What Are 403(b) Rollover Options?

A 403(b) rollover option refers to the process of transferring funds from a 403(b) retirement plan, typically sponsored by non-profit organizations, public schools, and certain ministers, to another retirement account.

The purpose of such a rollover is to maintain the tax-advantaged status of the retirement funds when changing jobs, retiring, or for better investment options.

Understanding these rollover options allows individuals to effectively manage their retirement savings and navigate their options during career transitions or other significant life events.

For the readers, gaining insights into 403(b) rollover options can be crucial in informed financial decision-making, potentially impacting their retirement preparedness and long-term financial stability.

In the broader context of retirement planning, knowledge about these rollover options is an essential component of strategic retirement savings management.

Different Options for a 403(b) Rollover

There are several options for a 403(b) rollover, each with its unique features, benefits, and considerations.

Rollover to an IRA

An Individual Retirement Account (IRA) can provide a broader range of investment options compared to a 403(b) plan.

Traditional IRA: A Traditional IRA offers tax-deferred growth, similar to a 403(b) plan. Contributions may be tax-deductible, and taxes are paid upon withdrawal in retirement.

Roth IRA: A Roth IRA offers tax-free growth and withdrawals in retirement, but contributions are made with after-tax dollars.

Rollover to a New Employer's Plan

If your new employer offers a 403(b) or a similar plan like a 401(k) and accepts rollovers, this option could allow for continued tax-deferred growth of your retirement savings.

Rollover to a Personal Retirement Account

For self-employed individuals or small business owners, options like a SEP-IRA or a Solo 401(k) could be viable alternatives.

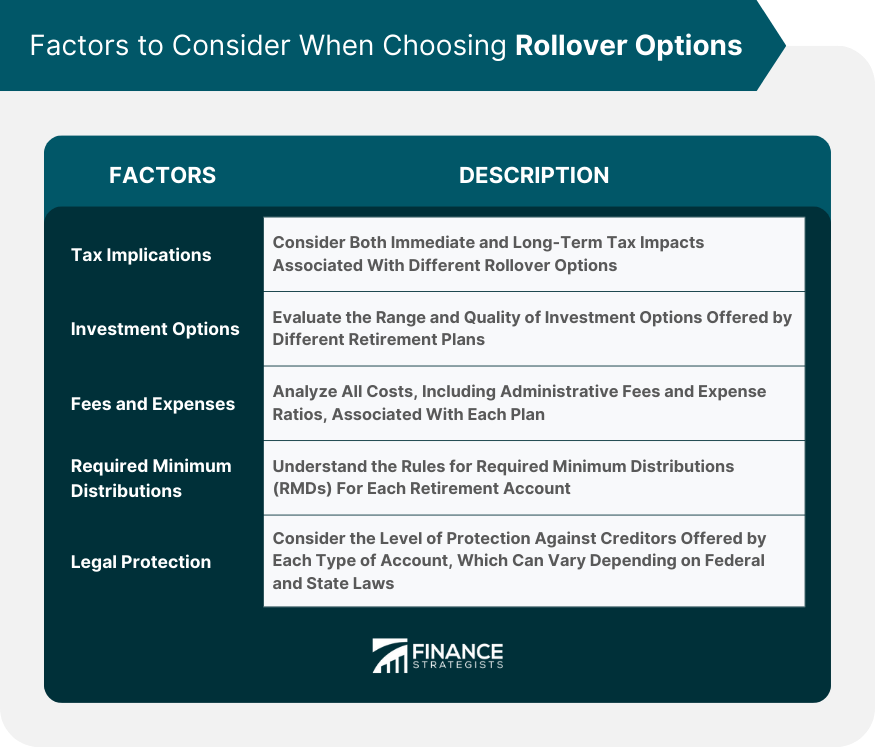

Factors to Consider When Choosing Rollover Options

There are several factors to consider when deciding on the best rollover option for your 403(b) plan.

Tax Implications

Different rollover options can have different tax implications, both at the time of the rollover and upon withdrawal in retirement.

Investment Options

Investment options can vary significantly among retirement plans. Some plans may offer a wide range of investment choices, while others might be more limited.

Fees and Expenses

Costs, including administrative fees and expense ratios of the investment options, can significantly impact the growth of your retirement savings over time.

Required Minimum Distributions

The rules for Required Minimum Distributions (RMDs), the minimum amount you must withdraw from your retirement accounts each year starting at age 72, can differ among retirement accounts.

Legal Protection

Certain retirement accounts, like employer-sponsored plans, have strong protection against creditors under federal law, while others, like IRAs, have variable protection that depends on state law.

