(k) are tax-advantaged retirement savings vehicles, but they come with different rules. An IRA is a type of account you open on your own, whereas a 401(k) is sponsored by an employer. While both offer tax deductions on contributions, the contribution limit for a 401(k) is significantly higher than for an IRA. Not everyone is eligible for an IRA to 401(k) rollover. Generally, you must have a 401(k) plan with an employer that accepts such rollovers. Additionally, the funds in your IRA must be eligible for rollover, which generally means they were contributed to the IRA through a previous 401(k) rollover or as direct contributions. The IRS has specific rules regarding rollovers. For instance, you can only do one IRA-to-IRA rollover per 12 months, but you can do unlimited trustee-to-trustee transfers. This rule doesn't apply to rollovers from an IRA to a 401(k). An IRA to 401(k) rollover is generally a tax-free process if executed correctly. It's vital to opt for a direct rollover or trustee-to-trustee transfer to avoid any tax implications. Otherwise, the distribution could be subject to mandatory withholding. The first step in executing a rollover is to contact your 401(k) plan administrator. They can confirm whether your plan accepts rollover contributions and guide you through the process. While many 401(k) plans allow rollovers, not all do. You need to confirm this with your plan administrator. It's also essential to check if your 401(k) plan accepts both pre-tax and after-tax contributions if you have a traditional and a Roth IRA. Once you confirm that your 401(k) accepts rollovers, you can request your IRA custodian to start the process. You'll need to specify how much you want to roll over and provide the details of your 401(k) plan. After initiating the rollover, you need to follow up with both your 401(k) plan and your IRA custodian to ensure the funds are transferred correctly. This usually takes a few weeks. One of the major advantages of 401(k) plans is that they often provide access to institutional funds that may not be available to individual investors. These funds often come with lower expense ratios than similar funds available to individuals. Unlike IRAs, 401(k)s often offer the ability to take out loans against your retirement savings. While this should be a last resort, it can provide a safety net in case of financial emergencies. Federal law provides robust protection to 401(k) assets against creditors. IRAs also offer some protection, but the level of protection varies by state and may not be as strong as the protection offered to 401(k)s. If you are still working and don't own 5% or more of the business you work for, you can delay taking required minimum distributions (RMDs) from your current employer's 401(k) beyond age 73. This rule doesn't apply to IRAs or 401(k)s from previous employers. While 401(k)s often provide access to unique institutional funds, they typically have a more limited range of investment options than IRAs. If you like having a wide array of investment choices, this could be a drawback. 401(k)s often have stricter rules for withdrawals before age 59 ½ compared to IRAs. If you anticipate needing to access your savings early, this could be a potential disadvantage. Some IRA custodians may charge fees for transferring out funds. Make sure to check with your IRA custodian to see if this applies. Deciding on an IRA to 401(k) rollover is a personal decision that should be tailored to fit your unique financial situation and long-term retirement goals. Your overall financial plan, inclusive of your risk tolerance, investment preference, and projected retirement lifestyle, should guide this decision. For some individuals, consolidating multiple retirement accounts into a singular 401(k) plan provides convenience and a simplified way to manage their retirement savings. This ease of access can prove invaluable, allowing for streamlined management and monitoring of investment growth. Furthermore, a 401(k) plan may offer unique investment options not readily available in an IRA, presenting an opportunity to diversify your portfolio and potentially enhance your returns. For individuals contemplating a backdoor Roth contribution, an IRA to 401(k) rollover can be a smart strategy to circumvent the pro-rata rule, thus optimizing their tax situation. Additionally, if creditor protection is a significant concern, a 401(k) offers more robust security compared to an IRA, which could be a compelling reason to consider the rollover. Ultimately, the decision should align with your financial objectives, warranting careful deliberation or consultation with a financial advisor. Keep the IRA as It Is: If you're satisfied with your IRA's investment options and fees, it might make sense to keep things as they are. Transfer to a Different IRA: If you're unhappy with your IRA but don't want to roll it into a 401(k), another option is to roll it over into another IRA. This could provide a wider array of investment options and potentially lower fees. Convert to a Roth IRA: If you anticipate being in a higher tax bracket in retirement, you might consider converting your traditional IRA into a Roth IRA. This option involves paying taxes on your savings now so you can withdraw them tax-free in retirement. Understanding your retirement savings options is crucial for ensuring a secure financial future. An IRA to 401(k) rollover offers an excellent means to consolidate your accounts, access unique investment opportunities, and potentially gain superior creditor protection. However, this process is not for everyone. Depending on your circumstances and the specifics of your 401(k) plan, it could limit your investment choices or result in stricter withdrawal rules. It's also essential to remember that an improperly executed rollover could lead to unnecessary taxes or penalties. As such, it's always wise to consult with a financial advisor or tax professional before initiating a rollover. When considering an IRA to 401(k) rollover, it's crucial to compare it to other options like keeping the IRA, transferring to a different IRA, or converting to a Roth IRA.Overview of IRA to 401(k) Rollover

