There's a dizzying array of retirement savings options available to the modern worker. Some are tied to specific employment types, while others are available to virtually everyone. These options, ranging from employer-sponsored plans to individual accounts, provide different benefits depending on your financial and life circumstances. Navigating the retirement planning landscape can be challenging. Yet, understanding each option's nuances is crucial, especially when considering long-term financial health. The right retirement plan can ensure financial security in your golden years, while the wrong one might leave you scrambling. Each retirement plan has distinct rules, benefits, and drawbacks. Tax benefits might favor higher earners in one plan, while another offers withdrawal flexibility. Understanding these differences allows individuals to align their retirement strategies with their life goals and craft a tailored plan. A 457(b) plan is not an IRA. A 457(b) plan is a type of non-qualified, tax-advantaged deferred-compensation retirement plan available for certain governmental and non-governmental employers. In contrast, an IRA (Individual Retirement Account) is a tax-advantaged account that individuals set up independently to save for retirement. A 457(b) plan is often associated with public sector employees, such as those working for the government. It's a type of deferred compensation retirement plan akin to the more widely known 401(k) plans found in the private sector. These plans originated to provide government workers with a way to save for retirement, given that their employment settings often differed from the corporate world. Over time, the 457(b) plan has evolved, seeing updates and changes in regulations. The core premise remains the same: allowing eligible employees to put away money for their retirement, often with the benefit of matching contributions from their employer. Unlike some retirement plans, 457(b) plans are exclusive to certain types of employees. Typically, state and local governmental employees, as well as certain non-profit workers, can access these plans. However, not every such employee will have access, as it depends on the employer's offerings. In terms of beneficiaries, things are straightforward. If an employee with a 457(b) account passes away, the funds in that account will typically go to the named beneficiaries, which can be updated and changed as life circumstances evolve. Individual Retirement Accounts, commonly known as IRAs, are tax-advantaged savings accounts designed for retirement. There are primarily two types: Traditional and Roth. A Traditional IRA offers tax breaks on the money you contribute, but withdrawals during retirement are taxed. Roth IRAs, conversely, are funded with after-tax money, meaning withdrawals during retirement are generally tax-free. The distinction between the two primarily hinges on when you prefer to get your tax break: now (Traditional) or during retirement (Roth). Both types have their unique advantages, and the best choice often depends on your current financial situation and future predictions. IRAs came into existence with the Employee Retirement Income Security Act of 1974. Their primary goal was to provide retirement savings options for those who didn't have access to employer-sponsored plans. Since then, IRAs have become a cornerstone of retirement planning in the U.S. The benefits of an IRA are numerous. They offer tax advantages, either upon contribution or withdrawal, depending on the type. Additionally, IRAs usually offer a broader range of investment options compared to employer-sponsored plans. This flexibility can be especially advantageous for those who want more control over their retirement investments. One of the primary benefits of the 457(b) plan is the generous contribution limit. As with many retirement plans, these limits are periodically adjusted for inflation. In 2024, individuals can contribute up to $23,000 ($23,500 in 2025) annually to a 457(b) plan, encompassing both contributions from the employee and the employer. However, it's uncommon for employers to contribute to 457(b) plans. For those 50 years of age and above, an extra contribution of $7,500 is permissible, raising the total allowable contribution to $30,500 for 2024 and $31,000 for 2025. Participants can contribute a significant portion of their salary, and those closer to retirement age may have the opportunity to contribute even more through catch-up contributions. However, these benefits come with a caveat: exceeding the contribution limits can lead to penalties. Thus, it's crucial for plan participants to be vigilant and stay informed about the current limits. 457(b) plans are unique when it comes to withdrawals. Unlike many other retirement plans, 457(b) plans don't penalize participants for withdrawing funds before a certain age. This feature is especially advantageous for those who might consider early retirement. However, there are still rules governing withdrawals. For instance, while there isn't an early withdrawal penalty, distributions are still subject to ordinary income tax. Additionally, certain circumstances might necessitate a required minimum distribution, affecting the withdrawal strategy. Just like 401(k) plans, 457(b) contributions are made with pre-tax dollars. This means that contributions reduce your taxable income for the year, providing immediate tax relief. Upon withdrawal, these distributions are taxed as ordinary income. This pre-tax benefit can be quite impactful, especially for those in higher tax brackets. By lowering taxable income, participants can sometimes reduce their overall tax liability, maximizing their yearly take-home pay while also preparing for the future. Perhaps the most notable feature of the 457(b) plan, distinguishing it from IRAs and even 401(k) plans, is the lack of an early withdrawal penalty. While most retirement plans penalize withdrawals made before age 59½, 457(b) plans don't. This flexibility is due to their origin: they were designed for public-sector employees, who often have different retirement trajectories than private-sector workers. Additionally, 457(b) plans allow for simultaneous contributions to other retirement accounts. This means that if an eligible employee also has access to another plan, such as a 403(b), they can contribute the maximum allowable amount to both. Both Traditional and Roth IRAs come with annual contribution limits, which are typically lower than those of many employer-sponsored plans. For 2024 and 2025, individuals below 50 can contribute up to $7,000 to an IRA, while those aged 50 and above have a limit of $8,000. These limits are established by the IRS and can change based on inflation adjustments. It's important to note that these limits apply to the total contributions to all IRAs, not per account. While these limits might seem restrictive, especially when compared to plans like 457(b), the tax benefits often make IRAs a valuable part of a diversified retirement strategy. Additionally, those over age 50 can make additional catch-up contributions, providing an opportunity to boost retirement savings later in life. The primary distinction between Traditional and Roth IRAs lies in their tax treatment. Contributions to a Traditional IRA might be tax-deductible, offering immediate tax relief, but eventual withdrawals in retirement are taxable. Roth IRAs flip this script. Contributions are made with after-tax dollars, but qualified withdrawals during retirement are tax-free. The decision between a Traditional or Roth IRA often hinges on an individual's current tax bracket and predictions about future tax rates. If you anticipate being in a higher tax bracket during retirement, a Roth IRA might be more beneficial. Traditional IRAs come with certain age-related stipulations. For one, you must start taking required minimum distributions (RMDs) by April 1st of the year following the year you turn 73. These distributions are calculated based on life expectancy tables, and failing to take them can result in hefty penalties. Roth IRAs, on the other hand, have no RMDs for the original owner, offering more flexibility in retirement distribution strategies. However, there's an age restriction for contributions: individuals cannot contribute to a Traditional IRA in the year they turn 70½ and onwards, while Roth IRAs have no such restriction. 