A Stretch Individual Retirement Account (IRA) is a retirement savings account that allows an account owner's beneficiaries to stretch distributions over their lifetime. The beneficiary of a Stretch IRA can choose to take Required Minimum Distributions (RMDs) over their life expectancy, rather than the account owner's life expectancy. This can result in smaller distributions and potentially lower taxes over a longer period. Stretch IRAs are typically established as a type of inherited IRA, and beneficiaries must begin taking RMDs the year following the original account owner's death. A Stretch IRA can be created with various types of retirement accounts, including Traditional IRAs, Roth IRAs, and employer-sponsored plans like 401(k)s, 403(b)s, and 457(b)s. The account owner must have reached the age when Required Minimum Distributions (RMDs) must be taken to initiate a Stretch IRA. To establish a Stretch IRA, the account holder must designate one or more beneficiaries. A beneficiary can be a person, a trust, or an entity such as a charity. Non-spouse beneficiaries are subject to specific distribution rules and may have limited options for continuing tax-deferred growth. The age at which RMDs must be taken for Traditional IRAs and employer-sponsored plans is 73. Roth IRAs do not have RMDs for the original account owner. Beneficiaries must take RMDs based on their life expectancy, but the rules are different for spouses and non-spouse beneficiaries. To create a Stretch IRA, the account owner can initiate a direct rollover from their existing retirement account to a new or existing IRA in their name. This process ensures that the funds remain tax-deferred and continue to grow. A key component of a Stretch IRA is the designation of one or more beneficiaries who will inherit the account upon the owner's death. It is essential to keep beneficiary designations up-to-date to ensure the desired individuals inherit the account. A trust can be named as the beneficiary of an IRA. This option provides added control over the distribution of assets and can protect the account from potential creditor claims against the beneficiary. RMDs are taxable distributions that must be taken from Traditional IRAs and certain employer-sponsored plans. Beneficiaries must take RMDs based on their life expectancy, which can reduce the tax burden and extend the life of the account. Stretch IRAs can help minimize inheritance taxes and maximize the wealth passed on to beneficiaries. By extending the life of the IRA, the account can continue to grow tax-deferred, reducing the overall tax burden on the estate. Beneficiaries of a Stretch IRA can take advantage of continued tax-deferred growth and potentially lower tax rates, depending on their income and the type of IRA inherited. Account owners can designate multiple beneficiaries for their Stretch IRA, allowing the account to be divided and passed on to several individuals. This approach can help spread the tax burden and extend the life of the IRA even further. Converting a Traditional IRA to a Roth IRA can provide tax-free growth and distributions for beneficiaries, eliminating the need for RMDs and potentially providing a more significant inheritance. Incorporating charitable giving into a Stretch IRA strategy can provide tax benefits and support philanthropic goals. Naming a charity as a beneficiary or using a Charitable Remainder Trust are two popular options. The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in 2019, has significantly impacted Stretch IRAs. The Act eliminated the ability for most non-spouse beneficiaries to stretch RMDs over their lifetime. Instead, they must now withdraw the entire inherited account balance within ten years of the account owner's death. The SECURE Act increased the age for RMDs to 73, providing additional time for tax-deferred growth. This change may benefit account owners and their beneficiaries by allowing more time for strategic planning. In light of the changes brought by the SECURE Act, IRA account holders may consider alternative strategies such as Roth IRA conversions, using trusts to control distributions, or exploring other estate planning options. A Roth IRA can provide tax-free growth and distributions for both the account owner and beneficiaries. While Roth IRAs have income limitations for contributions, Traditional IRA holders can convert their accounts to Roth IRAs regardless of income. Life insurance can be used as a wealth transfer tool, providing tax-free death benefits to beneficiaries. Some policies also offer tax-deferred cash value growth, making them an attractive alternative to Stretch IRAs. A Charitable Remainder Trust (CRT) can provide an income stream for beneficiaries, support charitable causes, and offer significant tax benefits. CRTs may be a suitable option for those looking to minimize taxes and support philanthropic endeavors. As tax laws and regulations continue to evolve, it is crucial to stay informed about potential changes that may impact Stretch IRAs and other estate planning strategies. The future of Stretch IRAs is uncertain, given the recent changes brought by the SECURE Act. However, they still play a role in estate planning and wealth transfer, especially for spouse beneficiaries and certain eligible non-spouse beneficiaries. As financial professionals and investors adapt to the changing landscape, new strategies and developments may emerge to optimize the benefits of Stretch IRAs and other wealth transfer tools. A Stretch IRA allows the beneficiary to take Required Minimum Distributions (RMDs) over their lifetime, which can result in smaller distributions and potentially lower taxes over a longer period. The account owner can initiate a direct rollover from an existing retirement account to a new or existing IRA, and the beneficiary must take RMDs based on their life expectancy. Beneficiaries of a Stretch IRA can take advantage of continued tax-deferred growth and potentially lower tax rates, depending on their income and the type of IRA inherited. The impact of SECURE Act has significantly impacted Stretch IRAs by eliminating the ability for most non-spouse beneficiaries to stretch RMDs over their lifetime. In light of the changes brought by the SECURE Act, IRA account holders may consider alternative strategies such as Roth IRA conversions, using trusts to control distributions, or exploring other estate planning options. What Is a Stretch Individual Retirement Account (IRA)?