Definition of an IRA to 401(k) Rollover

Reasons to Consider a Rollover

Brief Comparison Between IRA and 401(k)

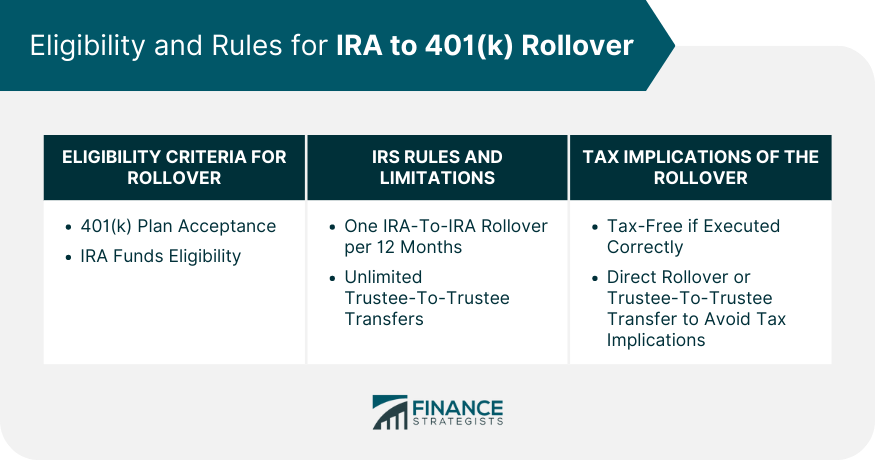

Eligibility and Rules for IRA to 401(k) Rollover

Eligibility Criteria for Rollover

Legal Limitations and IRS Rules

Tax Implications of the Rollover

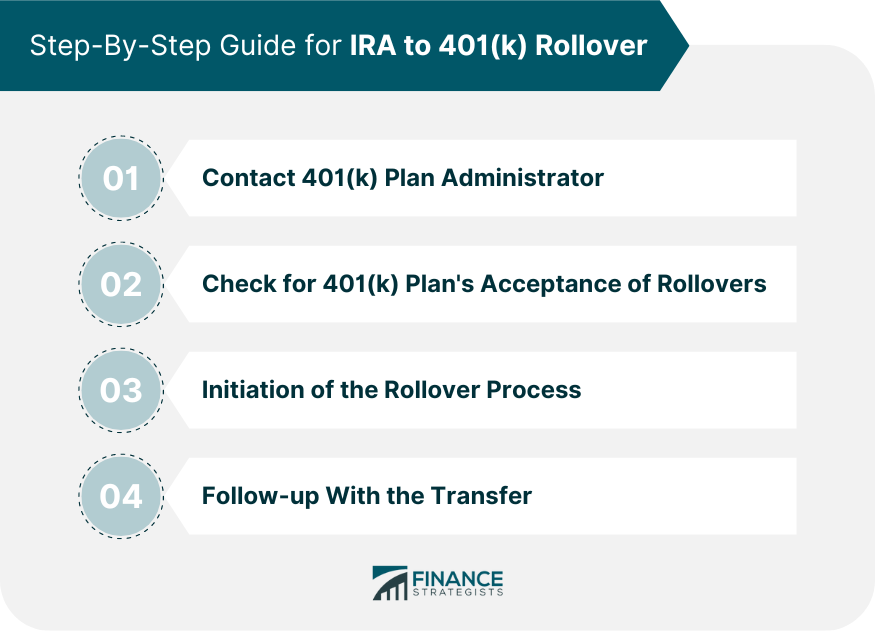

Step-By-Step Guide for IRA to 401(k) Rollover

Contact 401(k) Plan Administrator

Check for 401(k) Plan's Acceptance of Rollovers

Initiation of the Rollover Process

Follow-up With the Transfer

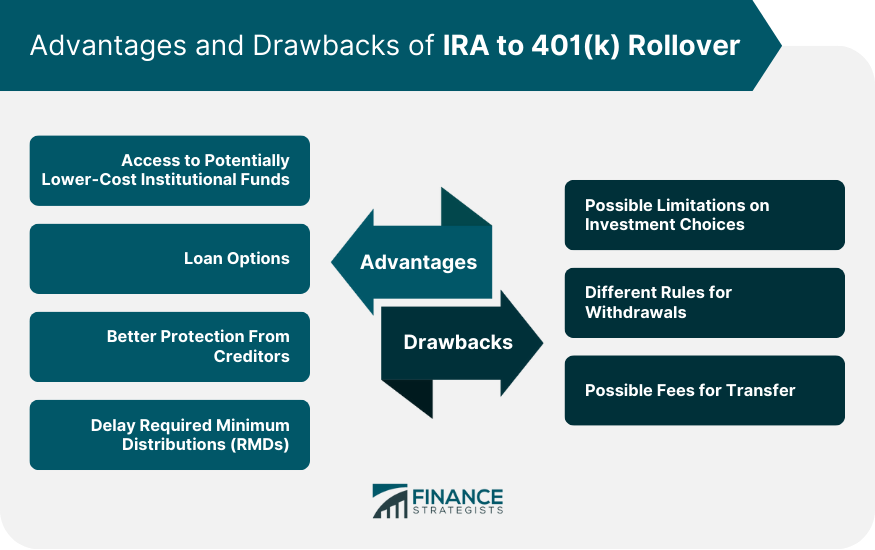

Advantages of IRA to 401(k) Rollover

Access to Potentially Lower-Cost Institutional Funds

Loan Options

Better Protection From Creditors

Delay Required Minimum Distributions (RMDs)

Drawbacks of IRA to 401(k) Rollover

Possible Limitations on Investment Choices

Different Rules for Withdrawals

Possible Fees for Transfer

When an IRA to 401(k) Rollover Makes Sense

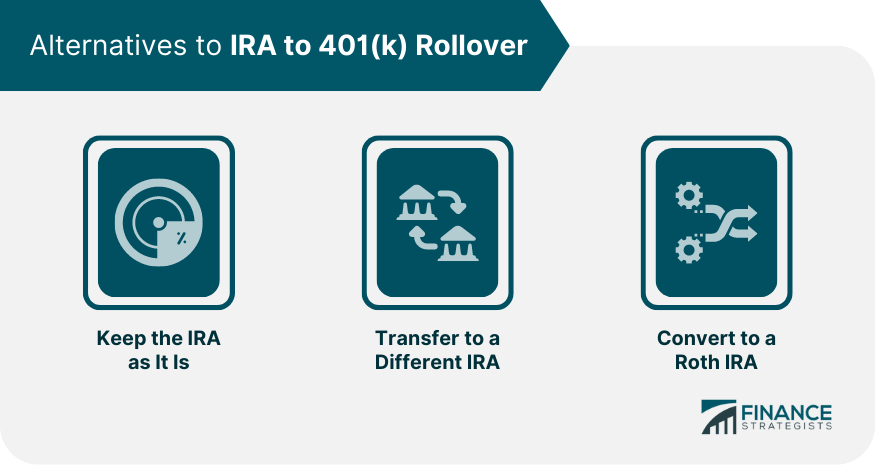

Alternatives to IRA to 401(k) Rollover

Bottom Line

IRA to 401(k) Rollover FAQs

You can perform an IRA to 401(k) rollover if you meet certain conditions, like having a 401(k) plan that accepts rollovers and having rollover-eligible funds in your IRA. Additionally, be aware of IRS rules on rollovers to ensure you don't inadvertently trigger taxes or penalties.

If executed properly, an IRA to 401(k) rollover should not incur any taxes or penalties. However, an indirect rollover, where you receive the funds and then deposit them into the 401(k), could lead to mandatory withholding. To avoid this, it's best to opt for a direct, trustee-to-trustee rollover.

Typically, a 401(k) offers a more limited range of investment options compared to an IRA. However, 401(k) plans often provide access to institutional funds not usually available to individual investors, which may come with lower expense ratios.

Yes, an IRA to 401(k) rollover does not affect your ability to contribute to your 401(k). You can continue making contributions up to the annual limit set by the IRS.

If your 401(k) plan does not accept rollovers, you have a few options. You can keep your funds in the IRA, consider rolling over to another IRA with better investment options or lower fees, or look into converting your traditional IRA into a Roth IRA. Each option has its own set of considerations, so it's important to evaluate each in light of your personal circumstances.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.