457(b) plans and IRAs serve different demographics, primarily based on employment type. As mentioned earlier, 457(b) plans are tailored for public sector employees. They cater to those who might have distinct career trajectories, like police officers or firefighters, who might retire earlier than the private-sector workforce. IRAs, meanwhile, are broadly accessible, designed for anyone earning an income. This universal accessibility makes them a favorite among those who might not have access to employer-sponsored plans, including freelancers, self-employed individuals, and those whose employers don't offer retirement benefits. One of the standout features of IRAs, especially when held with major brokerage firms, is the vast array of investment options. Investors can dive into individual stocks, bonds, mutual funds, ETFs, and sometimes even more exotic investment vehicles. 457(b) plans, while offering a range of investment options, might not have the same breadth as IRAs. Typically, these plans offer a curated selection of mutual funds, which can be beneficial for those seeking simplicity but might be limiting for those desiring more investment control. Rollovers refer to the transfer of retirement funds from one account or plan type to another, typically without incurring penalties or taxes. Both 457(b) plans and IRAs offer rollover options, but the rules and conditions vary. For 457(b) plans, rollovers can typically be made to other employer-sponsored plans or to IRAs. However, the receiving plan must accept these funds. IRAs, given their flexibility, can often receive rollovers from a variety of sources, including 457(b) plans, 401(k)s, and other IRAs. Retirement accounts don't just impact the account holder—they can also have significant implications for heirs. Both 457(b) plans and IRAs can be passed to beneficiaries, but the tax and distribution rules vary. For IRAs, especially Roth accounts, the tax-free distribution can be a boon for heirs. However, recent legislation changes have adjusted how beneficiaries must withdraw these funds, potentially affecting tax strategies. 457(b) plans also have specific rules for beneficiary distributions, so careful estate planning is essential to maximize benefits and minimize tax implications. Government entities, including state, local, and some federal agencies, frequently offer 457(b) plans to their employees. These plans are especially common among public safety workers, such as police officers and firefighters, who might have early retirement options. The provision of these plans aligns with the unique career paths and retirement trajectories of public sector workers. As these employees often have pension plans and other retirement benefits, 457(b) plans can serve as an additional layer of savings, offering more financial security. Certain non-profit organizations also offer 457(b) plans, though these are slightly different from the governmental 457(b) plans. They come with distinct rules, especially concerning early withdrawals and rollovers. For employees in the non-profit sector, these plans can be invaluable. They offer a structured way to save for retirement, often complemented by other benefits like pensions or 403(b) plans. Every individual has unique financial goals and needs, especially concerning retirement. For some, a 457(b) plan might be a perfect fit, while others might find more value in an IRA or another retirement option. When assessing a 457(b) plan, consider factors like your current tax bracket, potential employer contributions, and your retirement timeline. If, for instance, early retirement is on the cards, the no-penalty withdrawals of a 457(b) might be especially appealing. Your current tax situation and predictions about future tax rates can significantly influence the best retirement plan for you. If you're in a high tax bracket now and predict lower rates during retirement, the immediate tax savings from a 457(b) or Traditional IRA might be beneficial. Conversely, if you expect higher taxes during retirement, a Roth IRA might be more appealing. Your career path plays a crucial role in retirement planning. For those in the public sector or non-profit organizations with access to a 457(b) plan, this option might be the most advantageous. But if you foresee a career change or move to the private sector, diversifying with an IRA might be prudent. Sometimes, the choice isn't between a 457(b) and an IRA but how to balance multiple retirement options. If, for instance, you have access to both a 457(b) and a 403(b), you might be able to maximize contributions to both, supercharging your retirement savings. Diversification isn't just for your investment portfolio; it's also a smart strategy for retirement accounts. By diversifying between account types, like a 457(b), Traditional IRA, and Roth IRA, you can capitalize on different tax benefits and provide more flexibility in retirement withdrawal strategies. While each account type has its benefits, their combined strengths can offer a robust retirement strategy, ensuring financial stability regardless of future economic or tax scenarios. The financial landscape is ever-changing. Market conditions shift, tax laws get revised, and personal financial situations evolve. Periodically reviewing and adjusting your investment strategy ensures that your retirement savings align with your current goals and the broader financial environment. This might mean rebalancing your portfolio, adjusting contribution amounts, or even rolling over funds from one account type to another. Regularly revisiting your strategy ensures you're on track to meet your retirement objectives. While personal research and education are invaluable, sometimes the expertise of a financial advisor can be beneficial. Complex situations, major life changes, or just a desire for a professional perspective might warrant seeking out advice. An expert can provide clarity, offer tailored strategies, and even highlight opportunities you might have overlooked. Whether it's a one-time consultation or an ongoing relationship, professional financial advice can be a catalyst for optimized retirement savings. In the complex landscape of retirement savings, the 457(b) plan and Individual Retirement Account (IRA) stand out as distinct options with unique advantages. A 457(b) is specifically tailored for public sector employees, allowing them to defer a portion of their salaries for retirement. Originating as a vehicle for government workers, it offers generous contribution limits and the significant advantage of no early withdrawal penalties. On the other hand, IRAs, introduced by the Employee Retirement Income Security Act of 1974, are available to all income earners, providing tax advantages and a broad range of investment choices. The distinction boils down to employment type, investment flexibility, and tax treatments. To directly answer the article's question: No, a 457(b) plan is not an IRA. While both serve as retirement-saving vehicles, they cater to different demographics and have distinct rules and benefits, highlighting the importance of understanding each to ensure optimal long-term financial planning.Overview of Retirement Savings Options