Eligibility and Requirements

Eligible Account Types for Stretch IRA

Qualifying Beneficiaries

Age Limits and Distribution Requirements

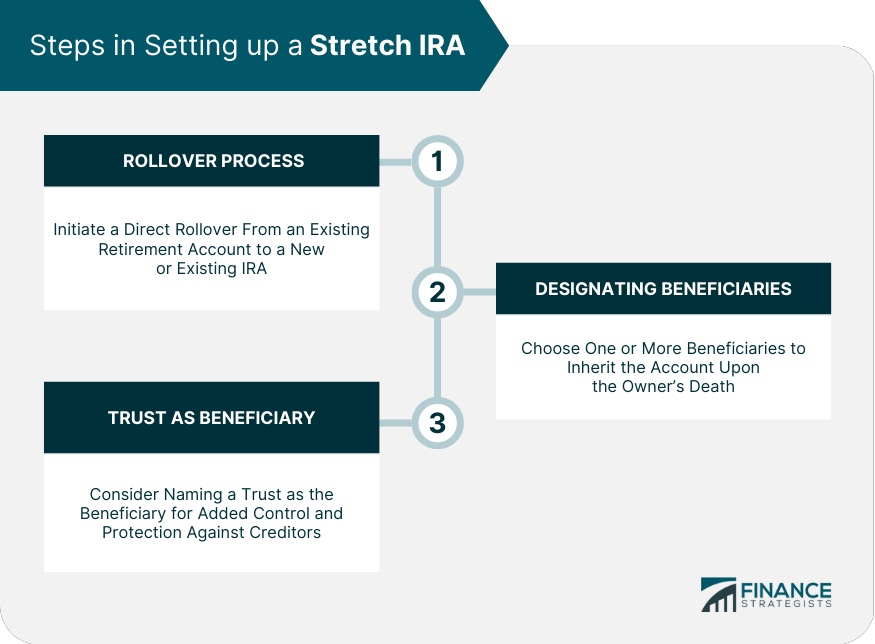

Setting up a Stretch IRA

Rollover Process

Designating Beneficiaries

Trust as Beneficiary Option

Tax Implications

Required Minimum Distributions (RMDs)

Inheritance Taxes and Estate Planning

Tax Benefits for Beneficiaries

Stretch IRA Strategies

Multiple Beneficiary Planning

Roth IRA Conversion Strategy

Charitable Giving Strategies

SECURE Act and Its Impact on Stretch IRAs

Changes to Beneficiary Rules

Modifications to RMD Rules

Strategies for Dealing With New Regulations

Stretch IRA Alternatives

Roth IRA

Life Insurance

Charitable Remainder Trusts

Future of Stretch IRAs

Potential Regulatory Changes

Impact on Estate Planning and Wealth Transfer

Innovative Strategies and Developments

Conclusion

Stretch Individual Retirement Account (IRA) FAQs

A Stretch IRA is an estate planning strategy that allows the account owner to extend the life of their IRA by passing it on to multiple generations of beneficiaries. This strategy enables the inherited IRA to continue its tax-deferred growth, potentially providing a larger inheritance for the beneficiaries.

The SECURE Act, passed in 2019, significantly impacted Stretch IRAs by eliminating the ability for most non-spouse beneficiaries to stretch RMDs over their lifetime. Instead, they must now withdraw the entire inherited account balance within ten years of the account owner's death.

Yes, a trust can be named as a beneficiary of a Stretch IRA. This option provides added control over the distribution of assets and can protect the account from potential creditor claims against the beneficiary.

Inheriting a Stretch IRA can have tax benefits for beneficiaries. They can take advantage of continued tax-deferred growth and potentially lower tax rates, depending on their income and the type of IRA inherited. However, the SECURE Act requires most non-spouse beneficiaries to withdraw the entire inherited account balance within ten years, which may impact their tax situation.

Some alternatives to Stretch IRAs for estate planning and wealth transfer include Roth IRAs, life insurance, and Charitable Remainder Trusts. Each of these options offers different benefits, such as tax-free growth and distributions, tax-free death benefits, or support for charitable causes while providing an income stream for beneficiaries.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.