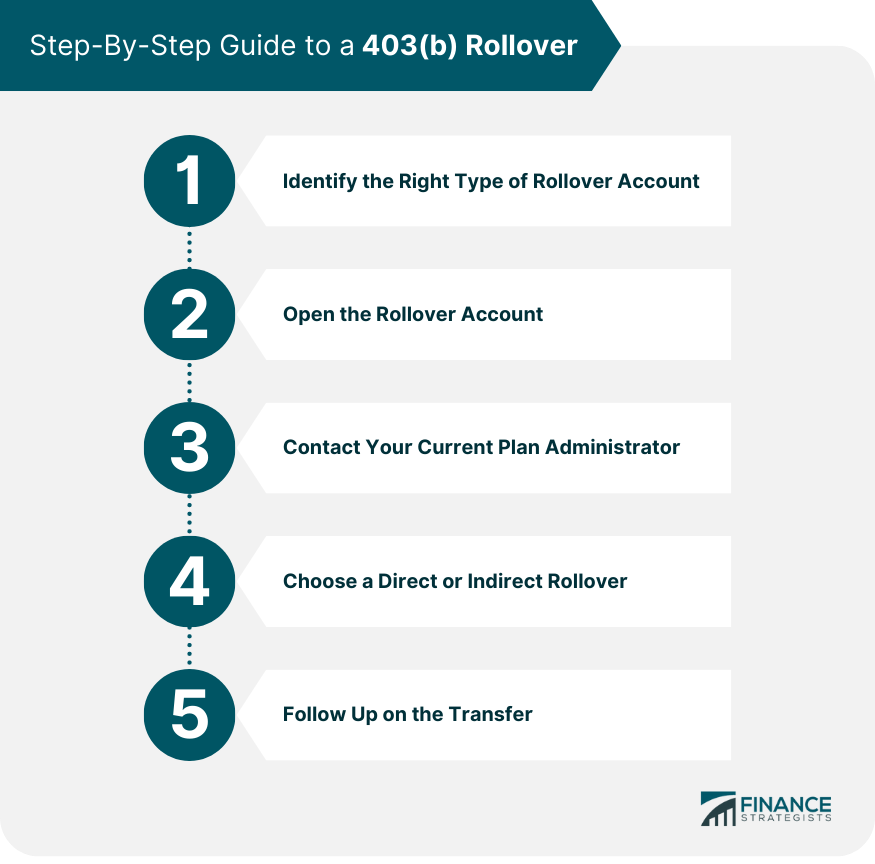

Step-By-Step Process to a 403(b) Rollover

A 403(b) rollover is a multi-step process that involves careful planning and execution.

Identify the Right Type of Rollover Account

Depending on your employment status, future income prospects, and retirement goals, identify the best type of account for your rollover.

Open the Rollover Account

If you don't already have the chosen account open, you need to open it before initiating the rollover.

Contact Your Current Plan Administrator

Notify them about your plan to roll over the 403(b) assets. They will guide you through their specific process and may require you to fill out certain forms.

Choose a Direct or Indirect Rollover

A direct rollover is typically the better option because it avoids potential taxes and penalties.

Follow Up on the Transfer

Make sure your funds have been transferred to the new account within a reasonable time.

Impact of a 403(b) Rollover on Retirement Planning

A 403(b) rollover can significantly influence the trajectory of your retirement planning.

Potential to Grow Retirement Savings

The rollover might provide access to better investment options or lower fees, which can help increase the growth of your retirement savings.

Opportunity for Account Consolidation

By consolidating multiple retirement accounts, you can simplify the management of your retirement savings and ensure a coordinated investment strategy.

Conclusion

Understanding and managing your 403(b) rollover options can significantly shape your retirement preparedness and financial stability.

With several avenues such as Traditional IRA, Roth IRA, or a new employer's plan, your retirement savings can continue to grow in a tax-advantaged environment.

Key considerations like tax implications, investment options, fees and expenses, and legal protections play a critical role in deciding the best course of action.

Conducting a successful rollover involves identifying the right account, opening the rollover account, notifying your current plan administrator, and ensuring a smooth transfer process.

By properly handling your 403(b) rollover, you can tap into better investment opportunities, possibly lower your fees, and simplify your account management.

As each individual's financial circumstance is unique, it's advisable to consult a financial advisor to maximize the benefits of your 403(b) rollover.

403(b) Rollover Options FAQs

403(b) rollover options are pathways that allow you to transfer your funds from a 403(b) retirement plan to another retirement account, maintaining the tax-advantaged status of these funds.

Common 403(b) rollover options include rolling over to an Individual Retirement Account (IRA), a new employer's 403(b) or 401(k) plan, or a personal retirement account if you're self-employed or a small business owner.

Key considerations include tax implications, available investment options, fees and expenses, rules for required minimum distributions, and levels of legal protection against creditors.

A 403(b) rollover can influence retirement planning by potentially providing access to better investment options or lower fees, increasing your retirement savings, and simplifying the management of your retirement accounts.

The process involves identifying the right type of rollover account, opening the rollover account (if not already open), contacting your current plan administrator, choosing a direct or indirect rollover, and following up on the transfer.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.