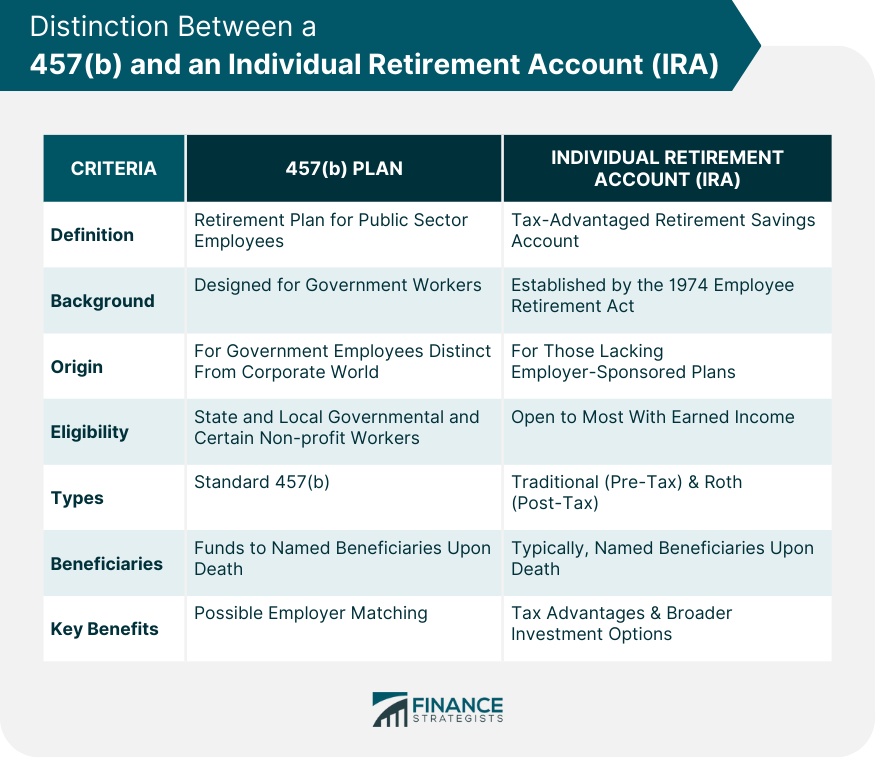

Distinction Between a 457(b) and an IRA

Definition of a 457(b) Plan

Background and Origin

Eligibility and Beneficiaries

Definition of an Individual Retirement Account (IRA)

Types of IRAs: Traditional and Roth

Background and Benefits

Characteristics of 457(b) Plans

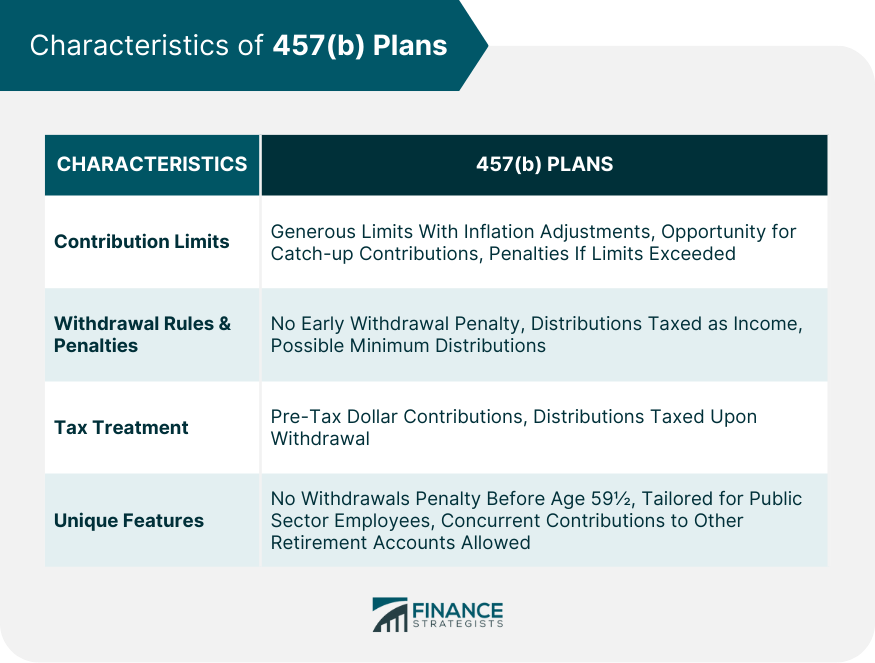

Contribution Limits

Withdrawal Rules and Penalties

Tax Treatment

Unique Features Not Found in IRAs

Characteristics of IRAs

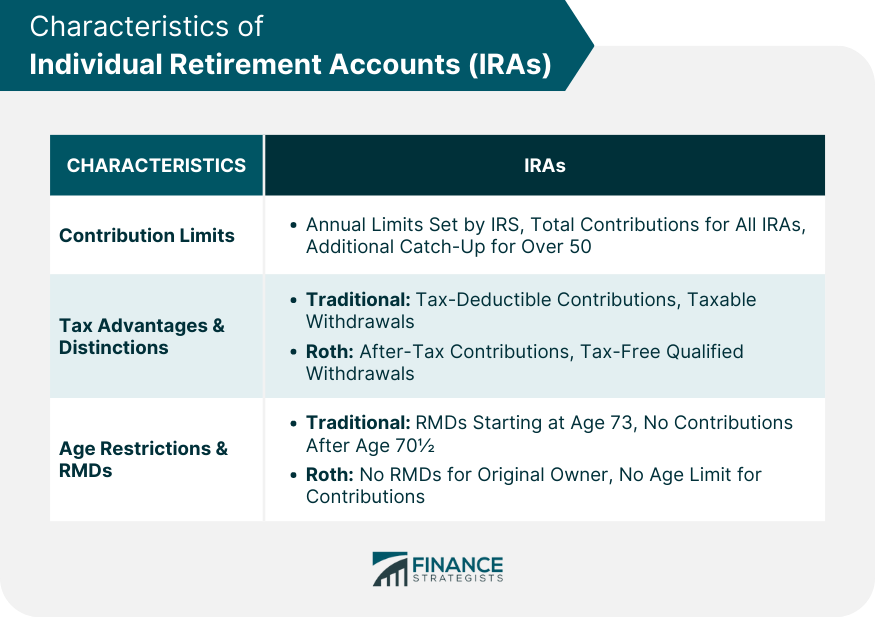

Contribution Limits for Traditional and Roth IRAs

Tax Advantages and Distinctions

Age Restrictions and Required Minimum Distributions (RMDs)

Comparing and Contrasting 457(b) With IRAs

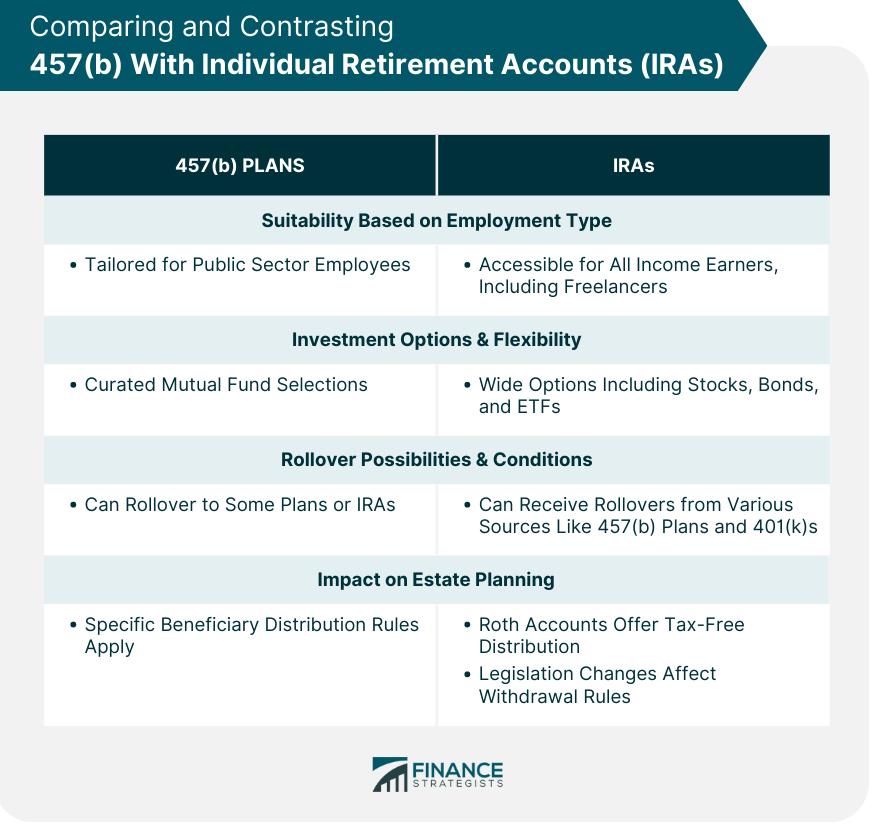

Suitability Based on Employment Type

Investment Options and Flexibility

Rollover Possibilities and Conditions

Impact on Estate Planning

Understanding Eligibility and Suitability for 457(b) Plans

Typical Employers Offering 457(b) Plans

Government Entities

Non-Profit Organizations

Assessing Financial Goals and Needs Against the Plan's Features

Factors Influencing the Choice Between 457(b) and IRAs

Current and Future Tax Scenarios

Expected Employment Trajectory

Availability of Other Retirement Options

Tips for Optimizing Retirement Savings

Diversify Between Different Types of Accounts

Review and Adjust Periodically the Investment Strategies

Seek Professional Financial Advice When Necessary

Bottom Line

Is a 457(b) Plan an IRA? FAQs

A 457(b) plan is a deferred compensation retirement plan primarily for public sector and non-profit employees, offering unique withdrawal benefits.

An IRA is a tax-advantaged retirement account open to almost anyone with earned income, while a 457(b) is tailored for the public sector and certain non-profit workers.

Yes, you can typically roll over funds from a 457(b) plan to an IRA, but it's essential to ensure the receiving plan accepts these funds.

While 457(b) plans offer curated mutual fund selections, IRAs, especially with major brokerages, provide a broader array of investment choices.

Consider factors like your tax scenario, employment trajectory, and available retirement options. Seek professional advice if unsure about the best fit.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.